This blog is devoted to helping investors make informed decisions. It will be regularly updated and provide opinions on earnings results. It is not intended to give investment advice and should not be taken as such. Consult your investment advisor.

Textbooks will tell you that economies work in concert with some kind

of ideal and consistent. Unfortunately, it never quite works out like

that. In the financial sector in particular we have seen some unusual

developments in recent years.

On a historical basis the sector looks cheap, with many of the

leading companies trading at below book value; however, we are living in

uncertain times and the credit cycle is not the same as it once was. So

do the financial companies present good value right now?

It’s different this time

These are some of the most famous last words in investing. They

induce investors into making assumptions that they build into stocks,

which then promptly disappoint them. In the case of the financials we

are seeing ongoing weak consumer demand for loans; however, I think it

would be a mistake to assume that it really is different this time. At

some point--as long as the economy keeps improving--consumer demand for

loans will increase. History suggests that when employment and incomes

increases then loan growth will follow.

With this said it is worth reflecting on how slow the recovery has

been. Employment gains have been on a par with previous recoveries, but

nothing near enough to recompense for jobs lost in the recession.

Moreover, we have come through a few years of consumers deleveraging,

and such behavior can become habitual. Meanwhile, the

Federal Reserve is doing anything it can to throw liquidity into the

economy. Interest rates are low and financials are facing declining net

interest margins as they struggle to replace higher rate loans that are

maturing. A veritable mix of pluses and minuses.

How this plays out in the Industry

We can see these issues playing out in the metrics of the lenders. For example, here is Discover Financial Services' (NYSE: DFS) net charge off rate and delinquency rates for its US credit loans.

Clearly asset quality has improved in a rather dramatic way since the last recession, and it is notably lower than before.

While asset quality has improved across the board, low interest rates

have created net interest margin (NIM) difficulties. For example, here

is a look at Wells Fargo’s NIM numbers.

In the case of Wells Fargo It has seen significant increases in

deposits, which created pressure on its NIM while new mortgage

origination hasn’t been as strong as many might have hoped.

In a sense the whole industry is positioned in a similar manner.

Asset quality is improving, but consumer demand remains weak and many

loans are maturing, leading to significant amounts of runoff and capital

appreciation.

Enter Capital One Financial

Within financials the stocks that I like are Wells Fargo (on the

basis of its exposure to the US housing market and conservative

approach), Goldman Sachs because it still trades below book value and offers significant upside from exposure to more M&A activity this year, and Capital One Financial .

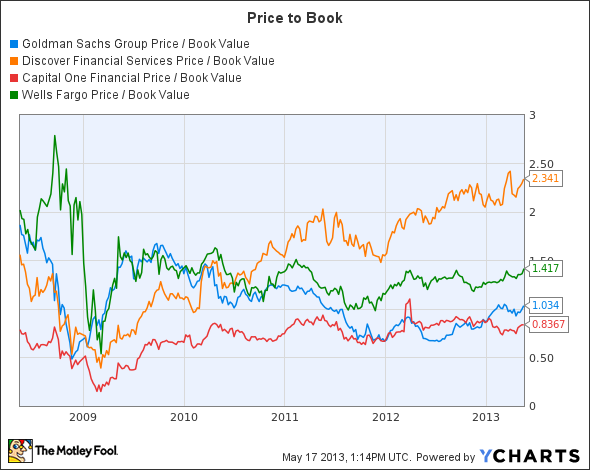

Here are the price to book numbers for the stocks discussed in this post.

Discover’s evaluation reflects its more aggressive approach to

lending, while Goldman Sachs remains subject to regulatory risk.

Nonetheless I think Goldman is good value. I’m not the biggest fan of

this company and the way that successive administrations have catered to

its interests, but I’m willing to bet that these trends will continue

and regulatory fears will ease. As for Discover, investors have to ask

themselves if it is chasing too much business.

Good Value?

Evaluations are attractive, but these stocks will not have such good

value if lending doesn’t come back. My point is that if the economy

continues to improve then at some point loan demand will surely return.

However if it doesn’t (or if the same weak environment ensues) then I

would rather be invested in a financial with a traditionally

conservative approach to lending. In this regard I think Capital One is a

good option.

Drilling down into the details of Capital One’s latest numbers it’s

clear that it expects run-off to continue this year and the next. It

plans for $12bn in 2013 and then a further $8.5 billion in 2014. So

while its credit performance is good, consumer demand is still weak. It

would be understandable if its management then decided to chase growth

in areas like auto loans (which grew $800 million); however its auto

loan originations declined by $500 million in the quarter as they

refused to chase low quality loans.

In essence Capital One is a more conservative lender that still gives

exposure to the upside of an improving economy. The fact that areas

like auto loans have offered growth to lenders hasn’t caused Capital One

to create potential areas of weakness in its loan book which could then

threaten the company’s ability to lend in future.

Moreover, it is planning to use its capital appreciation to reward

investors with buybacks and is already in talks with regulators about

this.

The bottom line

Capital One offers a solid way to get exposure to the financial

sector without too much risk. I think investors should take this into

consideration rather than just looking for broad-based financial

exposure.

Its evaluation is not expensive on a price to book basis, and a

dividend yield north of 2% plus the prospects of further capital returns

to shareholders offers upside prospects if the economy continues to

grow.

Another week and another set of earnings in the industrial space that

confirms the curious bifurcation in the sector. Companies selling to

the aerospace and automotive sectors had a good quarter, while others

found things a lot tougher. Such thoughts came to mind when looking at Precision Castparts' latest results. In this article I want to delve into the reasons why, and suggest some other stocks in the aerospace sector.

Precision Castparts lifts off

The bifurcation that I spoke of above was further demonstrated in

these results. Fortunately for Precision Castparts’ investors, the

company has increased its exposure to aerospace. It now makes up 67% of

revenues, vs. 64% last year. The Timet acquisition has helped while

also allowing it to generate operational efficiencies and synergies.

A quick breakdown of revenues demonstrates the positive effects of Timet on the forged products segment:

And a breakdown of operating income in the quarter shows how it makes its money:

Moreover, there is still plenty of growth to come as it ramps up

production (notably by getting its 29,000 ton press back to full

capacity by the end of the year) for the Boeing 787 this year. It will do similar with the 737 next year. Fortunately,

large commercial aerospace makes up 75% of its market, with military

only at 17%. Elsewhere, its other segments saw less than stellar

performance, with power falling to 18% of sales from 21% last year, and

general industrial remaining flat at 15%.

What the industry is saying

Focusing on the macro aspect of its results, investors need to

understand that the commercial aerospace industry is highly cyclical.

The good news is that in this cycle the airlines have been surprisingly

profitable. I discussed some of the reasons why here.

In summary, I think airline profitability is better this time, due to

a combination of factors. Austerity measures have brought about a

reduction in the willingness of governments to subsidize loss-making

‘national champions'. At the same time, financing has become harder for

new entrants. In addition, the growth in emerging market

passengers has created new growth drivers for the industry. And finally,

the airlines have had a few years to adjust to high oil prices. The really interesting point is that –past the short term- profitability does not appear to correlate with oil prices. All said, it is a better operating environment for the airlines.

We got a good early read on the current strength of the industry when Alcoa reported results. It was a generally positive set of numbers

from its end market perspective. With regards to aviation, Alcoa stuck

to its previous bullish guidance of 9-10% global growth this year, with

particular strength coming from emerging markets. The issue with Alcoa

is not necessarily its end market growth, but rather the state of

overcapacity in aluminum production. Its aviation demand remains strong.

