This blog is devoted to helping investors make informed decisions. It will be regularly updated and provide opinions on earnings results. It is not intended to give investment advice and should not be taken as such. Consult your investment advisor.

The market gets what the market wants and, for the first quarter of

2013, the market has wanted relatively (as compared to treasuries) high

yield ‘defensives.’ I use inverted commas because when looking at a

stock like McDonald’s (NYSE: MCD)

I’m not convinced it is as attractive as the market thinks it is.

Furthermore, if you buy a stock because it is fashionable then you

better be prepared for any disappointment should fashion change.

McDonald’s Disappoints

It’s been a tough year for the fast food sector, and McDonald’s

delivered another quarter of disappointing same store sales growth.

Moreover, it described the informal eating out industry as being flat or

declining in many parts of the world. So where did it all go wrong?

Wasn’t this supposed to be the great defensive stock that proved itself

so well in the last recession?

My take on this is that the 2008-09 recession certainly resulted in a

significant amount of global unemployment and income insecurity, which

fed through into consumers trading down and adjusting their behavior by

dining out in cheaper outlets. Such conditions played perfectly into the

hands of companies like McDonald’s and Yum! Brands (NYSE: YUM). In addition they had growth opportunities in expansion into China.

Fast forward into 2012 and the trading down has run its course and

suddenly comparables are getting a lot harder. The easy growth has gone

and the challenges are building. Sales growth from China is slowing, and

McDonald’s is having problems adjusting its menu to deal with the

slowdown in Europe. I discussed some of these issues at the start of the year.

A look at its global comparable sales growth for the last few years.

Spot the slowdown?

Market Share Gains

While recognizing that the US market is tough, McDonald’s spent a lot

of time trying to convince investors that it was gaining market share

in the US. The idea is that the key to its long term growth

would be the retention of market share and not necessarily margin or

cash flow growth. It’s hard not to think that this is going to have an

effect on Yum and Burger King(NYSE: BKW) in the US.

But this isn’t just about the US. The optics in China are becoming

cloudy thanks to a combination of the chicken supply problem at Yum’s

subsidiary, KFC, and a later outbreak of Avian flu. All of which has

caused issues for the rest of the fast food outlets in China. While this

is causing some to believe that there is an inbuilt opportunity to

bounce back in the second half of 2013, I’m not so sure. If you look at

the chart above, McDonald’s APMEA growth was slowing well before these

issues kicked in. Indeed, it was a similar story with Yum, so this isn’t just a story of some temporary weakness.

So even while China’s performance is uncertain, there is no let up in

investment with McDonald’s planning to open hundreds of restaurants in

China in 2013. Similarly Burger King wants to open 1,000 stores in China

within the next seven years, and the country is the focal point of

Yum’s growth plans. Obviously these companies wont adjust their long

term strategic plans based on some temporary weakness, but might it

prove a longer term issue?

As for Europe, despite previous efforts to take action in France and

Germany conditions remain weak in Europe, and macro challenges in

Southern Europe mean that growth will be hard to come by. Only the UK

and Russia are performing in a manner that McDonald’s can be happy with.

Where Next for McDonald’s?

I think this is going to be a tough year for the company.

Commodity costs are only forecast to go up 1.5-2.5%, but the real driver

of earnings growth will be sales growth. Given that the stated strategy

is to preserve or gain market share, it is hard to see any significant

margin expansion this year. There is a lot of uncertainty with China,

Europe remains in difficulty, and the US is becoming increasingly

competitive. In conclusion it is hard to make the case that McDonald’s

is the kind of defensive play that investors should be chasing, and if

the market loses its fixation with yield then it might not be so well

supported.

We are still early in earnings season but already there are signs

that corporations have been affected by a sense of caution in the

quarter. Of course these things are part and parcel of an uncertain

political environment, and long term investors usually see them as

decent buying opportunities. The problem with this approach is that when

companies start reporting disappointments it will look similar to what

they might say going into a protracted slowdown.So what to make of Verizon's (NYSE: VZ) latest results?

Irrational Melancholy

Investors had a right to be cautious going into these numbers. After alltwo leading tech companies had already warned of slowing spending by their telco customers.

Firstly, Fortinet(NASDAQ: FTNT)

warned that telco service providers were being cautious over closing

deals in the quarter and, in particular over larger deals. On a more

positive note, it argued that some customers were switching from a

'CapEx to OpEx’ spending mentality (so revenues might be more spread out

in the future for Fortinet) and that the problems were not due to competitive losses.

I also think there could have been an element of ‘pull forward’ in the

previous quarter because Fortinet reported a very strong number of

larger deals in the previous quarter.

Secondly, F5 Networks(NASDAQ: FFIV)

also warned of a weak telco vertical. What is puzzling is that both

companies reported decent enterprise spending. In the case of F5’s core

application delivery controllers (a market that Fortinet has also

recently entered by buying Coyote) telco carrier spending was far less

than expected. Indeed, if you look at the details

F5 reported strong numbers from telco customers in the previous quarter

however, they did not follow through as planned in the last quarter.

Putting these things together, there are two scenarios that investors need to consider.

Is it the (bullish) case that

there was a pull forward in telco spending at the year-end due to a

budget flush effect, and all we are seeing now is a natural reaction to

that which will get smoothed out in future quarters?

Alternatively, are the bears right and there is something unduly

negative going on in the telco market causing a change of sentiment?

It’s time to look at what Verizon said.

Verizon Delivers a Mixed Prognosis

It is hard to give a definitive answer to the questions above. If it was easy then it would already be priced in!

On the bullish side the transition to newer technologies and services

continues to accelerate at Verizon. The company started investing in

4G/LTE networks over five years ago and rolled out its network far

quicker than AT&T(NYSE: T).

It obviously has less need to invest now, and as the following graph

demonstrates Verizon did its heavy lifting in next generation networks a

few years ago while AT&T is playing catch-up.

Moreover, Verizon is seeing increasing penetration from smartphones

(up to 61% from 58% at the end of the year), and given that 38% of the

customers upgrading to a smartphone in the quarter were first-time

users, the potential for rapidly increasing bandwidth utilization should

be obvious. Verizon wants to do this. 4G/LTE smartphones already

represent 40% of the smartphone total and 54% of its data is being

carried on the 4G/LTE network.As more customers upgrade

it will drive growth at other carriers, and the pressure on the industry

to spend on telco infrastructure must increase as a consequence.

On the bearish side Verizon spoke of ongoing caution among its enterprise customers.They

still don’t appear keen on committing to capital spending, and the

environment continues to be one of cost cutting first rather than

investing for growth. Some sequester-related weakness in government

spending was expected and it didn’t disappoint, but the ongoing caution

among enterprises was a bit surprising.

Indeed, hopes of an upside to telco spending in 2013

still largely rest on Tier 1 carriers like AT&T investing in new

networks as well as emerging market telcos starting to invest too. In my

view the outlook for legacy telco spending has gotten a bit weaker recently with companies like Spirent disappointing with their legacy systems sales and noting that customers seemed minded to jump to higher bandwidth solutions.

The Bottom Line

In conclusion, the underlying trend of smartphone adoption and the

proliferation of bandwidth-rich devices and applications continues

apace. On the other hand, Verizon’s commentary continues to exercise a

note of caution over enterprise spending and until it and AT&T talk

of some sort of improvement there it would be churlish to conclude that

happy days are here again for telco spending.

Those of us that think, and are invested in the telco spending theme,

are left to sulk in the corner and wait for AT&T (which is expected

to spend more this year) and others to report better things before

going overweight on the idea. It’s more jam tomorrow I’m afraid.

t’s rare that I recommend watching a movie in order to try to

understand investing, but in this case I strongly suggest finding the

time to look at the late great Akira Kurosawa's masterpiece ‘Rashomon.’

