This blog is devoted to helping investors make informed decisions. It will be regularly updated and provide opinions on earnings results. It is not intended to give investment advice and should not be taken as such. Consult your investment advisor.

The retail sector usually makes sense,or at least we can delude

ourselves that we can make sense of it all. There are obvious

macroeconomic trends filtering through into the results of the companies

in the sector. From the dollar stores to the high end, through the

specialty stores and the online based companies, there are discernible

patterns we can use to gauge future performance. And then there is Costco Wholesale (NASDAQ: COST).

Costco executes

I last looked at Costco in an article linked here and highlighted how well the company was doing but also inquired as to where the value was in the stock price. The

answer to my question was that it lies within its ongoing execution and

ability to service its customers with the goods they want. As

investors, we are more interested in its stock price potential rather

than its company performance per se, but in this case I think the

stock’s evaluation of 24x trailing earnings is at a level where the two

things are correlated.

This chart helps to outline how well the company has been doing over the last year:

Clearly gross margins have been expanding over the last five quarters

(note that the yearly comparisons are starting to get tougher too)

while comparable sales growth remains good too. Overall revenue growth

remains in the high single digits, and the company’s expansion program

(particularly internationally) remains on track. Indeed, Costco expects

to finish the year with 28 new openings as opposed to 16 last year. Of

the nine more expected for 2013, three are planned for the U.S. and the

other six are international.

What is Costco doing right?

And, more pertinently, can it continue to do these things right? I

have a five main points to discuss from its recent Q3 results.

Firstly, Costco’s traffic remains strong and it reported year to date

frequency up 4-5%. Costco cited the draw of its gas sales (30% of

people buying gas go on to shop at Costco), fresh food (which has seen

increased demand as the slow economy has reduced the demand for eating

out), and the ‘wow’ factor of many of its items.

Second, I think the psychological effect of inducing people to shop

at Costco after they have paid a membership fee is a sound one based on

many of the principles inherent in work on behavioral studies. I think a

membership fee is looked at as a sunk cost, but since people will ‘pay’

more to avoid a ‘loss’ they will shop at Costco in order to do this. Of

course if that cost increases (and Costco has hiked membership fees in

recent years) than the feeling of 'loss' will increase and customers may

be induced to shop more at Costco.

Third, membership fee increases have not encouraged churn. In fact

business renewal rates started and finished the quarter at an impressive

93.9%. New membership signups increased 19% with particular strength in

Asia. Membership fee income increased 12% to $531 million.

Fourth, Costco continues to generate growth where others can’t. In

particular I was struck by the strength within hard lines where it

recorded strong growth in lawn and garden and consumer electronics.

And lastly, Costco continues to reduce its stock keeping units (SKUs) in order to optimize inventory turns and profitability.

Costco is, of course, not alone in many of these activities but it

compares very well across the sector because it does all of them well.

For example Lowe’s Companies(NYSE: LOW)

has an ongoing plan to reset its product lineups in order to reduce

SKUs and ‘normalize inventory.’ While this may appear routine stuff,

Costco has been doing it well for years while Lowe’s has had to adjust

because it wasn’t doing it well. With that said, Lowe’s actually has some upside potential from successful execution of this plan.

Moreover, Lowe’s (and Home Depot for that matter)

both reported that outdoor and garden items were a bit soft in the last

quarter thanks to the late spring. In comparison Costco cited these

categories as being strong.

Whither Wal-Mart?

Costco isn’t alone in its membership fee model as BJ Wholesale and Wal-Mart’s(NYSE: WMT)

Sam’s Club also take membership. Wal-Mart is following Costco by

increasing its membership fee but its execution is nowhere near Costco.

For example its comparable sales growth (ex fuel) was only up .2% in the

last quarter with traffic up 1.3% compared to Costco’s 4.5%. In

addition its ticket value was down 1.1% while Costco’s was flat.

So while the economic environment is difficult and Wal-Mart on the

whole has been a bit disappointing (a net sales increase of only 1.8% in

the last quarter), Costco has outperformed, particularly against Sam’s

Club.

The bottom line

In conclusion, while something like Wal-Mart is largely a play on the

economic environment, Costco has demonstrated that its superior

performance can justify an evaluation premium over Wal-Mart. The problem

is that it will be pressured to continue this execution in order to be

rewarded by the market. Any slip-up and/or step-up in competition from Target or Wal-Mart and its current PE of 24x will start to get hard to justify.

When looking at a stock it is always tempting to take an initial peek at its share price graph to make a quick and easy assessment. In the case of Pall Corp(NYSE: PLL) and its impressive looking chart, it would be easy to conclude that things are going great, but the reality is that it has been a challenging environment for the industrial sector.

In summary, there are some changes afoot, and investors would be best advised to be selective with investments within the sector.

Structural changes

I have two main observations here.

The first is that it has been a mediocre Q1 reporting season for the industrial sector outside of the automotive and aerospace sectors. This has been a recurring theme in this reporting season whether from a large industrial bellwether like General Electric(NYSE: GE) or a smaller niche player like Ametek(NYSE: AME). I’ve discussed these companies' results in articles linked here and here.

The second is that the nature and quantum of growth in China is shifting. We all know that China is taking up an increased percentage of global manufacturing but we also know that its reliance on export led growth cannot continue indefinitely. Europe’s growth is anemic, and the long term prospects for US growth look hampered given its public deficits. Moreover, the Chinese government knows this and is gradually trying to shift the economy towards domestic consumption. And China matters for the global players. Even a cursory look at Alcoa’s(NYSE: AA) results will demonstrate the emphasis it is placing on growth from China. Many of us that think that China has the reserves in order to ‘buy’ its way to 7-8% growth but we must recognize that its stimulus plans are likely to be different this time around.

What did all this mean for Pall Corp?

It was a tricky Q3 for Pall Corp, and the repercussions of these two changes are being seen in its numbers. Total sales fell $18 million to $640 million and investors can take little solace in the fact that excluding currency effects its sales would have been flat. On the positive side pro forma EPS for the nine months was up 11% to $2.15 with some notable cost savings being implemented while higher margin consumables increased as a part of the mix. Naturally this meant that margins went up. This is good but recall that future consumables sales rely on the system sales being made now.

In order not to cover old ground I have a primer article on Pall Corp linked here. In fact its growth prospects have progressively weakened since that article. The latest numbers imply that sales are still weakening (particularly within industrial), but at least system orders are looking relatively better at the moment.