Therefore, it is not surprising that Boeing has been beating

estimates and looks set to continue. Naturally, the aviation industry

will never truly escape being cyclical, but as long as the global

economy remains on track, it is a sector that can outperform. This is

good news for Boeing, Precision Castparts, and other players like cabin

manufacturer BE Aerospace.

The latter is one of the most interesting names

in the aerospace sector, and offers a rare way to get pure exposure to

commercial aerospace. Its growth prospects rely on a mix of retrofit and

new build demand. In addition, it is a key beneficiary of the trend

towards wide bodied aircraft, and has a number of new innovations, like

its lavatory system for the 737 which allows airlines to gain a few

extra seats. However, I think its key plus point relates to the

profitability of airlines. If the industry is on a more sustainable

path, then airlines will be better positioned financially in order to

retrofit planes, rather allow them to depreciate.

Where next?

On a stock specific basis, this means that companies like Precision

Castparts can continue to outperform. It offers a combination of upside

from a ramp-up in production, plus synergy opportunities. Both

activities can increase margins going forward. Similarly, something

like BE Aerospace is going to benefit from more favorable industry

financials. Boeing is an obvious momentum play. If you are

bullish on the global economy and particularly emerging markets, then

all these stocks represent attractive propositions.

Tech investors have seen a slew of warnings over the last few months, so Cisco Systems' (NASDAQ: CSCO)

recent ‘beat’ was always likely to be well received. As ever with

bellwethers, there is as much interest in what its constituent segments

mean to the tech industry as there is in its own prospects. Moreover, as

Cisco is reporting late in the quarter, there may be some indication

that the tech market is going to recover from a weak calendar Q1.

Cisco cheers the Market

After heavyweights like IBM, Oracle,and

basically any company that sells anything to service providers

delivered disappointing numbers, investors were entitled to expect Cisco

to miss as well. However, the company has always been a little

different than others thanks to

the strength of its

government-based business (which made it relatively weaker last year as

austerity measures crimped expenditures). This can cause some lumpiness

in results.

a huge cash pile with which it can invest to buy growth. Indeed, acquisitions have always been a major part of the strategy.

Its ability to bundle solutions together in order to generate growth across all segments.

I think these factors need to be understood before looking at the

results. In summary, I think its core business of switching, routing,

and services was a little bit disappointing. The good performance was in

the non-core activities where acquisitions and the ability to bundle

solutions may well have helped out. Nonetheless, this was a positive

report overall for the tech sector.

On a geographical basis, the Americas grew 7% with some surprising

strength in its U.S. commercial business, which was up 10%, and in a

bullish marker for the tech industry, its U.S. enterprise numbers were

up 10% with service provider-based revenue up 10%. In fact, this is a

continuation of the strength that Cisco saw in the last quarter with

regards to U.S. enterprise.The U.S. public sector grew 5% with local and

state growth of 13% counteracting a 3% decline in Federal.

EMEA was flat with some signs of ‘bottoming out’ being cited.Asia-Pacific was somewhat more disappointing with only 1% growth and some Cisco specific issues were cited in China.

Cisco’s core business

You can access a review of Cisco’s previous numbers in an article linked here.

Switching was a bit weaker than I had expected because previously, it

had said that switching revenue would be flat for this quarter and the

next. Routing revenue was flat year on year but saw a nice sequential

increase from a disappointing quarter in Q2.

Services revenue growth was only 7%, and this reflects the lower

growth profile that the company has had in the last couple of years. It

calls into question whether Cisco will hit its 9%-11% CAGR target for

services in the next 3-5 years.

A graphical depiction of these segments growth depicted below.

Having looked at what Verizon(NYSE: VZ) said recently over its enterprise customers' spending patterns

and their ongoing cost cutting first based approach, it is no surprise

to see Cisco’s switching and routing revenue entering a period of

weakness. Switching had a stronger quarter in Q2, but in common with the

rest of the industry, this quarter delivered a weaker set of numbers.

For Verizon investors, Cisco's positive commentary on enterprise

spending must be a plus going forward.

Whereas Verizon has rolled out much of its next generation network, AT&T(NYSE: T) is supposed to be playing catch up. However, in its last results,

it announced that its capital spending plans would be reduced by 9% for

the next two years. This is clearly disappointing because it was one of

the service providers that the market was hoping would give a lift.

So, if the core results were a bit disappointing, where was the good news?

Cisco grows its non-core revenue

For a mix of reasons there was better news in its non-core activities. Starting with Service Provider and Collaboration.

While the SP Video results look great, they were largely a

consequence of the NDS acquisition. This is no slight on Cisco, because

the idea that it can use its cash pile to buy growth is a big plus

point, but it does suggest that it should make more acquisitions.

Unfortunately, poorly timed acquisitions in the collaboration sector may

well have dimmed the market’s confidence in its strategy. Speaking of

collaboration, it saw conferencing rise 11% but there was more

‘softness’ within telepresence as it continued to decline.

It is, therefore, somewhat puzzling to see Polycom(NASDAQ: PLCM) rising in sympathy. I think this end market may well face some structural challenges

in the next few years. IT spending trends are favoring mobility, open

source platforms, and cloud-based solutions rather than hardware that

ties purchasers to do things like use a fixed room within a location in

order to engage in ‘telepresence’.

Turning to Wireless, Security, and Data Center, it is here that we can see the strength in these results.

Data Center has been a stand out performer for Cisco for some time,

and its unified data center strategy is enabling it to offer integrated

solutions to its customer base. Moreover, Cisco is executing very well

in wireless. Telco budgets are shifting from wireline to wireless and it

is essential that Cisco takes advantage of this. In particular, its

service provider wi-fi growth was quoted as being ‘extemely strong’

while its wireless local area network group was up 17%.

I read this as a positive for a stock like Ixia (NASDAQ: XXIA).

Not only is Cisco a major customer, but the company’s test, assess, and

monitor solutions are well placed to take advantage of enterprise

spending on wi-fi and LANs. If Cisco is rolling out more networks, then

Ixia should be well placed to benefit from spending on making sure those

networks function effectively.

The bottom line

Frankly, in the current environment, the market will take a lot of

heart from these results and the relief rally is evident. Cisco didn’t

beat by much and its EPS guidance of was in line with analyst estimates,

but it has been such a tough quarter for tech and Cisco’s commentary

(particularly on U.S. enterprise spending) was positive.

In reality, it was a mixed performance with its core businesses

demonstrating sluggish growth, but the strength in its non-core

activities is pointing the way to the future. In short, Cisco needs to

use its cash pile to make acquisitions. The good news is that it can,

and consequently, it still presents a decent value proposition.

It’s been a disappointing earnings season for technology stocks. A

marked reluctance among telcos and enterprises to sign off on big deals

has caused company after company to miss earnings and lower guidance. In

this environment any company that merely hits guidance is a 'winner.'

With these thoughts in mind the market liked the recent results from NICE Systems(NASDAQ: NICE).

In fact I got the impression from the tone of the questions on the

conference call that the analysts were rather surprised at how well it

all went.

NICE guys come first

Nope not a throwback to before the dark ages of feminism but a reference to NICE Systems earnings in the quarter

Q1 Revenues $225 million vs. internal guidance of $220 million-230 million

Q1 EPS of $0.61 vs. internal guidance of $0.57-$0.62

Q2 Revenue guidance of $220 million-230 million vs. analyst consensus of $231.9 million

Q2 EPS guidance of $0.58-$0.64 vs. analyst consensus of $0.62

Full year revenue guidance of $940 million-970 million vs. analyst consensus of $957 million

Full year EPS guidance of $2.55-$2.65 vs. analyst consensus of $2.61

The results were pretty much in line and the guidance for the full

year was left unchanged. This is good in relation to what others have

been reporting but it is also encouraging for NICE shareholders because

the company is becoming more back end loaded in its results. In other

words, earnings are being pushed towards Q3 and particularly Q4. It’s

great when they come in as expected but investors will always have

concerns when in Q1 & Q2. I discussed some of the reasons why in an article linked here.