The film is about the relativity of truth and depicts how three

different people recall (in contrasting fashion) what is broadly the

same event. Tech investors will have an inkling of what I ‘m talking

about already because IBM (NYSE: IBM)

became the latest company to disappoint with earnings. The problem is

that the reasons for these misses are becoming ever more varied.

Time Heals Everything

IBM’s great rival Oracle(NASDAQ: ORCL) also gave weak results recently and insisted they were largely due to sales execution. Fast forward a few weeks and Fortinet (IT security) and F5 Networks (application delivery controllers) both argued that their telco verticals were weak in the quarter. Red Hat missed estimates and Verizon discussed an ongoing cautious spending environment amongst enterprise customers. TIBCO Software(NASDAQ: TIBX) missed and guided lower and gave its--now all too familiar--refrain that its sales execution wasn’t up to scratch but

that it would all be sorted out soon enough. Although frankly I think

it would be just as interesting to now hear what the sales guys said

about the management.

Just as with Rashomon, all we do know now is that we

have dead body on the scene even if the exact story isn’t entirely

clear.The good news is that we can get a bit more detail from the crime

scene.

Let’s put it this way: if it truly is a question of a bit of excess

caution being caused by political uncertainty over the sequester

(Oracle’s quarter end fell on the deadline) then as companies report

through the ongoing earnings season we might expect to get a bit more

color on any pick-up in demand. Indeed, I think IBM may well have just

done that.Oracle’s numbers ran to the end of February while IBM’s ran to the end of March. A lot can happen in a month.

Who Said What

In essence Oracle said that it expected to bounce back

in its Q4 and that the pipeline was up significantly. Its miss was

largely a result of sales execution and timing issues rather than

competitive losses or businesses walking away from future deals or even

trying to reduce the size of them. TIBCO said a similar thing.

Fast forward to IBM, and in the latest report we hear about issues

relating to sales execution, the timing of Easter, the sequester, $400

million of software and mainframe revenues rolling in to the next

quarter, the weather and even the change in the Chinese Government.

The conclusions of which led to some disappointing revenue growth numbers for IBM in the quarter.

Superficially it is worrying, but unless you believe that all these

tech firms (TIBCO, IBM and Oracle) have suddenly seen their sales

managements lose the ability to sell, then the real cause of this

slowdown in tech spending (and I think it’s time to call it that) is

probably due to some caution around the sequester. IBM reported in

September that orders had fallen over a cliff only to see a nice rebound

in the next quarter.

Furthermore, none of these companies are blaming the macro

environment or seeing their pipelines diminish, so if you are bullish on

the economy then there is every reason to expect that this order

weakness will prove temporary.

The Bottom Line

I think my line of argument applies to all three companies, but they

differ in their attractiveness. Frankly, TIBCO really needs to report a

couple of good quarters and regain investor confidence.It

appears to have more issues than just sales execution. Oracle is

attractive in this viewpoint, but longer term it faces risk as it

refreshes its hardware. It also has to demonstrate that it can continue

to be as dominant in the cloud based era as it is with on-premise

For IBM, the response to the weak quarter is to take some workforce rebalancing in Q2, and if recent reports are trueit is prepared to sell some low margin hardware businesses. All

of which is in line with its long term objectives to go for margin

improvements by divesting and reducing lower margin sales. Even in this

bad quarter IBM managed to increase gross and operating profit margins.

Moreover, despite the weaker numbers this quarter it didn’t lower its

full year earnings guidance. The company is still forecast to deliver

double digit earnings growth in the next couple of years while

generating huge amounts of cash flow. I think the sell-off is a decent

buying opportunity so I bought some more.

Anyone who has watched the classic sales movie Glengarry Glen Ross or

worked in sales will know that the acronym ‘ABC’ stands for ‘always be

closing.’ However anyone who hasn’t and instead has solely listened to

US blue chip conference calls over the last few years will probably

conclude that it actually stands for ‘always be cost-cutting.’ In other

words, investing for growth is still on the back-burner in favor of

pruning and consolidating measures made in light of uncertain end

demand. Such considerations came to mind when considering General Electric’s $GE latest results.

A mixed Industrial Environment

The earliest indication of how the industrial sector was faring was outlined by Alcoa $AA

recently, and it was pretty positive in my view. Other than a slight

weakening of its European automotive outlook, Alcoa kept its end markets

prognosis constant. However, on closer inspection it is clear that

Alcoa’s growth prospects in 2013 are highly reliant upon China. In

addition it is exposed to a few industries that are doing relatively

better.

As this article demonstrates,

global aerospace is doing well with airlines surprising on the upside

and passenger growth numbers growing at a decent clip. This is obviously

good news for General Electric and its aviation segment. In addition,

Alcoa’s North American outlooks for its automotive and commercial

building & construction segments respectively were for 0-4% and 1-2%

with China growing up to 10% in both. Europe is expected to decline in

both of these segments. So while China is doing well and some global

industrial sectors are doing okay, it is far from a universal situation.

More evidence of this divergence in the industrial sector can be gleaned from looking at what the industrial suppliers like Fastenal and MSC Industrial are saying. Aerospace and auto are fine but elsewhere there was weakness in Q1.

What GE Said

Fast forward to GE’s latest results and the company reported that its

industrial segment profits were $200 million lighter than had been

expected largely due to Europe being weaker than forecast. The power

& water segment was particularly affected while elsewhere GE

reported some reluctance to close orders in a few of its shorter cycle

industries. Again, the latter statement correlates with what the

industrial suppliers (who are as about as short cycle as you can get)

indicated.

In order to see the relevance of the power & water segment here

is a breakdown of GE’s segmental profitability in the quarter.

As the chart indicates the industrial segments that increased

profitability were aviation, healthcare and transportation. GE capital

profits improved in line with its rationalization strategy. Overall

segment profits were down 4%, but net earnings rose 16% thanks to lower

charges and eliminations.

See what I mean about ABC? Indeed, the immediate response to the

weakness in the quarter was to announce more cost cutting measures. Plus

ca change and all that.

What the Results Mean to The Market

Another area of interest was US healthcare, which GE said was a bit weaker than expected. Investors got an early read on this when Johnson & Johnson

gave results and noted (within its medical devices and diagnostics

segment) that US hospital procedures were weaker than the hospitals had

forecast going into 2013. In addition hospital spending wasn’t as

strong. It’s nothing dramatic for Johnson & Johnson

because it has plenty of other profit drivers within pharma and consumer

products, but for a company like Varian Medical Systems $VAR it is a cause for concern.

I like Varian, and based ona SWOT analysis

think it has some very impressive long term growth prospects with its

proton therapy solutions. In the near term it can expand its radiation

therapy into indications like lung cancer, particularly within emerging

markets. In addition its new deal (GE was its former partner) with Siemens (which

is pulling out of radiation oncology) gives it a large installed base

on which to target. On the other hand its systems require significant

outlays, and with Johnson & Johnson and GE reporting some weaker

conditions, can we really expect immediate upside from Varian?

On a more positive note GE forecast that its oil & gas and home

& business segments are going to be ‘pretty solid’ for the year.

Within the latter segment one of its key rivals is Whirlpool $WHR

I think Whirlpool has good growth prospects in 2013. The US housing

market is recovering, and Whirlpool is starting to anniversary the

housing boom of 10 years ago. In other words, the white goods purchased

back then should have depreciated by now and a replacement cycle should

kick in. Furthermore, GE reported good results in emerging markets so we

have reason to believe that Whirlpool will do okay in its key Brazilian

market.