Digging deeper into the numbers shows that Life Science sales (67% bio-pharmaceuticals,16.3% food and beverage and 16.7% medical) are doing okay with good growth from bio-pharmaceuticals (pharma is still investing) of 9% offsetting a 21% decline in food and beverage sales.

Turning to Industrial sales (59.4% process technologies, 20% aerospace and 20.6% microelectronics) it’s clear that there are some issues here. Ametek recently spoke to strong performance in its aerospace markets and it’s been a strong reporting season for aerospace companies. On the other hand it mentioned some softer than expected numbers in its process industries as well as softness caused by the heavy truck and trailer market. Indeed, this is exactly the sort of thing that Alcoa’s results had presaged when it forecast deteriorating conditions in its heavy truck markets.

Pall Corp’s process technologies sales declined 13%, and it was no surprise to see its microelectronics sales down 14% as well. The one bright spot was--you guessed it--in aerospace as sales rose 25%; but as it only makes up 9.8% of total sales, it is not enough to make a significant difference.

The conclusions are clear, outside of automotive, aerospace and parts of healthcare, the industrial sector is doing great and investors should be minded to consider factoring this into their decision making.

China?

Similarly with regards to the regional breakdown, Pall stated that its Asian sales were down 11% due to weakening in its industrial markets in China and ‘mature Asia.’ Obviously part of this will relate to tougher conditions within microelectronics and you only have to look at what Intel said to confirm this. However, Pall’s management stated that conditions were changing in China, and I think this is self evidently true from most commentary on the country. Aerospace and automotive should do fine because they are strongly related to the Asian consumer (car buying and air passenger traffic), but some of the major infrastructural markets may see a slowdown.

For companies like Alcoa or General Electric this may cause some problems, but it may cause opportunity as well. Alcoa does have significant exposure to automotive and aerospace but any weakness in China will hit its growth prospects quite hard.

As for General Electric its healthcare, transportation and aviation (which together contributed 61% of industrial profits in the quarter) should do fine this year, but its power & water division disappointed last time around (Europe was blamed), and it’s hard to read what its oil & gas numbers will be for the rest of the year. Both companies' future results are well worth looking at in this context.

Where next for Pall Corp?

Pall Corp is attractive, and it has some good long term prospects from filtration demand promulgated by environmental regulation. My concerns would be more over the short to mid term outlook. This is a stock that trades on nearly 23x full year EPS estimates to July 2013. It is hardly cheap and its outlook has been getting worse even as the share price has risen.

Clearly the market is pricing in a second half industrial recovery here with no knock–on effects from China’s shifting growth path. Even if you are comfortable with these scenarios then Pall Corp does not look cheap.

The U.S. economy remains in slow and unspectacular recovery mode, but

this fact should not deter investors. Making money in the markets is

not just about buying/selling stocks in line with the economy but, in my

opinion, more about finding stocks that can surprise on the upside

within an understanding of the future economic climate.

I think the off-price retailers are a good example of the sort of

stock that has the potential to do well in this environment. In this

article I’m going to focus on Ross Stores (NASDAQ: ROST). I will discuss its recent results and suggest some other names to look at.

Ross offers good value -- well, just about

I last looked at the stock in March in an article linked here.

Since then the stock has done well, and I think it has a bit further to

run. The recent rise is putting pressure on it to continue to

outperform, but the good news is that current trading is pretty good.

As ever with Ross Stores it is worth noting that it tends to be

conservative with its guidance. In the article linked above I referenced

its guidance of 1-2% growth in comparable same store sales growth and

suggested that it might beat that number. In the end the number came in

at 3% for the quarter, and the guidance of 1-2% for the next quarter

(and the full year) remains intact. Traffic was flat but an increase in

the average basket size helped gross margins carry on their impressive

performance.

Here is a table comparing its guidance with what it has reported:

As the notes in the graph suggest I think the market seems to expect

Ross to beat its conservative same store sales guidance each time. If

true, this could put pressure on the stock price should it fail to beat

the range given for the next quarter.

TJX is a useful company to compare and contrast with Ross because its

same store sales came in at the top end of guidance with 2% growth; but

the good news was that it guided towards 2-3% for the current quarter.

The other interesting comparisons are that TJX is aggressively expanding

into Europe and that it plans to launch an e-commerce initiative in the

second half. By way of comparison Ross’ management

declared that the economics of an e-commerce operation don’t ‘add up’

for the company. Will it work for TJX? And will either of these

companies change their minds about e-commerce?

TJX’s home goods sales have been doing well while Ross had some

disappointments last year and is somewhat playing catch-up. No matter,

its management declared itself as ‘feeling good’ about the changes and

said they were on track.

Another company worth watching in this context is J.C. Penney (NYSE: JCP). Frankly anyone would struggle to put this company’s difficulties as eloquently as Howard Davidowitz has done over the years. No prisoners taken when this guy gets fired up!

The good news is that the company has grasped the gauntlet and is

starting to offer the kind of promotions that many think it needs to.

Furthermore, it is pinning its hopes on expanding its home goods sales.

Both of these activities will potentially increase competition for TJX

and Ross, and investors need to watch events closely. The difficulty

that J.C. Penney has is that it is exactly in the kind of mid-range

retail space that this economy has ravaged.

Where next for Ross Stores?

In conclusion I think the stock has a bit more to run and I'm holding

for now. Ross forecast EPS of $3.70-$3.81 for the full year, which puts

it on a forward PE of around 17.2x as I write. In addition, this is a

heavy investment year with a step-up in capital expenditures to around

$670 million. The implied EPS growth rate of around 6.4% may not seem

like much, but lets recall that last year's earnings contained a

positive contribution of $0.10 from an extra week's sales. If you strip

that out then the EPS guidance is for a more respectable 9.4% increase.

I think a target price of around $69 is reasonable given the

risk of the extra capital expenditures (mainly to build out two new

distribution centers), the possibility that J.C. Penney might get its

act together and the chance that the market may be currently pricing the

stock to keep beating its own guidance.

I'm more of a GARP orientated investor but I occasionally I dabble in

some value stocks. I confess I get tempted by the sordid infidelity of

it all.

A few years ago a well known UK fund manager outlined one approach to

the art of value investing to me. In short it involved analyzing

companies across a sector and finding one that was under-performing

based on various key metrics, but whose management was committed to

restructuring in order to get them back in line with the industry.

Such an approach fits well with the investment thesis for buying Quest Diagnostics (NYSE: DGX) and here is why the stock is worth a look.

Quest Diagnostics diagnostic quest

For the sake of brevity I’m going to refer to a previous article I wrote in January, which outlined a five point strategy aimed at returning the company to growth and improving efficiency.