NICE Systems earnings drivers

In essence NICE is seeing larger deals coming in (a notable contrast

to the rest of the tech world) as it is able to sell on more advanced

applications solutions to its customers. While this is obviously good

news it also means that bookings may take longer to translate into

revenues. In addition the sales cycle will be longer with these types of

complex deals. All of which means that earnings and revenues are

becoming more back end loaded (a lot of deals will be signed in Q4).

A graphical depiction of what to expect can be seen here.

The company is looking for bookings of above $1 billion in 2013. A

quick look at the revenue guidance of $940 million-970 million confirms

that the book to bill is expected to be above one this year. Another

good sign is that it claimed the growth was coming from its existing

customers, which implies that it has good opportunities to sell its

advanced applications into its installed base.

With all this good news going on, investors are entitled to ask how it hit guidance when so many had missed?For example TIBCO Software(NASDAQ: TIBX) gave a horrible set of results recently and this company has questions to answer over its guidance.

Although not strictly speaking a competitor, TIBCO is exposed to

enterprise spending on big data analytics.TIBCO needs to demonstrate

that it can turn around its poor performance with its US sales

execution. In addition it has spent a year blaming this region for its

problems but now its European operations are performing poorly too. My

guess is that this because its solutions maybe tied to expansionary

spending expectations (marketing budgets etc) rather than the sort of

efficiency gains that NICE offers.

Moreover IBM

also missed estimates (a rare event in itself) amidst discussion of a

weaker macro environment. Its analytics results were relatively stronger

and there is a suggestion that it is taking market share from TIBCO.

However it was hardly a strong statement regarding the overall spending environment.

Why NICE Systems is doing so well

Some reasons why it did so well are that other than the opportunity

to sell its advanced applications to a mature and large installed base I

think its solutions are somewhat non-discretionary. Whereas a

corporation may hold back on investing in new marketing expenditures

(TIBCO) and on upgrading its IT (IBM) if a company is facing increasing

security, money laundering or regulatory & compliance requirements

it will need to invest. Indeed NICE has a deal with IBM to incorporate

its analytics solutions within its services.This gives both companies

advantages to sell through services particularly with financials.

Moreover NICE’s new solutions largely involve analyzing customer

interaction data that its systems are already capturing. In other words

it is a proposition largely based on productivity and efficiency gains

rather than purely growth.It also means companies can buy a range of

solutions from one supplier.

Longer term there is always going to be speculation over a potential tie up with its rival Verint Systems(NASDAQ: VRNT). The companies aregood potential partners

thanks to complimentary end markets and customers. NICE is strong with

financials and call centers while Verint has more strength with

Government business and security solutions. Indeed Verint’s recent

results were quite good and

I think its guidance may prove to be conservative. Verint's focus on

security should enable to grow as there is no shortage of worries over

cyber attacks and in particular with Government agencies. A deal between

the companies is a real possibility due to complimentary end markets, a

common culture (both are Israeli) and they are likely to share many

shareholders in common as a consequence.

Where next for NICE Systems?

Anyone predicting that he had found a corner of tech that is

oblivious to the slowdown in Q1 would have been left with egg on his

face, or rather an omelet. So I would be cautious with expecting too

much here.

With that said NICE seems to be on track to hit its full

year guidance. In terms of evaluation the current PE may seem high at

33x but its cash flow conversion is excellent. This business has

generated an average of nearly $126m in free cash flow over the last few

years. Compared to its market cap of $2.18 billion and enterprise value

of $1.85 billion this makes the stock good value and I think the

analyst consensus target of $40 is achievable.

t’s been a pretty good earnings season for the home furnishings industry, and Restoration Hardware $RH continued the good cheer by upgrading its Q1 guidance only a few weeks after reporting an impressive set of full year results.

The company has a number of positive drivers behind it. It marries a

recovering housing market with the spending power of the high-end

consumer and a collection of ongoing operational improvements along with

new category launches. In summary, it is well worth a look for anyone

wanting to get exposure to the sector.

Restoration Hardware upgrades

Before going into details, I want to outline the changes to guidance.Note that these changes were made on May 10, having been previously been issued on April 18.

Q1 Revenue guidance of$295 million-300 million versus $280 million-285 million.

Q1 adjusted diluted EPS guidance of $0.02 to $0.04 versus$(0.02) to break-even.

Q1 Adjusted net income guidance of $900,000 to $1 million versus $(1) million to break-even.

The increase in Q1 guidance is expected to be incremental to the full year guidance, so start penciling in upgrades folks.

For the sake of clarity, the existing full year guidance is $1.42

billion -1.45 billion in revenue and $1.29-1.37 in adjusted EPS.

It’s an impressive hike and the company lost no time in announcing on

the May 14 that it would launch a follow-on offering of 7.5 million

shares to be sold by existing stockholders. The business appears to be

firing on all cylinders, so what should investors look out for going

forward?

Restoration Hardware’s growth drivers

I’ve previously discussed the stock in an article linked here which should give some good background reading.Regarding its growth drivers for 2013, I have a few bullet points

Increasing the number of its full line galleries

Growth from new business launches such as RH Tableware and RH Objects of Curiosity

Opening of distribution centers in order to increase capacity and improve service

Expanding its baby and child offerings

Developing its contemporary art offerings

It’s worth noting that despite the 30% increase in net revenue in Q4,

gross margins actually fell 200 bps to 36.5%. This is largely a

consequence of the increase in lower margin furniture sales as part of

overall revenue. Going forward, investors should look to initiatives

like the new business and, in particular, the contemporary art offerings

to increase margins as they contribute more as a share of revenue. No

matter the revised Q1 guidance implies 35%-38% revenue growth.

With that said, the key to its growth will be the increasing number

of full line galleries. I note that previously, the company argued that

only 25% of its current assortment was being displayed in retail

galleries, but it recently quoted a figure of 20% (and below 15% if baby

and child categories were included).

The opportunity is to expand retail space (via full line galleries)

and maximize the potential in its overall assortment. Indeed, it

declared that the first three full line galleries in LA, Scottsdale and

Houston were outperforming expectations, and with new galleries being

opened this year, we can expect more of the same.

What the Industry is saying

It is certainly not alone in reporting good numbers, although I note

that other companies have differing operational improvements planned in

order to benefit from an improving housing market. For example Pier 1 Imports $PIR is following a strategy

of expanding its e-commerce activities and in store point of sales

systems in order to drive new channel growth. Meanwhile its Q4

same-store sales numbers came in at an impressive 7.5%. My longer term

concern here would be that its e-commerce activities might cannibalize

its in-store offerings and place extra pressure on it to innovate in

order to achieve product differentiation.

Another good indicator for Restoration Hardware is Williams-Sonoma $WSM.It has seen good growth

in its pottery barn kids and teens categories, and in addition to

expanding its e-commerce and direct to consumer sales channels (now 46%

of total sales), it has an ongoing international expansion plan.However it also needs to keep a focus on achieving product differentiation because online specialists like Amazon are entering the space. Just like Pier 1, the company is targeting mid to high single digit revenue growth. Impressive stuff.

And finally, I think Bed Bath & Beyond $BBBY is worth a mention. I think it has been the business most challenged by online competition and is finding it difficult to hold onto margins.