Where Next for GE?

Cost cutting isn’t sexy, but it does represent a key bottom line

opportunity for GE this year. Europe was weaker than expected but

China’s strength was a welcome positive note. As noted above GE’s end

markets will be variable this year with areas like aviation,

transportation and health care (especially in emerging markets) likely

to remain strong and counteract areas more exposed to austerity measures

like US military spending and European infrastructural spending.

Investors looking for a more focused exposure to their favorite

end markets will not buy GE because of its diversification, but those

looking for a 3.5% yielding global GDP type play will view this mini

sell-off as a buying opportunity.

Investing in Intel

is a bit like betting on an old and slightly out of shape, but hard

hitting fighter. Mr. Market keeps landing quick jabs and slows his

opponent down. The odd cheeky hook to the body gets slipped in, and your

fighter starts to slow and look out of place. He is way down on points

by the middle rounds, so, he starts throwing haymakers, and commentators

scoff about the superior mobility of the other guy.

The quicker opponent comes out confidently in the eighth round,

throws a few jabs, and then gets caught square on the chin by an

overhand right from your guy. Ten seconds and a medic later, the

ringside journalists start re-writing their reports to reflect how

‘clever’ Intel was with its strategy.

Intel fights on

Frankly, the company has had its fair share of jabs in the last year and I looked at some of them recently.

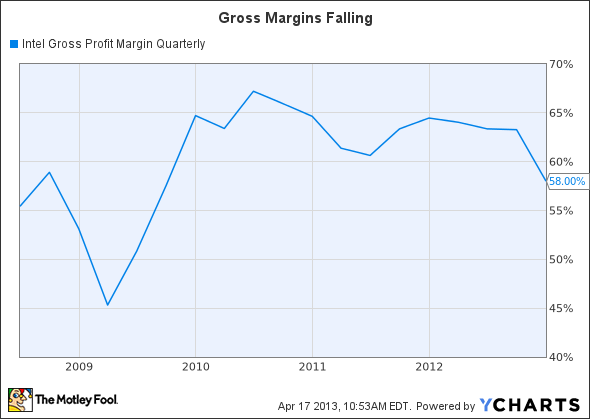

Weakening PC demand has hit its core market and negatively impacted capacity utilization and inventory. Ultimately, gross margins have taken a hit too.

Intel found itself behind the curve in adjusting to the shift towards tablets, ultrabooks, and smartphones.

A slowing consumer

electronics market, plus weaker than expected demand pull from the

release of Windows 8 affected its growth expectations

The end result is falling margins, as inventory gets cleared and

Intel shifts investment to newer technologies and end markets. Indeed,

Intel had to lower revenue forecasts throughout 2012.

It’s easy to make after-the-event criticisms of a management when

these sorts of transitions occur, but it’s also hard not to feel a

certain amount of sympathy. Those that can predict industry trends (let

alone macro) can throw the first stone. Indeed, the market clearly

‘gets’ that Intel has had difficulties because the stock has been marked

down accordingly. The question now is whether its adjustment plans will

work?

Reasons to be cheerful

Before considering the investment case for Intel, it’s worth

reflecting on a couple of issues that will govern the investment

decision. The first is that irrespective of the secular shift to tablets

etc., the semiconductor market is highly cyclical. Indeed, Intel’s

forecast of a better second half is based on an economic improvement.

The second is that in the long-term, there is the threat of ARM Holdings'

core processors winning out over Intel. Intel confirmed that it

wouldn’t take on any competitor-based business within its growing

foundry business. In other words, buying Intel tends to imply a positive

outlook on global growth and confidence in its long-term future against

ARM. Intel’s problem is that ARM-based architecture dominates the

mobile phone market.

Turning back to the secular issues, Intel will launch its Haswell

processors, which will enable it to benefit from growth in tablet,

ultrabooks, and convertibles. This is all part of Intel’s drive to be

more relevant in a declining PC world. There was more good news with the

announcement that it was now making LTE-based phone shipments, while

its tablet and smartphone bases sales are growing well. The problem is

that it has a significant amount of PC-based sales to replace.

In addition, the negative surprise with PC sales has caused overcapacity issues. Gross margins have been falling…

…and they came in at a lower than expected 56% for the current quarter.

So again, it is a question of jam tomorrow with Intel, but at least

it is not lowering revenue forecasts as it did last year. On the

contrary, with the new Haswell processors and data center revenue

(already around 20% of total company sales) growing in double digits,

prospects look better for the second half. I also suspect the Windows 8

disappointment is already fully understood by the market, and Intel

looks better positioned from a product portfolio perspective than it did

last year.

Another area of growth is likely to come from increasing foundry activity. The Altera deal highlights the potential for Intel to generate some value from its older production technology. It

is also good news for Altera, because it secures its chip production

from a world class manufacturer that is looking to generate long-term

relationships with value-based solutions.

However, this developing aspect of Intel’s activities is not good news for Taiwan Semiconductor

The leading semiconductor foundry has seen its gross margin decline

over the last few years, and the last thing it needs is Intel muscling

in on the market. Altera is a long-term client of Taiwan Semiconductor,

and the Intel deal cant have been good news for it. It's margins (at

less than 50%) have never been as high as Intel's.

The bottom line

In conclusion, I think there is a lot to like about Intel. Its valuation is now levels not seen since the recession…

…and a 4%+ dividend yield is a fine income to enjoy while you wait for a turnaround.

Macro matters are always a concern with such a cyclical stock, and

ARM’s strength in mobile does overshadow Intel. But, if you are sanguine

on these issues, then I think Intel has good prospects. It’s a

heavyweight and still packs a punch, and at some point it is going to

remind the market of it.

It’s another huge week for earnings. In this article I've suggested some of

those companies that I find interesting and provide some ideas for further

research. It’s also a good time to try and check the underlying trends in the

economy versus what individual companies are saying about them.

Monday

BE Aerospace and Hexcel are two of the most

interesting stocks in the aerospace sector. The latter is set to benefit from

the increasing use of composites in aircraft, while BE Aerospace is one of the

very few ways to get pure

exposure to commercial aerospace.Incidentally, its French

rival Zodiac Aerospace reports on Wednesday.

However, my highlight of the day has to be Check Point

Software (NASDAQ: CHKP). The Israeli IT

security company disappointed in recent quarters with its negative

products and license sales growth. This is obviously a bit of an issue

because it operates a razor/blade model, even though it has been bundling its

software and hardware together recently. No matter--the fact is that the

company’s product growth is stalling, and I think it needs to do something about

it.

Despite being highly cash generative, tech investors will not reward Check

Point unless it gets back to growth. The good news is that given easier

comparisons coming up and its potential to better market its leading technology,

it may well start to do that in this quarter.

Tuesday

All eyes will be on Apple’s results. However, I am much more

interested in what AT&T says about its spending plans. Tech

is well represented today with Juniper Networks,

Broadcom, Cree, Polycom and

VMware all giving results. I like Idexx Labsas

a company, but must confess that I can’t get anywhere near its evaluation.

Discover Financial is one of the few lenders that has seen its

loan book growing, but is it chasing business or responding to market

demand?Affordable luxury play Coach gives

numbers as well, and it badly needs to demonstrate that it can execute

on its growth plans.

The highlight of the day is actually Yum!

Brands(NYSE: YUM). The company is very

interesting because it is focusing its efforts on growth in China, so what it

says about current consumer trends in that country will be fascinating.