In this article I want to try and assess the progress of the

strategy. My reasoning is that if Quest can achieve the aims of this

plan then there is no reason why it can’t get back to the kind of

valuation that its rival Laboratory Corp of America (NYSE: LH) has.

I’ve broken out some metrics for potential investors to consider in this graph.

A few years ago Quest and Lab Corp generated comparable returns on

invested capital and their price/sales ratios were similar. B ut over

the years Lab Corp has executed better. Consequently the market is

willing to pay a premium for Lab Corp in terms of price/sales.Quest’s challenge is to try and sweat its assets better while getting back to long term industry growth of around 4%.

How the five point strategy is faring

In summary Quest declared that its five point program was on track.

Disappointingly it lowered its full year revenue guidance to flat from

0% to 1% but it maintained its earnings guidance of EPS between $4.35

and $4.55. Its confidence in hitting earnings numbers-despite lower

revenue expectations- is a consequence of the management’s belief in the

successful execution of its restructuring plans.

Turning to cash flow, it forecast operational cash flow

of $1bn with capital expenditures targeted at $250 millin. In other

words free cash flow is a targeted at around $750 million, which

represents around 5.7% of its Enterprise Value (EV). Given that one of

the five points is to return cash to shareholders –and Capital

Expenditures (CapEx) are elevated this year thanks to restructuring --

this makes Quest a genuine value proposition. Indeed it bought back

$63.5 million worth of stock in the first quarter (Q1) (at a price of

$57.81) and plans to use the entire proceeds of the $300 million sale of

HemoCue (a point of care diagnostics business that it bought for $420m a

few years ago) in order to buy back stock in Q2.

Turning to the other initiatives, the HemoCue divestiture plus a

couple of smaller acquisitions is evidence that the restructuring of the

diagnostic information services segment continues apace. Its

‘Invigorate’ cost initiatives appear to be on track. Having left 2012

with a run rate of $200 million, Quest declared that it expected to

reach two-thirds of the $600 million forecast for 2014 before the end of

2013. The long term aim is to hit $1 billion.

As for the administrative changes the sales force has been expanded

and is now operating in a more methodical and targeted fashion while the

new organizational structure has removed a few layers of management.

A mental check list of the five initiatives would likely see all of

them ticked off in positive fashion. So while internal execution seems

okay what of its end market environment and new developments?

What is happening in the industry?

As ever, the specter of reimbursement cuts hangs over the industry

and given the necessity to reduce public deficits it would not be

surprising to see more pressure here, even as the Affordable Care Act

adds more people into the system. Both Lab Corp and Quest see the latter

as a positive but the uncertainty over reimbursement rates remains.

While Quest gave its Q1 results in Mid-April I decided to wait before discussing them because its large deal with CignaCorp(NYSE: CI) was under renewal discussions. The good news is that Cigna renewed the deal

with a multi-year extension. It's been a good year so far for the

managed care insurers and I note that analysts have progressively raised

their full year EPS estimates for Cigna this year from around $6.34 at

the start of the year to $6.49. Cigna's upside potential lies in the

hopes that the Affordable Care Act will increase the numbers of people

able to acquire health insurance and it also has growth opportunities

from its emerging market expansion.

Indeed it is a similar story for another client of Quest.The big story with Aetna relates to its purchase of Coventry Health Care and

the possibility for Quest to gain some volume from the future

integration. It is the early days (the deal was completed on May 7) but

this holds out hope for some upside potential.

Another recent development is the extension of Quest ties with women’s health company Hologic (NASDAQ: HOLX). According to Hologic the deal is non-exclusive with an initial term of five years and is focused on its APTIMA product range (which it acquired with the purchase of Gen-Probe) and

marries Quest’s analytical abilities with Hologic’s product range. It

makes sense because Hologic will benefit from increased distribution via

Quest while giving it a broader product range in order to offer to its

customers. Hologic needs this kind of initiative because 2013 is proving

to be a difficult year for companies selling high ticket capital

machinery to hospitals. For example Varian Medical

reported a 9% decline in its North American oncology sales Hologic

themselves reduced the mid-point of its full year revenue guidance from

$2.63bn to $2.54bn recently.

Where next for Quest?

I note that Quest recently re-affirmed its full year guidance and Lab

Corp also affirmed its full year guidance of full year revenue growth

of 2-3% at the time of its results in April. In other words, conditions

in the industry don’t appear to be getting worse. Moreover the restructuring plans are on track for Quest and provided the second half growth kicks in as planned them

I think the stock is probably headed higher. The Hologic deal makes

sense, the extension of the Cigna relationship helps to de-risk the

stock and there may be some upside from Aetna. The big concern is future

reimbursement issues and they effect that they might have on the

industry. With that aside I think there is a good chance that Quest can

play catch up with Lab Corp and it may well be a good proposition for

value investors.

It would probably be an understatement to say that it has been a

difficult earnings season for companies selling into the telco service

providers. After hopes of a second half recovery in 2012 were dashed by a

second half slowdown the idea was that pick-up would be pushed into

2013. So far it hasn’t worked out like that. Indeed a host of companies

have warned and lowered guidance and even companies who don’t

exclusively service the sector like Fortinet or F5 Networks (NASDAQ: FFIV)have cited specific weakness from their service provider verticals.

With that said, what is the market to make of the recent sterling results from Ciena Corp(NASDAQ: CIEN)? Does its earnings beat and guidance raise mean that telco spending is back?

Is it the industry or is it Ciena?

Answering this question requires an understanding of where the

industry and Ciena has come from. My view is that it is more about Ciena

than being a general signal that telco spending has recovered. On the

evidence so far, the indications are that telco spending is weaker but

Ciena is benefiting from some favorable trends in the industry.

Investors in the industry would be well advised to try and stay stock

specific.

I discussed Ciena in an article earlier this year linked here,

and many of the markers that they company laid out then came into

fruition in the latest set of results. Therefore these results were

really a continuation of positive trends identified by the company. For

example in the last conference call it outlined that its Q1 was back-end

loaded and Q4 had seen record orders. Clearly that momentum continued

into Q2. In addition the product mix is getting better for gross margins

too. Its lower margin solutions are in optical transport, and they

dropped as a share of revenues from 17.7% to 11.3% in Q1 as overall

revenues rose 6.3%. Meanwhile its gross margins improved to 41.2% from

38.2%, and it believes it can hit mid-40’s margins in the future.

What is going right?