With that said, it too is shifting to offering multi-channel

distribution amid launching new websites and integrating acquired

business. Rather, like Restoration Hardware, it offers some upside from

improvements in operational efficiency, but on the downside, it also has

a lot more specific competitive activity (Amazon et al) potentially

targeting its revenue base while its growth has been less than stellar

in recent times.

The bottom line

In conclusion, I think momentum is with the sector and it is a

favorable time to be invested in it. Analysts will likely raise full

year estimates so the top end of existing company guidance at $1.37

looks beatable. At least I would hope so, because at the current price,

it puts it on a forward evaluation of 37 times earnings.

It’s not the sort of stock or evaluation that I would chase, but we

have all seen how some stocks can perform when momentum is behind them

and they are raising guidance. Don’t be surprised to see this stock

higher by the year end, but be prepared for some significant downside if

it misses any numbers and the growth story loses its luster.

t has been a somewhat perplexing reporting season for many

companies in cyclical industries. I’ve detected a recurring trend with a

number of technology and industrial companies. Simply put, Q4 of last

year ended quite strongly, and encouraged a sense of optimism that many

companies haven't lived up to in 2013. The result is that many warned

and lowered guidance.

Is now the time to take advantage of lowered expectations and

cheaper share prices? I want to look at three factors that might help

you make your mind up.

IT Staffing Companies are reporting good growth

Following the earnings misses at tech bellwethers like IBM and Oracle(NASDAQ: ORCL)

investors in staffing companies must have been fearing the worst over

prospects for their tech operations in their upcoming results. However,

the reality turned out much better than most could have predicted.

On Assignment(NYSE: ASGN)

is a staffing company that generates the majority of its revenues from

the IT sector. It reported a strong start to the year and guided towards

the high end of its previous full year forecast. Its IT end markets

were cited as being particularly strong- with the largest growth coming

from healthcare, telecoms & media. Overall revenue was up 13.6% and

the stock rose double digits in response. Moreover, the outlook for its

tech sector was flat for Q2 vs. Q1; in other words it is not reporting

any sequential slowdown, and strong demand will continue.

In addition, Robert Half International (NYSE: RHI)

reported good results within technology. Overall its numbers were a bit

disappointing, but this is largely due to weaker European results. In

comparison the US numbers were in line with expectations, and it

declared that this was the first quarter in years in which its tech

operations had reported sequential improvement. Investors will hope it

can stabilize its European operations.

My view is that the strength that the staffing companies have

seen in tech is a consequence of underlying structural strength. Whereas

the weakness reported by the software companies is more of a tactical

response to fears over sequestration.

Business survey’s are indicating strength

If this is a tactical issue –which could be resolved pretty

quickly- then business surveys should be showing underlying strength. I

find the Duke University Fuqua CFO Business Outlook Survey to be a useful indicator of corporate spending plans.

I’ve broken out the key data that interests us:

It’s clear from the graph that capital and technology spending

tends to lag the earnings growth outlook. This is also intuitively true

because if revenues are rising then the spending needed to service it

should grow too. Note also that employment plans appear to be improving

this year.

It sounds good, but we still need to reconcile this sort of

survey data with the reality that tech spending was weak in Q1. My view

is that, again, this is due to some sensitivity over short term events

rather than an underlying malaise.

We’ve seen this before

If this argument holds, then we should have seen elements of it

previously. Political and economic uncertainties have been with us for a

while, and they are not going away anytime soon. In a sense I think

businesses have become hyper-sensitive to them. As I’ve articulated in an article here,

corporations and individuals have cleaned up their balance sheets and

debt situations. It’s now time for the government to do so.

The current worries are over the effects of the sequester on

the economy and they were around last year too. They hit their zenith in

Q3 over ‘fiscal cliff’ worries. I would argue that this is why we saw

such a relatively strong Q4 in technology. In other words, firms held

off from spending in Q3, which then got released in the next quarter.

For example, IBM talked of US orders falling off a cliff in

September and spooked the market, only to report a strong quarter in the

next set of results. Guess what? IBM missed estimates this time around

as sequester fears kicked in. Oracle also gave a disappointing set of

numbers this quarter and blamed it on internal execution. Even smaller

companies like F5 Networks(NASDAQ: FFIV), Fortinet, Citrix Systems,TIBCO Software and others have warned over profits.

Fascinatingly, they have all said a similar thing with regards

their pipelines. None have seen them reduce –as they might in a

systematic slowdown- but rather that there was a failure to convert them

into orders. The reasons for this differ with the individual companies.

F5 and Fortinet saw notably weaker performance from telcos, Oracle

blamed sales execution, IBM blamed a mix of things, while Citrix Systems

said a new solution caused order delays.

Of these companies I think TIBCO may be facing competitive

pressures, and F5 Networks' near-term prospects are somewhat made

unclear, thanks to its product refresh taking place. These things can

take a quarter or two to work themselves through, so anyone looking for a

tech stock to play a 'bounce back' may want to be a bit cautious with

it for now. In addition, Citrix reported a good quarter with its rival

Netscaler product, so it may well be taking market share from F5.

I think that they all experienced some tactical reluctance

amongst customers, with many of them adopting the same ‘wait and see’

approach that they did in Q3.

The bottom line

If this thesis is correct, then this is not the time to go

underweight in technology, and investors should hold their nerve with

some of the disappointing results we have seen in the quarter. If Q2

bounces back in the way that Q4 did, then the sector could outperform in

the coming months.

It’s been a varied reporting season with a general uptrend in markets

accompanying more than a few profit warnings. If you’ve been holding

some of these names before the disappointments then it has been painful.

The good news is that these situations can create buying opportunities.

I think Allergan(NYSE: AGN) is a case in point, and here is why.

Allergan’s Outlook

It was almost a tale of two reports. On the one hand Allergan's

ongoing operations are performing a bit better than expected while on

the other, there was some disappointing news with regards clinical

trials. The stock promptly sold of aggressively as the market discounted

future revenues from the two problematic programs. I will come to the

trial issues in a bit, but first here is how Allergan adjusted its full

year guidance for product sales.

As the table demonstrates there was a slight increase in the bottom

end of the revenue ranges, so obviously the mid-point of guidance has

been increased. The only product that saw the top end of guidance hiked

was Restasis (therapeutic dry eye). In addition there was quite a bit of

positive news on its key neuro modulator Botox.So if the guidance remains upbeat, what happened in the current quarter?

What Allergan Reported

Despite the positive guidance, sales in the quarter for its

ophthalmic products (47% of total product sales) were below long term

trends at just 3.2% in local currencies. While Botox sales (32% of total

product sales) came in with a much healthier 15.4% increase, ophthalmic

sales were affected by a decrease in Lumigan (eye pressure) sales

thanks to the discontinuation of a formulation of Lumigan. No

matter--sales should recover going forward as the inventory channel gets

filled up again.

All of this should interest Novartis(NYSE: NVO)

shareholders because it is engaged in a legal battle with Allergan over

Lumigan patents. Novartis is believed to be able to get a generic

version to the market in the next few years, provided it can avoid

infringing any patents. Restasis sales increased by 11.2% in local

currencies amidst an increase in consumer awareness, partly promulgated

by Allergan investing in direct-to-consumer marketing.