Moreover, it is trying to recover from chicken supply issues in China with

KFC. Don’t be fooled, though--its sales growth was slowing before

the chicken issue. And finally, it is trying to fight for market share within a

difficult market in the US. The stock offers some upside drivers, but it is hard

to predict what it will report. China bulls need to follow it carefully.

Wednesday

A huge day for earnings.Aerospace bellwether Boeing

will give numbers and Procter & Gamble will try

and demonstrate that it is back on track with its growth initiatives.Whirlpool is a genuine play

on housing, and I like its exposure to Brazil as well as its evaluation.

Cigarette company Lorillard is a favorite stock to the bears

who like its defensive characteristics. In similar vein, rail car part

manufacturer Wabtec has long offered one of the few ways to get

exposure to the rail industry.

Data center company Equinix gives results, and while

F5 Networks has already pre-announced

poor numbers, its investors will want to follow the commentary around the

results very closely. The key question is what is happening to its telco

customers? EMC and Coherent also give numbers,

but my highlight is Citrix Systems(NASDAQ: CTXS).

After two tough quarters Citrix got back

on track in the last quarter. Citrix isn’t just about desktop virtualization

anymore--it is a genuine play on the corporate need for mobility and for IT to

be integrated across multi-platform devices. It also has two powerful partners

in Microsoft (virtualization) and Cisco Systems

(application delivery controllers) who are both actively helping it

develop these relative markets.The problems at Fortinet

and F5 Networks were largely a consequence of weakness with telco, but

they reported decent numbers with enterprise customers--a good sign for

Citrix.

Thursday

Tech continues reporting, with Informatica giving results.

Look out for what Ametek says about aerospace, and

3M usually gives good color on the state of the economy. Within

consumer products Colgate-Palmolive needs to keep demonstrating

that it can innovate

and stay ahead of the competition, and, like Mead Johnson,

its growth prospects rely on emerging market growth.

Stanley Black & Decker(NYSE: SWK) is one of the most

interesting housing and construction plays in the market. Not only does it have

upside exposure to a stronger US housing market, but the company is engaging in

a

strategic growth initiative intended to ramp up revenues and take full

advantage of the synergies from the merger. It involves expanding its emerging

market operations and targeting new verticals. The company is highly cash

generative, and the growth programs do not appear to be expensive. If it hits

its targets then I think the stock will head higher because it looks like it has

good value.

Friday

Fridays are usually a bit quieter, but there are some interesting health care

results with Abbvie (the Abbott Labs spinoff) giving numbers.

Weyerhauser will update on end demand from housing.

My highlight is V.F. Corp(NYSE: VFC). There

are a lot of interesting things going on here. The weather got noticeably worse

since the last set of results, and I think this may have caused an increase in

demand for North Face and Timberland products. On the other hand Europe is its

biggest sales center (and Southern Europe its biggest region within that), and

the news hasn’t been great from the continent. Moreover, VF Corp is investing in

China even while its last

results in Asia were a bit disappointing. It is a mixed picture but the

upcoming results might help to set some trends for potential investors to look

into.

Earnings season is in full swing now and Johnson &

Johnson $JNJ was the first of the

major health care and consumer products companies to give results. In summary,

the numbers were pretty good, but the commentary contained some negatives about

the health care industry with regards the medical devices and the volume of

surgical procedures. On the whole, it was a net positive for the company and

despite the great run, I think there is still a bit of upside left in the

stock.

The story

of 2013 is really about integrating the Synthes acquisition with the medical

devices segment, developing sales for some of its new pharmaceuticals, and

getting most of the key brands (affected by production difficulties) back on the

market.

Consumer products making a comeback? (21% of sales)

Within consumer products, management confirmed that 75% of the brands (if not

necessarily the volumes) of those affected should be back on the market by the

end of 2013. Indeed, a build up of these sales is expected throughout 2013.

On the whole, I thought it was one of the most positive earnings reports I’ve

seen in a while for this segment. Okay, overall sales up 3.3% (operationally)

doesn’t sound great, but the underlying trends are positive and investors can

expect better things going forward.

Its two biggest categories are OTC/Nutritionals and Skin Care,

which together make up over 56% of the segment's sales. Sales in both categories

have been weak in recent quarters, but the former is benefiting from having

products back on the market (analgesics were particularly strong) while the

latter appears to be stabilizing in the face of strong competition. The good

news didn’t stop there as baby care sales grew 7% operationally, with oral care

also doing well with a 5.1% increase.

Colgate-Palmolive $CL shareholders should

note that Listerine mouthwash was cited as a notable positive in these results.

Frankly, I think that Colgate has had it a bit easy in the past, with being able

to aggressively launch new mouthwash products in the U.S.

It is obviously not a core activity for Johnson & Johnson (indeed it has

divested some toothbrush products), but it has learnt from Colgate’s execution

and the new Listerine products appear to be working well. I see no reason why

this can’t continue, so investors need to think about the assumptions they are

making over Colgate’s valuation and earnings.Moreover, Colgate already has a

strong position within emerging markets and it will have to defend it against

competitors.

Pharmaceuticals still going strong (39% of sales)

This segment has seen the most impressive improvement in performance over the

last year and it looks set to continue this year. Overall, sales grew 11.4%

operationally and many of the drugs that contributed to this growth are still in

the early innings of their sales progression.Meanwhile, its

biggest treatment is still Remicade (rheumatoid arthritis), which represents

nearly 24% of total pharma sales and it is still growing nicely with 5.5%

operational growth in the quarter.

Other highlights from the segment included

Immunology (including Remicade) grew

16.7% operationally, with Stelara (psoriasis) and Simponi growing sales by 72%

on a combined basis. As they are both relatively new drugs, it is reasonable to

expect strong growth to continue within this category

Neuroscience revenue grew 7.7%

operationally, with Invega and Invega Sustenna sales now totaling $416 million

and managing to replace declining sales of its older schizophrenia drug

Risperdal Consta, which contributed $335 million, albeit after a 6%

decline.

Oncology represents less than 12% of

pharma sales, but it contributed over 31% of the growth in the quarter. Zytiga

(castration resistant prostate cancer) sales grew over 72% and the intent is to

try and get its usage extended for other indications.

Xarelto (anticoagulant)

and Incivo (hepatitis C) contributed $158 million and $162 million in the

quarter, and both are likely to grow strongly in the future.

In summary, new drug sales are expanding rapidly and it’s hard not to see

continued strength here.

Medical devices and diagnostics (40% of sales)

This proved to be the most interesting segment as the company outlined how

within the U.S., hospitals had been commenting that procedures were running at

levels below what they had previously predicted for 2013. Moreover, within

general surgery and orthopedics, it declared that the acceleration that it had

seen in Q4 did not carry on into Q1, and suggested that this was a sign of

seasonality creeping into these elements' performance.

All of this would appear to be disappointing news for a company

like Covidien $COV. Covidien’s surgical

activities rely on growing procedures, but elsewhere, I thought there were some

good takeaways for Covidien.

For example Johnson & Johnson’s cardiovascular results were good, with

endovascular cited as generating double-digit growth. Meanwhile, its

international energy results were strong outside the U.S. This bodes well for

Covidien, because expanding in energy and vascular within emerging markets is

one of its key

growth drivers for the next few years.

So, it appears that Covidien will report good results from its existing

growth businesses, but there could be some pressure elsewhere. We shall see soon

enough when it reports on April 26.

There was no new news on the future of the diagnostics unit after it had been

put under review at the time of the last set of results.

The bottom line

This was probably a better set of results for the company than it was for the

health care market on the whole. The more negative outlook with regards surgical

procedures is likely to cause some concerns among the higher rated companies

within this sector of health care.