The key to the results is that the service providers are expanding

expenditures on newer technologies like 40G and 100G high speed Ethernet

networking and Optical Transport Networks (OTN). The share of Ciena’s

revenues from 40G and 100G rose to 70% from 60% in the previous quarter.

Meanwhile its management spoke to 100G and OTN spending being in the

first to second innings of a multi-year expansion.

Essentially telcos are having to adjust to huge growth in areas like

cloud computing and mobility, which are creating huge increases in data

volumes. Furthermore as the switch to wireless from wireline spending

gathers apace and 4G/LTE rollouts increase we can only expect more of

this. The question is this; if all these issues are coming together then

why hasn’t overall telco spending strengthened?

I’ve discussed the capital expenditure plans of AT&T(NYSE: T) and Verizon(NYSE: VZ) in specific articles linked here and here.

With regards to AT&T, it disappointed the industry by announcing

that its capital spending plans for 2014 & 2015 would be cut by $2

billion respectively so they would now lie at around $20 billion in each

year. This sounds like bad news but it was because it got better

deployment from its current 4G/LTE rollout and was actually ahead of its

plans to deploy 300 million 4G/LTE points of presence by 2014. Again it

outlined its shift in spending towards high bandwidth capability and

corporate mobility. Good news for Ciena, not so good for legacy

technology providers.

Similarly, Verizon talked of caution among its enterprise customers

and continued its ongoing drive to reduce CapEx as a share of revenue

figure. In a sense Verizon can do this because it began rolling out its

4G/LTE network around five years ago. But as with AT&T, its

smartphone penetration rates were higher than expected, with

significantly increased amounts of data now being carried on its 4G/LTE

network. The pressure to invest in higher bandwidth solutions in order

to meet this demand is ongoing. Again Ciena is well placed.

What is going wrong?

Ciena certainly did report strong growth from the big two Tier 1 US

carriers. In addition its management stated its international backlog

was good too. All of which is fine, but it doesn’t explain why everyone

else was so weak in the quarter. Granted plenty of other companies have

substantive legacy technology solutions (Ciena is positioned for newer

technologies) and no doubt they suffered as a consequence.

But what of something like F5 Networks? They offer application

delivery controllers, which ensure applications get moved around

networks safely and efficiently. Demand for such products should surely

increase in line with the trends discussed above. The fact that it

didn’t and other companies reported weak telco based sales is an

indication of how easily telcos can shift their approaches to spending.

Indeed, Ciena could even see some of this in future quarters. F5 has its

own question marks with a product refresh and increasing competition

but there is no doubt that its telco vertical was weak.

The bottom line

In conclusion, I think that these results were more about Ciena then

the industry. Its long-term outlook is good, but don’t be surprised if

there are some bumps along the way. As for the legacy technology

providers, this is not necessarily a good report and it is still too

early to conclude that the much-awaited pickup in telco spending is

coming soon.

Everyone loves a defensive growth story, and there aren’t many better companies in the category than Cooper Companies(NYSE: COO).

In general, ophthalmology is an industry that can grow irrespective of

the economy. Within this, Cooper has its own mix of earnings drivers

with which it can generate superior industry growth.

It is a compelling mix. In fact, so much so that the stock has gotten

away from this investor’s hopes for a buying opportunity. In summary,

the recent results were pretty good in a relatively weak environment,

and the full year EPS guidance hike is seeing the stock higher as I

write. Is there more to come?

Super Cooper

Before going into the details, here is a summary of the updated full year guidance versus the previous company estimates.

The key changes are the raising of EPS guidance (I have bracketed)

and a $10 million lowering of revenue guidance for Coopervision and

Coopersurgical respectively. The former is largely due to currency

effects and the latter is due to the kind of softness with medical

surgery that others like Johnson & Johnson (NYSE: JNJ)have reported in the quarter. In

fact, Johnson & Johnson explicitly stated that hospitals had

reported that surgical procedures were currently running at levels below

the rate that they had predicted for 2013. As for the full year

currency effects on Coopervision, we got an idea of how pervasive they

are in the current quarter whereby 11% growth at constant currency

turned into only 7% reported growth.

So while the reduction to revenue expectations was slightly

disappointing, the increase in the EPS guidance was well received. There

was no change to free cash flow (FCF) guidance.

Essentially Cooper is succeeding in its aims of trading

up customers to its (higher margin) silicone hydrogel lenses (which now

make up 43% of Coopervision revenues) and towards its one-day modality.

The latter generates 4-6x the revenue of ordinary lenses and 3-5x the

profit. All of which is good news because if we go back to the previous

set of results Cooper outlined its intention to increase capital expenditures

by $90 million in order to accelerate the sales expansion of its

silicone hydrogel based lenses. The recent results suggest that it was a

good move.

Long term growth looks assured

Going forward the long term opportunity for Cooper is obvious. The

company is catching up with its rivals in terms of its silicone hydrogel

lens penetration, and the benefits of a one day modality to the

consumer are obvious. Moreover, unlike some of its rivals, Cooper is not

encumbered with the strategic difficulty of missing out on lens care

sales (one day lenses don’t require care) because it is expanding its

one day sales. Furthermore it can expand its private label sales, and

the growth potential in the emerging world is obvious.

However, the story isn’t just about Coopervision. Its surgical

division is a strong FCF generator, and the strategy is to make further

acquisitions in the space in order to leverage its sales infrastructure.

Putting all these elements together should ensure long term growth and,

more importantly, at a rate in excess of industry growth.

What the industry is saying

Cooper reported that the market only grew 4% (at the bottom of the

expected 4-6% range) and that it expected it to grow at 4-6% for the

rest of the year. The good news is that Cooper is able to grow in excess

of these numbers. A quick look around the industry shows some sluggish

conditions. Its biggest rival is probably Johnson and Johnson, and it

reported only 1.6% constant currency growth for its vision care range;

thanks to currency effects its international vision care was down 4.4%.

It was a similar story with Novartis’(NYSE: NVO)

Alcon unit. Ophthalmic pharmaceuticals sales were up 5%, but vision

care was only up 3% and, in line with what Johnson & Johnson and

Cooper said, its surgical revenues were soft with only 2% growth being

recorded. Alcon is not a huge part of Novartis' revenues, but it is of

strategic important to the company and complements its generic and OTC

pharmaceuticals activities.