However, the really good operational news was with Botox. I confess I

was somewhat concerned going into these results as two competitors

appeared to be shaping up to try and grab some market share from

Allergan and Botox. First, Merz Pharma was able to start

re-commercializing Xeomin for aesthetics in the quarter. Meanwhile, Valeant Pharmaceuticals'(NYSE: VRX)

purchase of Medicis was partly intended to integrate Dysport into its

dermatology unit. As it turned out –at least according to Allergan-

Xeomin sales only increased slowly in the quarter and its market share

was cited as being just 5%. Meanwhile Dysport’s share was reported to

have dropped to 13% from 16% last March. Valeant will surely invest in

Dysport in time, but for now Botox has the momentum.

Moreover, the overall market is growing at 14% and Botox’s overall

market share is believed to be about 78%. It is also able to generate

future growth in areas like spasticity, chronic migraine and urology

indications. Aesthetic growth remains very strong--despite a weak global

economy--as the stretchy face look seems to show no signs of losing

popularity.

What Went Wrong?

The stock got hit thanks to delays to its DARPin (macular

degeneration) program. The Phase II data suggests product

differentiation with the control (Roche’s Lucentis), and this is

believed to have put the program back by up to two years. This is great

news for Regeneron Pharmaceuticals(NASDAQ: REGN)

shareholders because its rival product Eylea will now have more time to

entrench its market share. It is difficult to predict whether the

DARPin program is a bust or not, and Allergan was understandably

tight-lipped over giving an opinion before they release a comprehensive

examination of the data. My general view is that delays tend to decrease

the chances of success rather than increase. Regeneron should sleep a

bit more comfortably over the issue.

In addition the Bimatoprost (scalp hair loss) Phase II trial failed

to demonstrate sufficient efficacy in order to proceed to Phase III, but

the Phase II trial is now being extended to include a ten times higher

concentration. Enrollment with male patients will begin in Q3. All of

which leads me to wonder –if safety doesn’t appear to be a issue- why it

wasn’t tested in the high concentration anyway?

Where Next For Allergan?

Investors need to recall that neither DARPin nor Bimatoprost were

inside the time frame of Allergan’s five year plan. In other words this

company can go on generating mid-teens earnings growth for the next few

years and at least high mid-single digit revenue growth. In addition its

existing long term growth drivers are excellent and, from here, I think

any good news with the two clinical programs discussed here will

provide upside.

In conclusion you are getting as high quality, highly cash generative

name that has been sold off aggressively and I think it’s worth picking

Allergan up.

There are three positive earnings drivers to look out for with Stanley Black & Decker( NYSE: SWK),

and if they all come together in 2013, then this stock has significant

upside potential. It is a nice mix of value and growth.The company

offers a nice mix of improving end markets, ongoing cost savings from

synergies created via acquisition integration, and it has a strategic

growth initiative in place in order to drive revenue growth and return

on capital. In this article, I want to look at how these three facets

are playing out so far this year.

End market prospects

The recent results were a mixed bag, as estimates were missed but the

full year guidance for EPS and free cash flow was maintained at

$5.40-$5.65 and $1 billion, respectively. The strength in its mix of

business is undoubtedly coming from its construction and do-it-yourself

(CDIY) segment and it is set to continue. Meanwhile, its security and

industrial segments have more subdued prospects this year.

A breakdown of segmental profits in the quarter.

The results were superficially disappointing. Organic revenue

declined 1% overall, and it was only the 4% contribution from

acquisitions that caused the top line growth of 3%. Moreover, cash

outflows were greater than expected in the quarter and its core CDIY

segment saw flat revenue. It gets worse. Security revenue fell 1% on an

organic basis as did industrial revenue. So, is this a story of

declining organic growth and an over reliance on acquisitions? And where

does the confidence to maintain full year guidance come from?

The 2013 guidance is for mid-single digit revenue growth in CDIY, and

flat to low single digit growth for security and industrial,

respectively. With regards to CDIY, there were three issues of which two look like they will be rectified in due course.

Firstly, there is a late start to the North American outdoor season

which was primarily caused by the weather. Secondly, there has been some

temporary weakness in Latin America due to a variety of reasons.

Interestingly, Whirlpool(NYSE: WHR)said a similar thing

about the region, and in particular with Brazil. Both of these

companies are arguing that this is a temporary setback and Whirlpool

shareholders should take heart from the positive trends expressed for

Latin America in these results. Sequentially, things got better in Q1

and this gives confidence that Q2 will be better for both companies.

The third issue is -- you guessed it -- Europe, but investors need to

recall that comparisons are likely to get easier going forward.

Security’s exposure to Europe is worrying (and there was some temporary

weakness in the Nordic regions), but an extra $15 million of cost

synergies from the Niscayah acquistion are expected. This should help

out margin growth. It’s a similar story with industrial where moderate

U.S. growth is hopefully going to offset weaker conditions in Europe.

Another company displaying confidence in the North American outlook is Masco(NYSE: MAS).

This is more of a leveraged play on new housing construction, and its

margin expansion and operational leverage opportunities will come from

new builds, but its repair and remodeling market is also expected to

grow moderately. Frankly, I think the latter tends to key off the

former, and as long as there is good turnover in housing, then prospects

will get brighter for all the companies discussed here.

Acquisitions working well

The scorecard over its acquisition strategy over the last few years

is positive. It has been a difficult few years for housing and

construction related stocks, but I think it has done the right thing in

trying to drive cost synergies with its acquisitions. As discussed

above, there is an extra $15 million to come from Niscayah (security)

which should bring the total for 2013 to $50 million, and management is

currently evaluating the potential for increasing the targets for 2014.

Strategic growth initiative

I’ve haven’t got the room to discuss this in great depth here, but investors wanting more color on this can find it in an article linked here.

A graphical summary of the plan to increase revenue by $850 million

and profit by $200 million within three years is shown below.

Its early days, but the plans were declared as being ‘on track’.

Indeed there was a bit of extra investment in this program although

there was no adjustment to the targeted CapEx/Revenue figure of

2.5%-3.5%.

The bottom line

This is an attractive proposition and if it can hit its $1 billion in

free cash flow, then the stock would be generating nearly 6% of its

enterprise value (based on the current share price of $77). This is

cheap for a company expected to grow revenue in mid-single digits and

earnings in the mid teens for the next few years.

Ultimately, investors will have to price in the uncertainty that it will hit these targets. If

you are positive on the global economy, then this stock is going to

give you some upside potential and I think a target price in the mid

$80’s is not unreasonable. A good GARP candidate.

After Verizon(NYSE: VZ) had given a mixed

prognosis for the telco sector, the focus inevitably shifted onto

AT&T(NYSE: T) and what it would be

saying over spending. Going into the results there was a certain amount of hope

and trepidation. Hope because it had previously excited the telco

industry by outlining its plans to step up spending over the next few years.

Trepidation because other tech companies have been warning of weak spending by

the service providers. It looks like the pessimists won.

AT&T Giveth and AT&T Taketh Away

AT&T declared that it was keeping its capital expenditure forecast at $21

billion for this year but reducing it to $20 billion in 2014 & 2015 from $22

billion previously. Moreover, its subscriber numbers and revenue

trends were disappointing, and the stock fell heavily on the day of the results.

Nor was there any let up in the negative commentary over the levels of caution

being exercised by the enterprise sector. Verizon had argued that its enterprise

customers were being very cautious and still stuck in cost cutting mode.

AT&T said pretty much the same thing.

So it is a story of a weaker trading environment coupled with

less spending by the major carriers. This is not great for the service providers

and neither is it good news for the companies that supply them. While AT&T

is not the only telco carrier out there, it is a huge company whose conditions

do strongly reflect overall market conditions.

The usual bugbears were mentioned: persistent unemployment,

regulatory fears, political instability, government budgets etc.

Frankly I’m coming round to the view that there is a bit more

going on here, and the clues are in what the major carriers are saying about

trends within their operations.