However, for Johnson & Johnson, its pharma sales are expanding well and

look set to continue. There is still upside from a return of the affected brands

within consumer products and its plans remain on track.

The stock remains the sort of high cash generating, decent yielding defensive

type that the market is in love with at the moment, and I wouldn’t be surprised

to see the stock appreciate in the future.

Investing in stocks is a bit like a visit to an auction. Some people

enjoy paying a premium for what is in fashion so they can sell it on to

someone more excitable than themselves, others enjoy buying a quality

item at a reasonable price, and there are those that enjoy buying

anything because it’s cheap.

And then there are those who kind of think something is fashionable,

the item is cheap, and they can overlook some flaws in the product while

hoping that others will do too. This article is about the last group

and why they might love a stock like Bed Bath & Beyond $BBY.

Bed Bath & Beyond ticks some boxes

Yes, it is a housing-related play and yes, on a forward PE of 12, the

stock is cheap. On the other hand, this company has exhibited rather

less than stellar performance over the last year, as margins have fallen while comparable same-store growth is in low single digits at best.

Only last quarter, the company was forecasting same-store sales

growth to be in the 2%-4% range, but they came in at 2.5% for Q4.

Moreover, it is relying on growth from a couple of acquisitions which

have actually reduced margins. My sense is that there are better stocks

in the ‘housing franchise’, but as one of those people above who only

want to buy quality, this isn’t the sort of stock I can fall in love

with anyway.

Whether you buy value or growth, I think it’s fair to say that the

prospects of this company depend more over its execution than a

continuation of its immediate past. The company has been subject to

increasing competition in the sector, and is seen as the primary loser

due to Amazon.com's $AMZN move into the home goods space.

Not only does Amazon retail home goods through its core sites, but it

also owns the parent company of casa.com, and the latter appears to be

taking direct aim at Bed Bath & Beyond’s market. Amazon has the

scale to be able to hurt its rivals.

Here is a look at Bed Bath & Beyond’s margins and possibly at how Amazon has effected it.

I’ve included a bar chart of the year on year movement in operating

margins in order to better illustrate the situation. It doesn’t make

pretty reading, and there is a sense that the company needed to make the

World Market and Linen Holdings acquisitions in order to deal with

encroaching competition.

The industry fights back

The threat from Amazon has certainly spurred the incumbent players to

respond. And frankly, not an earnings report goes by without one of

them announcing a step up in capital expenditures in order to expand

e-commerce offerings.

For example, Pier 1 Imports $PIR

recently announced that it would be rolling out a point of sales (POS)

system and fully integrate it with its e-commerce facility.Pier

1’s plan is to continue to offer in-store pick up for its online

customers, while trying to differentiate its offering from the

competition.Will it continue to do this successfully in the future

and/or does it run the risk of cannibalizing its retail sales? That

remains to be seen.

Similarly Williams-Sonoma $WSM has a three pronged strategy

of expanding its e-commerce facility, international expansion, and

rolling out new stores in its growth brands. Again, it is trying to

achieve a certain amount of differentiation with its offerings and

experimenting with its new stores.

I think that it will do well with its teens and baby furnishings

because this is more of a ‘conceptual sell’. In other words, shoppers

will appreciate going to the store in order to feel the impact of its

furnishings. Furthermore, its range is somewhat more high-end than Bed

Bath & Beyond, and relatively less susceptible to Amazon’s

onslaught.

Where next for Bed Bath & Beyond?

In common with the industry, it is moving to a multi-channel offering

and is launching some new websites this year, while aiming to generate

margins in order to try and turn around performance. Thus far, the

acquisitions have eaten into margins (at a time when some of existing

stores were reporting poor performance), and the plan to improve

prospects will see a ramp up in capital expenditures to $350 million

next year from $315 million this year.

Much of the capex is dedicated to store refurbishments

and integrating the World Market and Linen Holdings acquisitions. In

addition, the shift to lower margin products in the sales mix as well as

increases in coupon redemptions will continue to pressure margins going

forward. It's tough out there.

Putting all these things together means that an investment in the

company depends upon a certain level of confidence in its plans to turn

things around in 2013. Its not the kind of situation I enjoy investing

in, so I will take a pass. It’s also not the sort of company you buy as a

pure play on housing, but you might if you are hunting for a bargain

than could suit your purpose. You just have to expect that it will come (as do all value plays) with some faults.

Pier 1 Imports (NYSE: PIR)delivered

yet another strong quarter of results that highlighted its status as

one of the ‘go to’ plays for a housing recovery in the States. It is not

that the US mass consumer is in particularly good shape right now, but

there are a few sweet spots (housing and autos) seeing relative

strength. In addition they tend to be coming off a low base so the

opportunity for upside leverage is considerable. Where next for the

sector?

Housing Thesis Still Intact?

It’s been an interesting few days for the housing market thesis. I’ll return to Pier 1 in a moment but first a few words on Wells Fargo’s (NYSE: WFC)

latest results. The bank’s importance to the US mortgage market is

significant, and there wasn’t a lot of great news on that front in the

latest report. Within its consumer lending group, originations,

applications and the application pipeline for home loans all declined

sequentially by $16 billion, $12 billion and $7 billion respectively.

However there was better news for auto originations, which rose 10% year

on year.

This is hardly great news for the current housing market and suggests

that it will take a while yet for the recovery to fully kick in. I

suspect we are seeing a sustainable recovery, but it is gathering

traction at the higher end first. Ultimately, these things feed down

into the wider market, and as long as employment gains continue to grow

apace I suspect this will happen. There is no doubt that it is taking

longer to happen than normal at this stage of a recovery, but that is

the way it is and investors need to factor this in.

For Wells Fargo investors this means patience will be required, and

they will need to take a sanguine view over yield compression. This

graph demonstrates the essence of the challenge facing the bank in 2013:

Net interest income and margins are getting weaker because the bank

has seen large rises in deposits while the bank deals with the maturing

of previous loans at favorable rates.

With that said, the net interest income after provision for credit

losses actually rose 4.3% thanks to a lowering of provisions. The bulls'

hope is that a point of inflection will come whereby increasing credit

quality and an improving economy will graduate into a better lending

environment. I happen to think this will happen, but Wells Fargo could

clearly do with diversifying its revenue generation while waiting.

Pier 1’s Plans

Of course this is music to the ears of Pier 1 investors, because the

company has thus far benefited from the nascent housing recovery and

there should be upside to come if it continues.I had previously thought that its same store sales guidance for 2012 was conservative, and indeed the Q4 numbers came in at a healthy 7.5%.

On the basis of any metric the company is seeing strong performance,

and its plans for 2013 and beyond are being made within a decent end

market backdrop. I think there is a good chance that Pier 1’s plans to

aggressively increase its e-commerce activities and its point of sales

(POS) in-store systems (the two will be fully integrated in the future)

will work to expand revenue generation in the near to mid-term.

The idea of a multi-channel retail experience is also in fashion at Nordstrom(NYSE: JWN).

The latter is trying to differentiate its offerings but offering more

of its lower price point stores (Rack) while increasing its e-commerce

activities (organically and via acquisitions) offering--you guessed

it--point of sales systems in its stores that are intended to integrate

with the e-commerce offering. My concern with Nordstrom relates to the

sheer expense and sophistication of its program.

Some Concerns

So Pier 1 is not alone here, and there is evidence that its

e-commerce sales tend to attract sales of higher ticket price items. All

of which sounds great, but I confess I have my longer term concerns.