However, the big news in the industry in the quarter was Valeant Pharmaceuticals'(NYSE: VRX)

agreement to purchase Bausch & Lomb for $8.7 billion. It is

certainly a busy time for Valeant as it attempts to integrate Medicis as

well as prepare for Bausch & Lomb. Interestingly Valeant disclosed

that Bausch & Lomb grew revenues at 9% last year (although this

includes its surgical segment). Valeant talked about generating $800

million in cost synergies by the end of 2014, but this does not mean it

won’t be investing in eye-care. In fact Bausch & Lomb’s strength in

emerging markets is complimentary to Valeant’s North American focus, and

eye-care, dermatology and aesthetics are good bed-fellows in terms of

strategic development. We can expect increased competition as a result

of this deal.

I would summarize the industry background as being stable but slightly weaker than might have been expected.

Where next for Cooper Companies?

In conclusion Cooper Companies is a very attractive company that can

achieve good revenue and margin growth even if the economy slows. In my

opinion its evaluation should command a premium over the market but, as

ever, the question is how much do you want to price in? The

‘defensive’ sector has certainly led the market this year, and many

stocks within it (particularly food stocks) are starting to look toppy

to me.

As I write this, Cooper Companies trades on $120 and an enterprise

value (EV) of $5.85 billion. Interpolating from my table above, this

puts it on a forward PE ratio of 19.3x and a forward FCF/EV yield of

only 3.1%. As much as I like the stock I am still going to truculently

go away, sit in a corner and mumble that it’s too expensive right now

while patiently waiting for a dip.

You can either pay sky high evaluations for big data plays or buy a backdoor entry into the sector with a company like Verint Systems(NASDAQ: VRNT).

Companies that already use Verint's customer interaction capture

hardware will increasingly want to buy its data analytics software and

services in order to analyze the captured data. I’m sympathetic to the

argument, and hold its rival and potential partner NICE Systems(NASDAQ: NICE). With that said, recent results from Verint were a mixed bag, and the stock looks fairly valued for now.

Verint reports mixed data

Verint’s first quarter numbers were pretty much in line with expectations, but as I wrote about the last results,

investors would have been justified in expecting a bit more from the

company. Its management was upbeat last time but, like a lot of

technology companies, this quarter's results were mixed.

In short, Europe, the Middle East and Africa proved to be a headwind,

while the Asia-Pacific region’s growth was strong enough to counter it.

European growth is now expected to be near flat for the full year

versus previous expectations of small growth. This affected its core

Enterprise Intelligence business and meant that it only grew by 1.2% in

the quarter as opposed to the total revenue growth of 2.6%.

In order to see how Verint generates its revenues, I’ve broken out 2013 segmental revenues below.

In geographic terms, the first quarter saw 54.6% of its $205 million

in revenues coming from the Americas, with Europe, the Middle East and

Africa contributing 20%, as opposed to 25% for the first quarter last

year, and Asia-Pacific with 25.4%. While the Europe, Middle East and

Africa decline of $9 million was unwelcome it wasn’t enough to put a

dampener on the overall results.

Communications intelligence is an area where Verint is stronger than

NICE, and it demonstrated an impressive 7.2% revenue growth. The

government vertical is large for Verint -- traditionally around 25% of

revenues -- and there were some concerns that it would be affected by

the sequester. Clearly these worries turned out to be misguided, and

Verint’s international exposure certainly helped. In addition, this type

of intelligence gathering and surveillance activity is not going away

anytime soon.

However, the biggest positive surprise was probably that the video

intelligence segment revenues only fell by 1.7% after declining 13.4%

over the last year. There was some discussion in the conference call of

increased interest following the tragic events in Boston and such events

emphasize the need for expenditure on these types of solutions.

Elsewhere in the segment a $4 million order came in from a big box

retailer in order to help it reduce shrinkage.

Long term growth drivers

Putting these elements together demonstrates that the key drivers of

Verint’s future growth are still in place. As argued in the conference

call, customers likely want to buy solutions from a single vendor and as

Verint already has a substantial installed base with its data capture

solutions, it can expect future growth. In addition it has a number of

secular drivers in its favor. For example, even in a slow economic

environment, financial institutions generate growth by investing in

analyzing existing customer interactions. Similarly reducing fraud and

money laundering will always be a part of a financial firm or contact

center’s operations.

Indeed, a quick look at NICE Systems' recent results

revealed these positive underlying trends. Similar to Verint it kept

full year guidance intact. NICE is seeing an increased willingness among

its customers to sign bigger deals and integrate its analytics

solutions with its product sales. NICE is well positioned to do this,

particularly to its string verticals like financials and contact

centers, because of its partnership with IBM(NYSE: IBM).

Back in October, NICE announced that it would be integrating IBM’s big

data analytics software within its solutions. It’s a mutually beneficial

solution because IBM will get entry into NICE’s installed base while

also giving NICE added functionality with which it can add value to

customers.

The interesting thing about IBM’s results

is that they somewhat presaged weaker conditions for IT enterprise

spending and set the tone for a disappointing IT earnings season. The

fact that NICE and Verint reported results that were pretty much in line

and kept full year growth expectations is therefore somewhat of a net

positive.

Where next for Verint?

Full year guidance is for 6%-7% growth and earnings of around

$2.75 and free cash flow generation of around $100 million. At the

current price this makes for a forward PE of around 12.8 and a free cash

flow yield of around 5.3%. All of which is pretty fair value for a

company forecast to generate single digit earnings growth over the next

couple of years. I suspect the stock is also being

supported on the back of speculation over a possible acquisition by

NICE. It’s worth monitoring but hard to make a case that it is great

value right now despite the positive long term prospects.

The most surprising thing about Palo Alto Networks'(NYSE: PANW)

recent results were that the market was surprised by them. In truth it

has been a difficult first quarter for technology companies, and despite

having defensive characteristics (IT security threats are definitely

not going away) its sector hasn’t been oblivious to the difficulties. In

summary Palo Alto missed estimates and guided lower than the market

consensus with the usual concerns over Europe and Government coming to

the fore.

Palo Alto gives little succor

Probably the most interesting aspect of these results was the timing. Its security rivals like Check Point Software (NASDAQ: CHKP) and Fortinet (NASDAQ: FTNT)

had already given weaker than expected results amid talk of customer

hesitancy (partly due to sequestration fears) and a faltering macro

environment. If this was to prove temporary then we might have hoped

that Palo Alto would report better conditions given that it is already

June. Unfortunately it intimated that things got worse in April (the

back end of its quarter), and performance in May was only ‘in line’ with

its adjusted guidance.

Here is a chart of Palo Alto’s performance.

Note that product revenues saw a sequential decline in the quarter,

and while the revenue guidance for Q4 of $106 million to $108 million

implies a near 43% rise in revenues (at the mid-point), it is below the

market estimates of $113.7 million. On such things do tech stocks soar

and crash.