Simply put, things like smartphone penetration, cloud based activity and the

shift to wireless from wireline services have increased in a quicker fashion

than many companies had expected. It is a case of the good, the bad

and the ugly. The good is the margin and revenue generating opportunities

inherent in increasing smartphone penetration (they churn less, use more data

etc). The bad is the implied loss in wireline revenues and small business

choosing not to use them. And finally the ugly is the period of uncertainty that

accompanies businesses when they adjust to unforeseen events. I want to talk

more about the last point.

Certain Uncertainty

Apologies for going all ‘Donald Rumsfeld’ on you, but it’s the best way to

describe the essence of the big question in technology investing. In other

words, what effects will the rate of technological change have on my

business?

A classic example of this--and it relates strongly to the

telcos--is Intel(NASDAQ:

INTC). The company

does face criticism for not being prepared for the shift to tablets and mobiles,

coming late to the LTE party and being too optimistic over a potential demand

pull from Windows 8. It’s easy to criticize, but it’s a lot harder to predict

these changes. Anyone who scoffs and says they can should show me how they

invested in these trades, because that is what really matters here.

So just as Intel found itself structured for a world and cycle that didn’t

look like it had before, so the telco service providers have also seen the same

challenges. It’s certainly true that they have been pushing out these services

(Verizon started investing in LTE over five years ago), but when AT&T cuts

its capital spending forecast by around $4 billion (or 9%) for 2014-15, it is

obvious that something has changed.

The reasons given for the cut are that it got better deployment from LTE than

it had previously expected. Its much vaunted Project VIP includes a commitment

to expanding 4G/LTE to 300 million points of presence (POPs) by the end of 2014.

The good news is that it expects to achieve 90% of this figure by the end of

2013. The bad news is (from the suppliers point of view) that this greater

efficiency is lessening the necessity for spending. It is also

shifting spending into newer technologies and away from legacy systems. Again

not good for the suppliers.

Where Next for Telco Spending?

Unfortunately it looks like a similar year to 2012 for the telco suppliers:

some hope in the first half which then evaporates into a weaker second half.

Some of the weakness in Q1 will possibly turn out to be temporary, but when

there doesn’t appear to be a major stimulus for increased spending by Verizon

and AT&T is cutting future projects it is hard to be too optimistic.

On a more positive note the increasing adoption of newer technologies like

4G/LTE, high bandwidth capability and corporate mobility solutions will surely

spur other telcos to invest in them, so the focus on investing in the sector in

2013 must be in these areas. The problem is that the telco suppliers are not

constructed to surgically target these areas alone. In conclusion If you are

bullish on the telco sector it probably makes more sense to stick with investing

in the carriers right now. The floodgates of telco spending aren't open yet.

I would rather forget last month. After nine months of gains, I hit a

nasty double digit loss. In truth, this sort of thing was inevitable

and the preceding months were as much a part of the process as last

month was. The previous month’s write-up and links to others can be found here. I do this stuff because I happen to believe that anyone writing about investment should disclose his own performance.

Philosophizing over, I'm going to confess to a certain amount of exasperation at being hit with accounting errors with Ixia, a weaker than expected tax return season at Intuit, the loss of a major customer contract with Regal Beloit, and when even Pfizer disappoints then you know it’s not going to be your month.

The weakness at IBM and Citrix Systems

was a bit more predictable and I topped up on both. I suspected tech

would be weak over earnings and held back buying more before their

earnings.In fact, this approach helped me avoid disasters in companies I like and have held before, such as Fortinet and F5 Networks.

It was definitely a month of dodging bullets! I’ve put some performance

charts at the end of this post for those interested. I will update my

current portfolio on my blog in a few days.

For now, it’s the usual format of reviewing the articles for January

(i.e. three months previously) and picking out some investing ideas that

readers might find useful. The companies in bold are those that I hold

now. Acuity Brands was sold because it hit its price target.F5 Networks was sold because it hit its target and my general tech caution.

Superficially these numbers look good, but let’s recall that the

S&P 500 has put on over 12% in 2013. The ‘buy’ stocks averaged 6.8%,

‘positive’ recorded (0.6)%!, ‘evaluation’ returned 7.7%, and ‘caution’

did 0.4%. The difference between what I bought and didn’t was 6.8% to

1.9%.

Some observations and conclusions

It’s been a relatively tough period for tech stocks like Fortinet, F5 Networks, IBM, and Citrix,and cyclicals like Dover, Fastenal(NASDAQ: FAST) and MSC Industrial.

The defensives are starting to look fully priced with nice gains for Cooper Companies and Perrigo.

Tech ‘value’ ex Intel and Check Point Software(NASDAQ: CHKP) has held up better than the growth tech stocks.

Nothing but nothing seems to stop the market wanting to buy yield with stocks like Johnson & Johnson and McDonald’s.

In conclusion, think it’s time to start thinking about buying some select industrial and/or technology stocks.

Some stocks to consider

With these thoughts in mind, I think Intel(NASDAQ: INTC) and Check Point Software are worth a look.I’ve covered both after their recent results in articles linked here and here.Intel

is a curious beast in the market place. It offers a high yield, good

value, and cyclical exposure to consumer electronics, but it is also

faces long-term challenges from ARM core processors. It also offers a

restructuring story as it adjusts to the shift in computing devices. Gross margin appears to be bottoming and while it hasn’t turned the corner yet ,the potential upside in the stock remains.

As for Check Point, in retrospect, its last results were okay and

there are some signs that its customers are more willing to buy its new

products. Like Intel, it offers a genuine value proposition because of

its high cash conversion and potential to leverage its technology into

expanding its sales. On the other hand, I think the market is tired of

seeing falling product and license growth and a ‘cash harvesting’

approach to its business development.If that should change, I’m sure the stock will go higher.But will it?

The next two stocks are both industrials. I still think Fastenal is

expensive and am concerned with the falling sales growth, but if you are

looking for some short-term upside from the idea that industrials will

come back then, it is a great stock to look at. Its visibility is

limited and it is exposed to short cycle decision making by purchasers,

all of which leaves it susceptible to violent changes in sentiment by

its customers. Bad when it’s bad, good when it’s good.If you like the industrial space and want a near-term play, then Fastenal is worth picking up

Another industrial worth considering is PPG Industries(NYSE: PPG). I like its end market exposure

and its purchase of Akzo Nobel’s U.S. household paints division.

Aerospace and automotive are the two stand out sectors within

industrial, and PPG is well placed in both. Its long-term dividend

record is excellent and it is a very good generator of cash and has the

potential to generate some synergy-based cost savings with the

acquisition.Despite reporting a good quarter -- notably

better than so many other industrials -- the stock has lagged the

overall market and looks decent value. I may pick some up.

The last stock for consideration is Capital One Financial (NYSE: COF).

The stock has underperformed this year and the credit card companies do

face challenges to net interest margins thanks to low interest rates

and the maturing of higher rate loans. Moreover, the weak recovery has

left the yield curve relatively flat and loan demand is not where it

usually is at this stage of an economic recovery. No matter, if you

believe that employment will keep increasing and the recovery is

ongoing, then at some point demand will come back. Meanwhile, asset

quality and delinquency rates carry on improving so Capital One is well

positioned to catch an uptick in end demand.

Additional data

As discussed above, here is how this lousy month affected performance

since inception. The blue line is my portfolio the red line is the

S&P 500.

Earnings season is starting to wind down, but we still have some

interesting companies reporting this week. Since we are nearing the end

of the season a lot of these companies’ peers will have already

reported, so the market will be anticipating the direction of the

results. I’m going to use this approach to preview what investors might

expect from the results this week.