If e-commerce is the future then investors have to recognize that the likes of Amazon(NASDAQ: AMZN)

are also stepping up their own home goods offerings. Not only does

Amazon have its own operations, but it also owns the parent company that

runs casa.com. Moreover, Amazon’s strength is in its scale offering of

commodity type products. Consumers are happy to buy such items online

because they do not have to make the kind of decisions that they do with

a more individual product. Ultimately an expansion in overall

e-commerce home goods sales could cause a situation where copycat

offerings are commonplace, and Pier 1 could lose its distinctive

identity or ability to generate sales via the in-store retail

experience. The result is an ongoing race to the lowest price. Not good

for margins.

The Bottom Line

In conclusion I think the housing market recovery will eventually

broaden, and Pier 1 is a legitimate way for investors to play this

theme. Its initiatives make sense, and the stock does not look

expensively priced at the moment. Longer term, there are concerns, and

the fears I’ve discussed above need to be monitored closely. It’s not a

stock I’d want to hold for the next five years but for now things look

okay.

I'm a bit bemused by the events at Ixia $XXIA.

Recently, the stock took a massive battering after announcing

accounting errors that reduced 2012 income, and will hit revenue

in Q1 2013. It sounds grim enough, but in reality, no contracts have

been lost, cash flows haven't disappeared, and -- at least for now --

the only major impact appears to be over the timing of how it reports

revenue. Let's find out what is going on.

Ixia reports accounting errors

On March 19, Ixia filed a notification to the SEC that

it would be late in filing its 10-K as a consequence of having

identified an accounting practice error related to how it recognizes

revenue from its warranty and software maintenance contracts.

This was followed by an 8-K filing on April 3, which

identified a separate implied arrangement error related to how it dealt

with revenue recognition after extended warranty and software

maintenance contracts have been signed. Ixia finally filed its form 10-K

on the April 4.

Now I know what you are thinking and you would be right. This does

sound like tortuous accounting and legal jargon, and I'm not impressed

by the accounting errors either. I wasn’t expecting this when I bought the stock, but are these errors really a big deal?

Accounting practice error

I’ll start with the accounting practice error and quote directly from the 8-K formregarding its historical practice which…

“was to begin recognizing revenues relating to the Company's

warranty and software maintenance contracts commencing on the first day

of the calendar month following the effective date of the contract, as

though the warranty period commenced on the first day of such month and

extended for its full duration thereafter”

In plain English, this means that if a contract was effective

on April 15, then the company previously recognized revenue on May 1,

rather than on the effective date. It will now have to report them from

the effective date instead. Frankly, I don’t think there is anything

dubious or sinister going on here. It was probably easier for the

accounts people to aggregate revenue in this way, and the practice had

the effect of reducing near-term revenue and income. Not something you would do to massage numbers.

Implied arrangement error

The second error was defined thus

“The Company has determined that it was required to cease to

defer revenues related to the implied warranty and software maintenance

arrangement upon the receipt from the customer of the first substantive

contract for extended warranty and software maintenance services, and

will recognize the applicable previously deferred revenues balance

related to the implied arrangement, provided all other revenue

recognition criteria have been met.”

This is more a serious issue as Ixia was deferring revenue

recognition while it waited to establish that it could enforce its

warranty and software maintenance contracts. The good news is that it

only relates to one contract. In any case, here are the material effects

expected for 2013 for both errors.

Ixia doesn’t believe the accounting practice error will have a material effect on Q1 2013 or the full year

The implied arrangement error

will move $4.15 million of the previously expected $4.9 million in

revenue from Q1 to previous years' results. No impact is predicted for

the rest of 2013.

So it looks like just an issue over revenue recognition timing.

Previous years?

I think the market has been fretting over the loss of revenue and

income for this year, rather than looking at the implied increase in

revenue and income for previous years. Indeed, the 10-K outlined that

net income would be going up around $360,000, $3 million, $1.6 million,

and $2.9 million in the years from 2008 to 2011, respectively.

Meanwhile, 2012’s net income was reduced by nearly $1.8 million and

the ‘loss’ of $4.15 million from Q1 will likely reduce net income

accordingly. It’s not good, but is that the only way to judge a company?

And this leads us to the crucial point. This is an issue of the timing

of recognizing revenue, and whether it is recognized as revenue or

deferred revenue at any particular time. From a free cash flow (FCF)

perspective, there isn’t much difference. For example, in the years

outlined above (where Ixia is now recognizing more revenue and income)

there isn’t a change to its FCF generation.

A company is best judged on its cash flow generating abilities, and I

think it’s being treated a bit harshly here. In fact, it generated

$62.4 million in FCF last year and that’s not a bad evaluation for a

company with a $1.34 billion market cap and high growth prospects.

Where next for Ixia?

Of course, none of this includes any analysis of what to expect in

the upcoming results. For that, you will have to look at its major

customers like Cisco $CSCO (13.5% of revenue in 2012), Alcatel-Lucent, Juniper Networks $JNPR, and the major telco carriers. Its competitors include companies like Spirent, JDS Uniphase, Gigamon, and Danaher.

Cisco is obviously the first port of call, and its wireless solution revenue has been growing at 20%-30% for the last four quarters. Indeed, Ixia confirmed that revenue from Cisco grew 30% last year. With AT&T and Verizon both stressing that wireless is an investment priority in 2013, Cisco should report good numbers in this segment.

Moreover, Juniper has been reporting better results of late as it

continues to beat estimates. Although wireless isn't a core part of its

revenue, it is one of its fastest growing segments. Analysts have been

gently raising forecasts over the last few months, but the key news is

that Juniper is seeing strength (in a weak environment) in areas like

mobility, high performance networking, wireless, and the cloud.

These are all good drivers for Ixia’s testing equipment.

As for JDS Uniphase, it reported CommTest revenue at the high end of

the guidance, and spoke of a return to spending by Tier 1 carriers in

2013, although its customers are expected to start releasing their

budgets in March.

In conclusion, accounting errors are never a good thing, but I don’t

see the reason for the stock to get beaten up so badly. In addition, the

company recently announced

that it expected revenue to come in line (excluding the $4.15 million

reduction discussed above), so the underlying trends seem okay. The

accounting errors aren't expected to affect future quarters and this

looks like a timing issue to me. It also looks like a buying

opportunity, so I topped up.

We are very early into earnings season but already two leading

tech companies have reported weaker earnings thanks to a reluctance

among telco service providers to close deals. F5 Networks $FFIV previously disappointed and now it’s the turn of Fortinet $FTNT to warn over missing estimates.

Fortinet Warns in Q1

The preliminary announcement of results brought with it some disappointing expectations.

Total billings expected to be $147-149 million vs. internal guidance of $158-162 million

Total revenue expected to be $134-136 million vs. internal guidance of $138-141 million

The billings miss of $12 million (at the mid-points) was blamed

on three factors. In the commentary around the results the managements

claimed that $6-9 million was due to the service provider segement,

Latin America missed by $4-6 million, and there was an inventory

shortage due to a product transition, which caused a $2-4 million miss.

The Good News First

Firstly, the inventory shortage issue was forecast to be

rectified within a quarter so we can expect some of those billings to

come back. Secondly, the geographic performance was mixed. Latin

American weakness was put down to some local macroeconomic issues,

although there is a new sales management in place there expected to

improve performance going forward. Europe was cited as being weaker, but

not by much, and a large deal is expected to close soon. Fortinet had

has some issues with China previously, but that region was declared

‘back on track,’ and Asia was strong in general with Japan surprisingly

good.

Thirdly, the really good bit of news was that US enterprise

based spending did well in the quarter. This nicely mirrors what F5

Networks said over this segment of its sales too.

This is heartening because it implies that this is not really a US

macro issue. I’m glad that Fortinet confirmed this, because the view

from F5 is somewhat obscured by the fact that it is undergoing a product

refresh right now.