To put this into context, Fortinet had already warned, and as articulated in an article linked here,

it will have to see a bounce back in the second half in order to hit

even the lowered guidance. Palo Alto’s recent statements would not

suggest that underlying conditions have improved much so I would suggest

taking Fortinet’s word (that Q2 would be similar to Q1) at face value.

In addition Fortinet stated that its service provider revenues were weak in the quarter. This is a similar story to what F5 Networks (NASDAQ: FFIV)

outlined over its application delivery controller based revenues too.

The good news for Palo Alto is that, although it did see some ‘softness

on its service provider based revenues, they do not make up a

significant part of its overall revenues.

What caused the miss?

It is really about sequestration effects and Europe, specifically

Southern and Central Europe. Palo Alto saw a $3 million-$4 million

shortfall in sales from this region. Overall EMEA sales declined 4% on a

sequential basis. As for federal work the weakness seen

was largely a consequence of sequestration effects. We can also see

these effects on federal spending in a detailed look at F5 Networks' recent results. With regards to F5 specifically, I note that Citrix Systems

had a pretty good quarter with its rival product, and since F5 is

undergoing a product refresh there may be other factors at play here.

With regards to competition there were a couple of interesting points made in the conference call. Firstly,

Palo Alto’s management doesn’t feel that ‘bundling’ will get the job

done anymore. I suspect this is a reference to competitors like Cisco Systems or Juniper Networks who

may well try to include security solutions as part of their networking

offerings. Indeed, Cisco’s security revenue growth turned negative in

the last quarter.

Second, there were the usual references to beating out Check Point

and others in the presentation. As a young and fast growing company we

should expect Palo Alto to be replacing the installed base of

competitors, but in retrospect Check Point’s recent results were

relatively good, and there are some signs (average selling prices

rising) that it is getting over the hump of convincing its customers to

buy its upgraded products.

Where next?

It’s hard to be overly positive because it would have been useful if

Palo Alto had reported better conditions in April/May but, the fact is

that they did not. With that said the bullish case sees the

sequestration effects as causing some short term reactions, much of

which will be ironed out later in the year. Sequestration has its most

obvious influence on public expenditure, but it will also affect the

private sector because the former uses the latter. However, once the

fear of the unknown recedes then companies like Palo Alto and Fortinet

can hit their revised guidance.

The bearish case argues that these effects will continue to slowdown

the IT market as the knock-on effects ripple through the economy and

guidance will have to be lowered for many of these companies. Meanwhile

the situation in Europe is hardly looking much better with sovereign

debt issues remaining at the forefront of concerns.

Since we have never had sequestration before, it is hard to know

which approach to take! My gut feeling is that things won’t get much

worse. Unemployment is falling in the U.S., and growth is moderate but

constant, while the housing market is picking up. F5 Networks has some

uncertainty about it and Check Point needs to demonstrate it can get

back to product revenue growth. However, if you are going to buy Palo

Alto and Fortinet then this could be a decent time to start thinking

about picking some of these names up.

The latest results from Dollar General (NYSE: DG) were met with a sharp mark-down as they disappointed in terms of both the sales and margin outlook.

In general the dollar stores are attractive for their defensive

properties, but many of the headwinds that began in mid 2012 are still

around and they are finding growth a lot harder to come by. In summary

Dollar General’s results raised more questions than answers and the

current valuation still makes it a difficult stock to get too excited

about.

Dollar General disappoints

After a disappointing quarter Dollar General declared that its

expected sales growth rate and gross margin performance for the full

year would be less than it had -only recently- predicted.

There were a few reasons cited and I have pulled out the salient points below

Payroll taxes, tough weather comps and sales headwinds from tax refund delays hurt the current quarter’s results

The sales mix contained a

larger amount of consumables which tend to be lower margin. Furthermore

even within consumables there is a shift to lower margin consumables

Inventory shrink was larger than expected

Increasing tobacco sales are naturally reducing margins

The issues hurting consumer’s income were somewhat expected (and

Dollar General had previously argued that this would be a weak quarter

anyway) but the sales mix concerns were somewhat more surprising. For

example, Dollar Tree(NASDAQ: DLTR) had recently given results and notably pointed out that its discretionary sales were growing faster than consumables. This suggests that Dollar General’s issues might not be solely down to tighter customer wallets in the quarter.

Moreover if we look at how Family Dollar(NYSE: FDO)has performed in recent times,

we can see that comparable sales growth has been achieved in a climate

of falling gross margins. In short, Family Dollar tried to expand its

non-consumables sales (mainly home based and apparel) and ran into

difficulties as it found it hard to sell higher margin products to its

customers.

In summary, Dollar Tree did fine with expanding discretionary sales

and therefore gross margins, but Family Dollar has had problems doing

this (particularly last year) and now Dollar General is lowering

estimates thanks to lower-than-expected discretionary sales.

My feeling is that Dollar General’s difficulties are more a

consequence of the difficulty in increasing higher margin sales. It

seems that hard pressed consumers feel more inclined to shop for

consumables in its stores. As to the weather effects, if they had

significant effect on discretionary sales then why wouldn’t the

management raise guidance now that spring weather has arrived?

Comparable same stores down across the industry

As ever it is useful to compare how same store sales are faring

across the industry. Please note that these numbers are adjusted to the

calendar year as these companies have different reporting periods.

It’s clear that same store sales growth started slowing in mid 2012.

Family Dollar did achieve some growth but, as discussed above, that was

largely a consequence of an expansion in lower margin product sales. The

dollar stores are seeing slowing comparable same store sales growth and

traditional grocers (Safeway, Kroger etc) are starting to fight back through engaging customers with pricing and promotional activity.

While these issues are affecting the industry there has been no let

up in their store expansion strategies. Indeed Dollar General affirmed

that its number one investment priority was to open new stores. Indeed

it is planning $575 million to $625 million in capital expenditures and

hoping to open 635 new stores while relocating/remodeling around 550

stores. Is this push for growth, by the whole industry, a wise strategy given that same store sales growth is slowing?

Are the dollar stores good value now?

As ever we need to put the growth prospects in the context of

valuation. Dollar General’s forecast for comparable same store sales

growth of 4-5% isn’t bad in a slow economy and its earnings are forecast

to grow double digits over the next few years. On the other hand none

of the dollar stores look particularly cheap right now and the expansion

plans are impacting the generation of free cash flow.

For companies in a growth phase I like to equate their capital

expenditures with depreciation in order to create an adjusted free cash

flow number.