Tuesday

I can think of very few sectors as unglamorous as painting and

coatings, but who cares? Anyone purely focused on making money couldn’t

help but notice that these stocks have been hot over the last year or

so. Valspar (NYSE: VAL) will give numbers, and following the recent solid results from Sherwin-Williams and others we can expect similarly good numbers here. However, it is somewhat a story of a two different markets.

The US consumer market has been strong--in line with an improving

housing market--but industrial coatings have been more varied. The key

thing to look for in these results will be how its mix of geographies

and end markets are holding up. The industrial sector has been mixed so

far this year, with areas like automotive and aerospace strong but

general industrials growing weaker. Indeed, Valspar reported weakness in

food and general line packaging last time around. Given the more

positive news out of China recently we could see a bounce back.

Wednesday

A couple of bellwether’s report on Wednesday, with Deere outlining the state of play in farming and construction machinery, and Macy’s will be discussing high end consumer spending.

Thursday

Thursday is undoubtedly the most interesting day of the week. Bring your own device (BYOD) play Aruba Networks(NASDAQ: ARUN)

has already pre-announced and disappointed by missing estimates and

guiding lower. Frankly if you don’t know that the telco and enterprise

technology sector has been weak in Q1 then you aren’t invested in

technology. Company after company has pretty much repeated the mantra:

customers are reluctant to sign off on big deals but the pipelines

remain in place, etc. It is disappointing, but the correct tactic has

been to buy after the crash. This is why the color around Aruba’s

conference call will be so important. Investors will want to discern

whether this is a company-specific issue or a macro one. If it is the

latter then the stock can recover strongly given a cessation of

sequester/macro fears. Unfortunately at this point it is hard to tell

the difference.

Autodesk(NASDAQ: ADSK) is a company I’ve discussed at length in an article linked here. Frankly it is very hard to predict what it will report.It

is a company with an enviable record of beating its guidance, so when

it misses the stock gets trashed. If you follow the general‘tech

is weak in Q1’ approach then you should be braced for a miss. On the

other hand, certain industrial sectors have been strong in Q1.

The question is does Autodesk have enough exposure to areas like automotive and aerospace?Moreover,

it has long term secular growth prospects from the shift to a software

as a service (SaaS) based company, and this should provide sales

support. The one thing I’m sure of is that the stock will be volatile

over the results. Its internal guidance is for $570-590 million in sales

and Non-GAAP EPS of $0.41-$0.46.

Two vastly different retail names also give results. Wal-Mart is about as mass market as you are going to get, but Nordstrom Inc(NYSE: JWN)

is arguably more of a high end play. It’s a company with a well

regarded management team that it engaging in every initiative it can to

generate future growth in the face of a difficult consumer environment.

There is an outline of its growth strategy in an article linked here.

Nordstrom is expanding its lower priced Rack stores and investing

heavily in its e-commerce facility and in store Point of Sales

offerings. Over the next few years its revenue streams will be

substantially changed. The key questions are whether this will

cannibalize or denigrate its existing brand and if the investment

program will be executed successfully. For the next few years it is all

about investment for Nordstrom, and investors should focus on this (and

its effect on margins) in the upcoming results.

Friday

Friday’s are usuallyquiet days, but I’m interested to look at industrial filtration company Donaldson (NYSE: DCI).

Its prospects are largely dictated by conditions in China. Its exposure

to transportation and industrial products (with a heavy weighting

towards construction machinery) will always mean it is a cyclical play.

Construction, mining and heavy trucking are problematic end markets

right now, and investors have seen the point of an anticipated pick up

being pushed out to the end if 2013 in previous reports. The key thing

in the upcoming results will be the commentary over the recovery in

China and where the country’s stimulus spending will be directed. In

general it has been a weakening environment for its industry

bellwethers, with Caterpillar and Joy Global both struggling to

convince. On the other hand, Alcoa reiterated its guidance for 2013 within China, and since this implies 12%-16% growth in its Chinese heavy truck and trailer division, I think this bodes well.

To be or not to be? To buy or not to buy? That is our question with The Estee Lauder Companies .

Whether it is nobler in the mind to suffer not buying a stock that that

the market loves, or to take arms against a high valuation, revenue

forecasts at the bottom end of guidance, and a management initiative

that thus far isn’t quite going as planned? The good news

is that unlike Shakespeare’s Hamlet not everyone is going to end up

being murdered--but, being the maverick type, I favor raising arms

against Estee Lauder's evaluation.

Estee Lauder’s growth prospects

I can understand why the market loves this stock and why it is

willing to award it an valuation of nearly 24 times earnings to June

2014. The company has a number of attractive growth drivers:

An aging demographic and cultural trends that will ensure the skin care business has good long term growth.

Strong emerging market growth prospects.

On a relative basis Estee Lauder has more focus on prestige brands than mass and is better placed than, say, Revlon or Avon Products to benefit from the two-tier recovery whereby the high-end fares better.

Unlike Procter & Gamble ,

it is a more beauty-focused company and should find it easier to

innovate and react to changing consumer trends. This is incredibly

important as more cultures become a bigger part of its clientele, and

unlike Nu Skin Enterprises it is relying on a traditional sales channels rather than multi-level marketing.

A strategic management

initiative (SMI) is intended to considerably increase inventory

management and therefore cash flow and return on investment. A key part

of this is a SAP deployment.

Putting these things together creates a powerful case for the company.

On the other hand, these drivers have been known for some time. I’m

not convinced that Estee Lauder is a good value or is outperforming to

the extent that the market is rewarding it.

Estee Lauder’s performance could be better

For brevity’s sake I should note that I covered the stock previously in an article linked here for anyone looking for a primer or background. I have three main points to make on why I think it could do better.

First, the SMI was supposed to produce significant cost savings and

improve its operational metrics. This is already happening, but by some

measures we could have hoped for a bit more. In the previous article I

discussed how Estee Lauder was hoping to increase inventory turn to 3x

from 2x. In simple terms this just means it holds relatively less

inventory and can decrease working capital requirements accordingly.

Ultimately this would help increase cash flow.

Its performance over this issue is best expressed in a graph. These are my calculations based on company data.

I realize that I am probably being a bit harsh here – it is early in

the SMI -- but we are still a ways away from the 3x figure. This is a

metric worth following because it will guide cash flow in the future.

Secondly, the SMI has caused some short term customer service

challenges, which led to some delays and products out of stock.

Management claimed that these problems were largely dealt with and were

expected to have been resolved by the end of the quarter, but I note

that the next wave of the SMI roll out has been delayed by six months.

The SMI is not entirely going as planned.

And finally, the full year revenue guidance has now been moved to 6%,

which is at the lower end of the previous guidance of 6%-8%. The reason

cited for this was that the overall market is now predicted to grow 3%

instead of 5%.

What the industry is saying

Revlon is more exposed to the mass market and it is suffering

accordingly. While declining sales in Europe are expected, the slowdown

in its Chinese sales (in line with the economy) is more

disappointing. Its Asia Pacific sales declined 2% mainly due to declines

in its color cosmetics in China. This is not a good sign in a market

that is supposed to provide its long term growth prospects.

Similarly, Procter & Gamble recently announced a net sales

decline of 2% in its beauty segment. Organic volumes and sales were down

1% each. The company cited a heavy competitive and promotional

environment in hair care and skin care, although sales increased in its

salon professional sub-segment. This is further evidence of a

bifurcation between the prestige and mass market. In fact, Procter &

Gamble faces challenges in keeping market share in all of its

categories.