And Now the Bad News

The bad news is that, just as F5 Networks did, Fortinet argued

that the telco service providers were determined to prove themselves

villains in the quarter. Almost word for word, Fortinet repeated the

mantra that F5 had earlier argued. My interpretation of the commentary

runs a bit like this: yes there are large deals out there, no they

weren’t closed with others due to competition, yes we think we can close

them in the future, but no we can’t be sure when the telcos will do

this… and I doubt they are both lying!

In the case of F5 it is a bit more obscure because of the

product refresh and its dominant market position (50-60%) in its core

application delivery controller (ADC) market. Moreover, Cisco Systems $CSCO

has pulled out of investing in its ADC, so it is reasonable to expect

F5 to be winning some new business there. Similarly, with Fortinet there

is the fear that its weakness is being caused by Cisco bundling

security solutions with its core networking equipment to the telcos and

undercutting other players. However, there was no indication of this

from F5 or from Fortinet.

Instead, there appears to be a shift in service provider

spending towards more cautious piecemeal spending. Indeed, Fortinet

spoke of one large customer that changed from a ‘capex to an opex’ based

approach and decided to shift the purchasing over multiple quarters

rather than buy with one large deal.

All of this resulted in a nasty sequential drop in Fortinet’s revenues:

And there can be few guarantees that this will recover in time.

Where Next for Fortinet?

It’s a nasty miss, but I think there is some cause for optimism here. Firstly, if we go back to what Fortinet reported last time we can see that it was a strong quarter that involved a significant amount of larger deals being won.

And since the telco deals that missed in Q1 tended to be larger

deals, perhaps the Q4 performance is a sign that there was a budget

flush in that quarter? Similarly, I note F5 reported a strong quarter from telco in its Q1 only to disappoint in Q2. A royal budget flush? I’m wondering out loud what this might mean for Cisco’s forthcoming results.

If this turns out to be the case then the weakness within the

service provider segment may be incrementally graduated into forecasts

over the full year as both companies get over the effects of the change

in purchasing patterns by the telcos. Furthermore, if US enterprises are

still spending then the economy can’t be in that bad shape.

As I write, Fortinet is trading on a current FCF/EV yield of

just over 5% and is on track (in a bad quarter) to generate 8% year on

year billings growth with revenue up 15% for Q1. That is not bad at all,

although cautious investors (like me) will want to listen to what the

Tier 1 service providers say about their spending plans in the

forthcoming results. Provided their outlooks are okay, I think Fortinet

is worth a close look down here.

It’s been an unusual year for the dollar stores. For much of the

first half of 2012 they looked overvalued, even as they continued to

generate impressive earnings growth. They were seen as the great trading

down play, and for good reason. The problem is that when everyone sees

it that way, it becomes hard to get a decent entry point. Roll on the

second half of 2012 and things became a bit more uncertain as its end

markets got tougher. Again the stocks looked attractive, but there was

no obvious entry point. Roll on 2013 and their outlooks definitively

worsened--and so did their stock prices, but are they good value now?

The Outlook For the Dollar Stores

The underlying story within the narrative above is that there has been a gradual shift in the sales mix for the dollar stores. In

the initial post recession years it became clear that the mass consumer

was trading down to the dollar stores and creating new demand. Now that

that easy pickings from that big move are over the challenge is to keep

generating growth while the established grocers like Kroger $KR take action to gain back market share.

In particular, Kroger has been gaining share in the value segment by offering its own corporate brands. It is doing very well with them and Kroger has the footfall to be able to recapture some sales lost to consumers trading down at the dollar stores.

As for the dollar stores, there are three things that I think they can and have been doing:

Expand category sales and try to move into higher margin areas

Expand stores and capture new geographies

Drive footfallvia tactical expansion into categories like consumables

I’ll come back to these points and give my assessment, but first a few words on their end market prospects.

The Dollar Store Marketplace

It is very easy to fall into the trap of analyzing the retail market

in terms of an amorphous mass that moves in the direction of the

economy. But a retailer like Family Dollar$FDO

shouldn’t be looked at in that way because it tends to sell to lower

income customers. To give some perspective, here is a breakdown of the

share of net worth in the US sourced from the Bureau of the Census. It

is sorted by income holders.

I think it’s fair to say that the dollar stores’ customers will

largely come from the bottom 60-80% of the populace. As you can see they

don’t have that much purchasing power! In addition, their prospects are

more affected by unemployment and job insecurity. So even as the

economy recovers moderately, conditions will still be tough for its

customers.

Family Dollar Analysis

I'm going to run through the three objectives discussed above in focusing on Family Dollar.

Firstly, it tried to increase higher margin home and apparel based

sales but ran into merchandising difficulties. I suspect that this is

partly a consequence of not having particular experience in apparel and

also due to the fact that its customers shop on necessity and want

consumables. Family Dollar may well have seen TJX Companies $TJX and Ross Stores $ROST doing very well in apparel and home goods, but it is another thing to be able to match them.

TJX’s management has vast experience in clothing, and its business

model is predicated on ‘off-price’ retailing rather than the kind of

discount clothing that the dollar stores may offer. Moreover, TJX’s

customer base is largely discretionary, its footfall is generated by

people coming to buy clothing and home goods. Whereas Family Dollar

shoppers are trying to buy a cheap bottle of ketchup, will they stop and

buy the apparel that has been placed at the front of the store?

Second, Dollar Tree $DLTR and Dollar General $DG

have also been rapidly expanding stores even while same store sales

growth is slowing. Indeed, Dollar General has spoke of aggressive price

competition and is (like Family Dollar) taking a more cautious approach

to its guidance. Its response to competition is to reduce pricing in

certain categories, but this comes at the cost of margins. Similarly,

Dollar Tree has seen same store sales slow to low single digits. Falling

margins, slowing sales growth and tough competition.Is this the time to be expanding stores?

The third point is that as Family Dollar generates footfall by

selling more essential consumables (which now make up nearly 70%) it is

likely to suffer gross margin pressure. We can see that in the following

chart:

Note how gross margins are falling.

Is Family Dollar a Buy?

In conclusion, there are challenges facing Family Dollar and as

attractive as they undoubtedly are I don’t think it’s time to buy in.

Family Dollar is increasing capital expenditures and its inventory

levels have been rising more than sales as it sells more consumables.

Analysts have it on a forward PE ratio of around 15, and

I don’t think this is adequate recompense for the risk in its expansion

program. I would like to see the dollar stores scale back these plans

and concentrate on their core competency.

Just when you thought it was safe to go back into industrial stocks, Fastenal $FAST and MSC Industrial Direct $MSM

delivered results that raised more questions than answers. Both

companies were downbeat and went to lengths to describe how their

businesses weren’t performing in line with the headline manufacturing

ISM numbers. So what is going on, and what is the read across from these

earnings?

ISM Not Relevant Anymore to Fastenal?

Traditionally the manufacturing ISM numbers have guided the

industry’s performance, and even more so when it comes to the industrial

suppliers. Indeed, the theory (at least mine) was that the stronger

numbers in the first quarter would lead to a resumption of growth in the

industry. Well, according to Fastenal and MSC, that was not the case!

Here are the headline PMI and New Orders numbers from the ISM.

Starting with Fastenal, it declared that its sales growth was a

‘struggle’ in the quarter and conditions continued to slow down. This

sort of commentary is not congruent with the ISM numbers, and its

management even suggested that its performance wasn’t as correlated with

the index as previously thought.