In conclusion I think it’s still time to hold fire on the sector

right now. It's probably better to follow its customers and hold out for

a discount.

The housing sector remains a favored play amongst investors and Williams-Sonoma’s

latest results highlight the attraction of the sector. The company is

firing on all cylinders and benefiting from a number of growth drivers

that are helping to push its stock to all-time highs. Is now the time to

pile in or to start to take profits?

Williams Sonoma confirms growth momentum

I last looked at the stock in a previous article.

The salient points raised then related to the necessity for the company

to expand its online activities and international expansion programs.

Both are needed in order to allow the stock to grow into its evaluation.

With a price-to-earnings ratio of around 20 times, it was hardly

cheap. The company was stepping up capital expenditures this year to a

range around $200 million to $220 million. All expansion programs come

with risk, and there are no guarantees that international markets will

take to its products as well as they do in the U.S.

The good news is that, if the latest set of results are an accurate precursor to future events, I

think that the company is slowly de-risking these fears. Here are its

key profit growth drivers, as previously discussed by the company.

Overseas expansion with an immediate focus on Australia and the Middle East

Investing in expanding West Elm and Pottery Barn

Expanding its e-commerce facilities and direct-to-consumer (DtC) offerings in general

Supply chain investments in order to drive multi-channel sales and margin expansion

Continue to offer differentiated products in order to remain competitively relevant against online competition

One thing that is clear from these expansion plans is that all these

measures are integrated into one coherent plan. Williams-Sonoma is one

of the most integrated multi-channel distributors in the U.S., and as it

expands internationally that approach is being taken there as well.

The Australian expansion is working very well so far. Management

describes itself as being "literally overwhelmed" by the response rates

in its retail stores and e-commerce sites. It is currently planning on

opening a new West Elm store in Melbourne, Australia, and moving in to

London as well. Of course, the company needs these launches to go well

because it needs to counteract the effects of short-term margin

contraction that occur when investing in new sites. I would read the new

store plans as a marker that the expansion plans are going well.

Moreover, the investments in e-commerce and multi-channel sales

efforts are also working well. For example, the company managed to

achieve a credible 1.9% growth with the core Williams-Sonoma brand in

comparable-brand revenues. The brand hasn’t been growing in

a while and it’s not a big part of the expansion programs as a result,

but the improvements were cited as a consequence of more efficient

e-marketing activities. To put this into context, total company revenues

grew 8.6%, with debt to cash up 11.9% (including high-teen growth in

e-commerce), while retail channel growth was only up 5.8%.

Interestingly, the company is seeing strong demand from online

purchasers who wish to pick up products in-store. This apes the strategy

of Pier 1 Imports , which has invested significantly in ensuring that its customers can engage in in-store pickups.

The company's key growth brands West Elm and Pottery Barn recorded

double-digit and high-single-digit increases in comparable-brand

revenues, respectively. Moreover, the company can expect more growth to

come because new home purchases tend to spur home furnishings purchases.

This is something to look out for because thus far we haven’t seen

large increases in new home purchases in this recovery. What we have

seen, however, has contributed to earnings upgrades at home improvement

stores like Home Depot and Lowe’s Companies.

What the industry is saying

In general, there have been a strong set of earnings for the home

furnishings sector and it has momentum going into the second half of

2013. What makes the sector interesting is that a number of retailers

within it have some good internal drivers to go along with positive end

demand.

For example, Restoration Hardware is engaging in a growth strategy

which involves rolling out new full-line stores. The idea is to try and

put more of its product offering on display in showrooms. The existing

full-line galleries are exceeding expectations, and the company recently

upgraded its revenue and earnings forecasts. In addition, the company

is seeking to generate revenue and margin expansion through expanding

into categories like art and objects of curiosity.

Like Williams-Sonoma, Pier 1 Imports is also aggressively engaging in developing a multi-channel approach to retailing. Its plan is

to invest in point-of-sale in-store systems that will help to drive

e-commerce sales in future. I noted that the Wiliams-Sonoma’s management

cited how strong the growth in revenues was from online customers who

wanted to pick up good from the store; this has actually been a key part

of Pier 1’s strategy, and the fact that a fellow home furnishings

company is saying the same thing suggests it is following the right

path.

Where next for Williams Sonoma?

Having previously looked at the company and concluded that its stock

looks fairly valued at 20 times earnings, I now find myself saying the

same thing! Of course, the stock has gone up from around $50 to mid

$50’s (as I write this) but I would argue this is largely a consequence

of the upgrade to its forecasts that was contained in its recent

earnings results. And therein lies the rub. The company is performing

very well, but much of this is already considered in the price and

investors seem to be relying on earnings upgrades in order to take the

stock higher.

It’s not a stock I would be chasing right now but it is well worth a

look if we see a dip in the markets because it does have good prospects

and the management is executing very well with its multi-channel

approach.

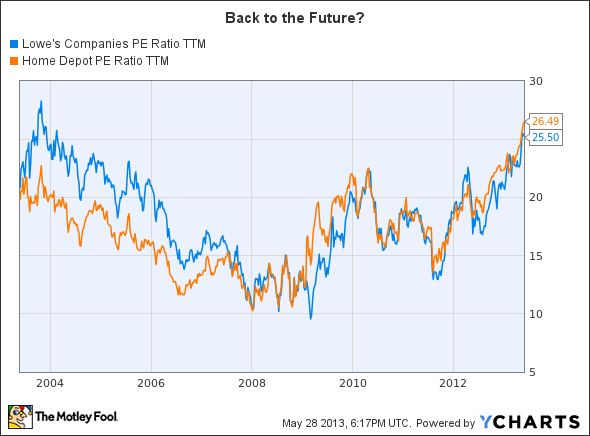

Investing in anticipation of a housing recovery has been one of the best trades of the last year, but with things like the home improvement stores Home Depot(NYSE: HD) and Lowe’s Companies (NYSE: LOW) hitting new highs is it time to start thinking about reducing your weighting in the sector?

My rationale in asking this question is not to question the validity

of the housing recovery but rather to highlight the fact that there may

well be other stocks related to it that are have better valuations.

Moreover a recovery in the U.S. housing market usually precedes

recoveries in other areas of the economy where investors may find

investment opportunities.

Home Depot and Lowe’s Companies report

Home Depot’s recent results were certainly better received--initially

at least--than Lowe’s Companies, but no matter; both stocks rose

afterwards. The truth is that the market has woken up to the housing

recovery and wants a piece of investing in it. As for the results, Home

Depot continued its recent tradition of raising full year guidance.