The last two companies are somewhat less reliable indicators. Nu Skin

has been reporting strong growth but I think this company is partly

reliant on keeping its distributors active and motivated. Avon is in the

middle of a restructuring program that will take time. Indeed, sales

are still declining in the US and China. Avon is more of an internal

restructuring story.

It is not a positive industry score card, and near term conditions do not look great for Estee Lauder.

The bottom line

In conclusion, while I think the company has good long term

prospects, it is hard to argue that it is a good value. Moreover its

near term prospects (despite the hike in EPS guidance) appear to have

gotten worse. The market is giving it the benefit of the doubt for now

but, I’m not sure it's time to follow it.

A few weeks ago IT security company Fortinet $FTNT

helped kick off a pretty dismal reporting season for technology by

pre-announcing a weak set of results. Since then a plethora of other

companies have reported and given a myriad set of reasons and excuses

for missing. I think it’s fair to conclude that there was a marked

reluctance among business to sign off on large tech deals in the

quarter. Given that this could be temporary, is it now time to start

buying these names? And with Fortinet, what does its new guidance entail for 2013?

Fortinet Updates the Market

Before going into the color I want to outline the full year guidance changes.

The guidance changes are pretty significant but I think that if they

are hit then Fortinet will be higher by the end of the year. As I write

the Enterprise Value of the stock is around $2.4 billion. I’ve followed

this stock for a while and never seen it trading on a forward free cash

flow over enterprise value (FCF/EV) of around (145/2400)=6%. The reason I

highlight this metric is to compare it with very low Government bond

yields.

It is arguably cheap on this basis alone. Furthermore consider the

new guidance was based on a continuation of the weak trends in Q1

continuing in Q2 and most notably coming from U.S. service providers. So

if you think this weakness will prove temporary then there could be

upside to come. On the other hand my concern is that the guidance

appears to imply some pretty optimistic assumptions for the second half.

Is Fortinet’s Guidance Achievable?

Consider that Q2 revenues were guided towards $143 million at the

mid-point with $135.8 million reported already for Q1. This makes $278.8

million for H1 but the full year guidance is for $600 million. In order

to see what this implies I have included the Q2 guidance plus my

guesstimates for what Q3 and Q4 are implied to be.

I’ve assumed that Q4 will contribute 28.3% of revenues as it has done in the last three years. The Q3 and Q4 numbers are my estimates.

As you can see the implication is for a pretty concerted resumption

to growth in the second half and I’m not entirely clear how this can be

accepted categorically given the weakness in H2.

Furthermore here is how these numbers look on a sequential basis.

From this graph it looks like the Q3 and Q4 assumptions are for ‘same

again’ sequential growth. Fortinet may well do this but given that Q1

& Q2 are notably weaker it does seem to imply a return to better

conditions.

Why Was the Q2 Guidance So Weak?

I must confess I was hoping a bit more from Fortinet than it gave in Q2 guidance. If you go back to the analysis of the Q1 results

there were three reasons given for the billings miss of around $12

million. Fortinet attributed $6-9m to service providers, Latin America

missed by $4-6m and there was an inventory shortage (due to product

refresh) which caused a $2 million-4 million miss. The

last two issues were believed to have been able to rectify in the

short/medium term thanks to new management and better execution, with

the service provider issue being more problematic. However

in the latest statement Fortinet basically said that conditions

remained the same in Q2 as Q1. Rather confusingly Fortinet cited

challenges in Europe even though a few weeks ago it said Europe was only

a bit weaker.

With regards the telco service providers, there can be little doubt that they have been reluctant to spend. F5 Networks $FFIV also reported very weak numbers from its key telco vertical . My suspicion with F5 is that its problems are a combination of weak telco spending, the success of Citrix Systems

with its rival Netscaler product and the difficulties in protecting its

dominant market position within the application delivery controller

market. For F5 and Fortinet the following graph of the latter’s deal

breakdown reveals a lot.

I think there is a case for a ‘budget flush’ in Q4 which caused some

overdue optimism and lets recall that the previous quarter contained

worries over the fiscal cliff while Q1 saw a lot of attention over the

sequester. Telco customers tend to do large deals and it wouldn’t

surprise if this boils down to a few deals that didn’t close in Q1. So

will future quarters bounce back?

The Competitive Environment?

Looking back at the recent results in the quarter I thought Check Point Software(NASDAQ: CHKP)reported a mixed set of results.

While Check Point probably needs to generate some product and license

sales growth to truly convince, in the light of what the rest of the

industry has reported its results are starting to look good. The good

news is that yearly comparisons are likely to get easier going forward

even if the company doesn't seem to ready to shake off its 'cash flow

now but investors wont see any of it' image.

Amongst the discussion of the deal commentary it mentioned winning a

seven figure contract with U.S. wire based carrier and replacing Palo Alto Networks(NYSE: PANW) as a consequence. In addition it won a large U.S. deal with a global retailer and beat out Check Point, Palo Alto, Juniper and Cisco

in the process. These sorts of wins (and other large deals cited in the

commentary) are actually quite impressive because Fortinet is coming

from a position as being known as primarily a SMB focused company.

For Palo Alto this sort of thing must be a concern because as a young

and fast growing company (with an evaluation top match) it is not a

good thing to see others replacing it with security solutions.

It has a lot of expectations built into its evaluation. Moreover its

solutions are not known for offering a value proposition so given any

kind of discounting in the industry it could see its margins cut.

F5 only has security as a very small part of its revenues (and only

really in the data center) but many of its customers are in common with

these companies and if CFO's have decided to 'go slow' then it will get

hit accordingly. My only concern with F5 as a recovery play is that it

is undergoing a product refresh which might take a quarter or two to

fully filter in. We shall see.

Is Fortinet Worth Buying Now?

As the charts indicate the guidance assumes somewhat of a bounce back

in the second half and there are some internal opportunities (Latin

American leadership and inventory shortages) which can be rectified but

the key issue will be with telco spending.

The good news is that we can keep an eye elsewhere at what other

companies are seeing. It has been a miserable reporting season for most

companies selling into them and cautious investors might want to wait

until one or two companies with telco exposure start saying better

things.

V.F. Corp

is one of those infuriating stocks that never seems to be cheap

precisely when you want it to be. The latest set of results kept up its

tradition of raising EPS guidance even if the revenue numbers were far

from stellar. Indeed the key takeaway from these results was the margin

improvements achieved within difficult end markets. This is one of the

best run stocks in the retail sector, but it faces some headwinds in

2013. Is it good value right now?

V.F. Corp Prospects and Challenges

With its key brands of The North Face, Vans, and Timberland the

company has benefited from the trend towards wearing outdoor sports

clothing as a kind of fashion statement. I doubt that most people

wearing mountaineering or hiking clothing have ever been on a climb or a

trail. Moreover wearing Vans and listening to Sonic Youth doesn’t

necessarily qualify you as bona fide skate boarder, but who cares as

long as it adds to the bottom line of the company’s numbers.

In order to explain how Timberland makes money here is a breakdown of

its segmental profits in Q1. The key brands are in the outdoor &

action sports wear division.

Throughout 2013 the company is going to be faced with the following challenges

Timberland’s has significant exposure to Europe and markets like

Italy and Spain are some of its biggest existing markets. Fortunately,

Vans and The North Face were ‘built out’ of Northern Europe.

J.C. Penney is a key retail channel and in

particular with Lee jeans and Vans. The difficulties with the department

store and ongoing restructuring efforts could affect sales generation.

It’s Chinese operations haven’t performing great and it is a key part of its international expansion plans

In general the mid-market consumer is challenged in the current

environment. It offers neither the income secure spending of the high