The bad news didn’t stop there, as its vending machine signings were

lower than expected. In addition it had planned for 65-80 new stores for

2013 but announced that it expected to be at the lower end of the range

in 2013. Although the company declared that it would still invest, even

in a slowdown, it wouldn’t surprise me if it reined in some expansion

plans if slow growth continues.

To put Fastenal’s report in the context of its longer term plans I would recommend going over this article.

In terms of its long term 'pathway to profit,' it is obvious that all

the objectives are somewhat reliant on sales growth. Unfortunately this

is something that has been slowing for Fastenal in recent quarters.

The problem appears to be in its fastener sales, and this is usually

an indication of broad based weakness.The one bright spot was its

metalwork products, which grew at above the company rate. I’ll come back

to this point later.

MSC Weak Too

It was a difficult quarter for MSC too. Having previously announced that its end markets were in a holding pattern, which had descended into ‘paralysis’

in December, it was reasonable to expect better things this quarter.

However, the company declared that the latest weak ISM number for March

were more in line with what it was seeing in its current trading

conditions. Indeed, it reiterated what Fastenal said about sequential

weakness in the quarter with January being relatively strong leading

into a weaker February and March.

Interestingly it highlighted the metalworking sector as a particular

area of weakness. This is contrary to what Fastenal said, but my guess

is that the latter has more exposure to aerospace and aviation. If we

look at Alcoa’s $AA

recent results there was ongoing strength predicted for the aerospace

industry, while the US automotive sector is forecast to grow at 0-4%

this year. However, Alcoa did not raise its forecast for its US

commercial building & construction despite more optimistic

indications from new house builds and the Architectural Billings Index.

Jam tomorrow?

What Is Going On?

It is hardly a clear picture, but what we do know is that the areas

of relative strength in the economy are in things like autos, housing

and aerospace. This is probably a function of how weak the first two

industries have been in recent years.In other words,

comparisons are easier in these industries. Furthermore they are due to

grow thanks to net household formulation and the age of the US care

fleet. Aerospace’s strength is due to its global exposure and the

recovery in profitability of the airlines.

Allegheny Technologies $ATI is the sort of stock that will give good color on these themes. It

recently outlined strong numbers from aerospace builds but weaker demand

from the nuclear industry. In addition oil & gas demand was

forecast to be lower thanks to inventory management actions by its

customers. The story from Allegheny is one of a mixed industrial outlook

and it mirrors what Alcoa said recently.

Where Next?

Fastenal and MSC are companies with limited visibility

so things can turn around pretty quickly for them. Furthermore, my hunch

is that there is a willingness among industrial customers to hold off

purchases whenever they see political uncertainty. Obviously long cycle

industries like aerospace can’t really adjust demand levels in the short

term. In other words, conditions can improve, and I suspect they will.

However my issue with buying either stock is thatthey

are not cheap enough. Falling sales growth is never a good sign, and

when I buy stocks like this I would expect to buy them with some excess

negativity priced in. As I write, they trade on 34x and 19x current

earnings respectively. I think that’s too much to pay for a cyclically

aligned sector with little visibility and falling sales growth.

After a quiet opening week to earnings season, this week brings a

torrent of earnings reports from Dow components and industry

bellwethers.

Monday

Monday starts with Citigroup reporting, and it’s going to kick off a big week for financials.

Tuesday

The banking theme continues on Tuesday with Comerica and Goldman Sachs reporting numbers. We also have three bellwethers reporting.

In healthcare, Johnson & Johnson (NYSE: JNJ)

will update investors on how its revival in pharmaceuticals is going.

Within pharma, I would look for ongoing strength with Remicade

(rheumatoid arthritis) and growing Stelara (psoriasis) sales. However,

the real question will be over its consumer products division.

A brief look at the previous results

reveals that it is still under performing, and it needs to get the

brands affected by quality problems back into production. Similarly,

OTC/Nutritionals and skin care have been weak in recent quarters. The

third major division is medical devices & diagnostics. The company

is ‘evaluating options’ with its diagnostics operations, and continues

to integrate Synthes in to its orthopedics offerings. In summary, the

focus in these results should be on execution with its consumer

products.

The key things to look out for in Intel’s (NASDAQ: INTC) results will be its gross margin outlook and inventory situation. Historically, the stock has tended to trade in the direction of its gross margins,

and the declines last year have mirrored poor stock performance. While

these issues will govern the short to mid-term performance, investors

should also focus on the development of its longer-term plans to invest

in solutions for ultrabooks and tablets. Intel is somewhat late to the

party with some of these things, but it has the scale and financial

firepower to get back on track.

The Coca-Cola Company is the third major bellwether to give results today. In addition, industrial play W.W. Grainger will give more color on current conditions.

Wednesday

This day will see numbers coming out from Abbott Labs, American Express, Bank of America,Core Labs, Crown Holdings, Sandisk, and Textron. Alcoa

recently talked of better conditions for business jet orders, so it

will be interesting to hear what Textron has to say because it too gave a good forecast late last year.

I’m also looking out for Dover’s results. It has had some difficulty with its sound solutions division, and it will be interesting to hear what it says about is smartphone-based sales because Nokia is a major customer.

In rather obscure fashion, I am going to focus on Quest Diagnostics(NYSE: DGX). This is not the sexiest stock nor is it in the most fashionable industry, but, I think there is an interesting value case here. It generates a lot of cash and is a dominant player within an industry in need of consolidation.

Moreover there are a number of management initiatives in place in order to try get to the kind of growth rates that its rival Lab Corp

(which reports on Friday) has been able to achieve. It’s a boring

stock, but it's cheap and if a turnaround can be achieved, it will

surely appreciate.

Thursday

There are some interesting health care plays reporting today with results from Baxter, Cepheid, and Intuitive Surgical. Banking is represented by Morgan Stanley.Industrial giant Danaher reports, as does Tier 1 telco carrier Verizon. PepsiCo is a company with a strategy that lacks coherence

in my humble opinion. It is also a decent yielding stock in a hot

category right now. The market has been very keen to bid up food stocks

lately.

There are also some interesting housing and construction plays reporting. I’m not convinced by Restoration Hardware’s valuation justifies the uncertainty over its growth strategy. As for PPG and Sherwin-Williams, the former has significant exposure to China and the latter is attractive thanks to its U.S. housing exposure, but the stock is hardly cheap.

Google(NASDAQ: GOOG), IBM (NYSE: IBM), and Microsoft also give numbers. As ever, the market will focus on the relationship between cost per click and paid clicks growth at Google.

Google doesn’t give guidance, so its results always cause a lot of

volatility and this time won’t be any different. I think Google is

managing the transition to tablet and mobile internet usage very well,

and investors often underestimate its international growth prospects.

There is no reason why it can’t reach the kind of metrics generated in the U.S. with its international operations.Moreover,

we are in the early infancy of the big data revolution and its search

facility is something actively used by people. Long-term growth is

inevitable.

IBM’s chief rival Oracle gave disappointing results recently,

so there are some concerns over what IBM will report. Oracle insisted

that this was more of a sales execution issue rather than macro

weakness. In addition, I think Oracle is going through some product

transition issues as well, as it's relatively underexposed to

cloud-based offerings.

IBM investors should expect good System Z hardware sales, and I

suspect we are about to find out whether it is taking share from Tibco Software in middleware and analytics after that company reported a horrible set of results recently.

Friday

The big news on Friday will come from General Electric. Its last results were strong and contained some upside surprise from health care in emerging markets, plus some impressive order growth overall. Baker Hughes, Honeywell, and Rockwell Collins also have activities that cross over with parts of GE.

Last but not least, Kimberly Clark and McDonald’s will update us on the mass consumer market.