Here is how Home Depot has tended to hike guidance over the last few years.

As the housing recovery as strengthened so Home Depot has continued

to upgrade its full year revenue estimates. It is now three quarters in a

row that it has done this, and in this set of results it noted that its

pro business had started to grow quicker than its consumer business.

This is a positive sign of recovery, as pro sales are seen as more

discretionary-based.

Furthermore the recovery it is seeing in its end markets

is becoming geographically spread with areas that were at the epicenter

of the housing crisis (California, Florida, Arizona, etc) starting to

recover as well.

With that said there were some challenges in the quarter with the

spring weather starting a lot later than last year. This made

comparables for things like garden and outdoor products a lot lower for

Home Depot. However, it said that April saw a strong snap back in growth following a weak March, and May is similarly strong so far.

It was a similar story with Lowe’s Companies. It reported comparables

down 10% in March, with April rising 10% and May continuing the

positive momentum. In addition, the weather affected its outdoor

comparables so that they were down 7%, with indoor rising 3%.

In fact the message from the macro front was pretty much the same.

The key operational difference between the two is that Lowe’s has

execution risk/return from its reset program. I’ve discussed this

initiative in more length in a previous article.

Lowe’s is aiming to complete the resets by the end of the year and

announced that the percentage increased from 30% to 50% in this quarter.

Unfortunately the weather effects helped to ensure that inventory

normalization only increased from 20% to 30%, but if what both these

companies are saying comes true, then this number should increase in

future for Lowe’s.

A note of caution

In summary, both these stocks have upside from a recovering housing

market and upside prospects in the current quarter as spring weather

finally kicks in. Moreover, Lowe’s should see some upside potential as

the benefit of the resets drops into the bottom line. So, why the note of caution?

My only concern here is that these stocks have come a long way, and

now most investors will have somewhat priced in a housing recovery. A

look at their evaluations suggests that they are at levels above what

they were when the housing industry entered a recession in 2006.

Frankly I think that momentum and ongoing positive news on housing is

going to take these stocks higher. However, investing is about trying

to find the optimal ways to generate returns from your views. With this

in mind I think it is time to look beyond the evaluations at the home

improvement stores and look at some of the wider housing and

construction plays.

Two housing and construction plays

Housing recoveries usually predate construction related improvements.

New housing projects get developed which leads to new commercial

construction. In this regard I think Whirlpool(NYSE: WHR) and Stanley Black & Decker(NYSE: SWK). The interesting thing about Whirlpool is that it offers upside from its push to increase margins.

Given that home improvement stores are reporting good numbers it is

reasonable to expect that Whirlpool will see a strong spring too.

Moreover, we are hitting the 10 year anniversary of the peak of the

housing boom so the replacement cycle should start to kick in soon as

well. The stock trades on a forward PE of 13.3x and traditionally

generates large cash flows.

Turning to Stanley Black & Decker, this stock has upside potential from a housing recovery and a strategic growth initiative with which it intends to generate growth via expanding in selected verticals while benefiting from ongoing merger synergies.

Its recent results were a bit disappointing, but like

Whirlpool it was affected by some temporary weakness in Latin America

(both companies argued that it will rectify in future quarters) and from

the weather effects of a late spring. At the time of both these

companies results I was slightly skeptical over the weather argument but

now that Home Depot and Lowe’s have confirmed its effect and, more

importantly, argued strongly that growth will come back.I think this is a

good sign for Stanley Black & Decker. Moreover the stock trades on

trades on a forward PE ratio of 14.6x and is forecasting $1 billion in

free cash flow this year.

The aerospace industry is faced with some unusual end market prospects

for the next few years. In previous cycles, commercial aviation was

characterized by extreme cyclicality and ongoing profitability issues as

government sponsorship of national airlines tended to encourage over

capacity. By way of comparison, military spending was always more stable

and tended to provide a useful counterweight in difficult economic

times. How times have changed!

The current situation is different. Commercial airline profitability

is coming in better than expected and I think we can expect more upswing

in this recovery. For the sake of brevity, I can’t go into the reasons

why, but there is a more in-depth discussion on the issue linked here. On

the other hand, horrendous sovereign debt issues in many countries are

creating the necessity for pro-long term growth measures like cutting

public spending (sic), and cutting defense spending (particularly on

hardware) is a key component of this.

Which stocks could benefit?

With these kind of industry dynamics, investors should be favoring

stocks exposed to commercial aviation and one useful idea is cabin

interior manufacturer B/E Aerospace .

The company benefits from new and retrofit of cabin interiors. My point

is that if airlines are seeing more stable long-term financial

conditions, then they should be more inclined to retrofit their older

aircraft. As a consequence, analysts have B/E Aerospace on 20%+ earnings

growth rates for the next few years. All of that can disappear in a

flash should the global economy falter, but for now the stock looks

attractive.

Another stock worth looking at for its secular growth prospects is Hexcel(NYSE: HXL).

Hexcel’s attraction is that it is the global leader in lightweight

advanced composites. With the trend towards wide bodied aircraft firmly

in place, the pressure to increase the usage of lightweight components

will only increase. Similarly, if we are in a world of $100+ oil prices,

then airplane manufacturers will have to try and reduce aircraft weight

(the most effective way to reduce fuel costs). Indeed, I note that

Hexcel reported revenue from Airbus and Boeing programs being up 20% in

the last quarter with the 787 Dreamliner being a particularly composite

heavy airplane.

What about Heico?

Another stock that I think could be a beneficiary is Heico . Its operations are split into the Flight Support Group (FSG) and Electronic Technologies Group (ETG).

The FSG is involved with offering parts, repair, and distribution to

airlines. It tends to be cyclical, as airplanes will require more

servicing as they rack up more air miles. Moreover, it has some

interesting secular drivers because airlines are increasingly looking to

cut costs and outsourcing this activity offers them the option to do

this. The ETG offers various aerospace components to a mix of commercial

and government customers. Traditionally, military-based spending makes up around 20% of Heico’s revenue.

Given the changed dynamics of the aerospace industry, I think its

long-term prospects are excellent. Provided global growth is good, it

can benefit from the increased profitability and financial stability of

the airlines.

Heico lifts off

The recent results pretty much confirmed this view, and the stock has

taken off since they were released, but is now the time to be chasing

the stock price? Before I get into the details, readers should note that

I have a primer on the company linked here.

Here are the key takeaways from the latest results

FSG reported record results

and exceeded expectations as sales and income grew 10% and 14%,

respectively. However, Heico argued that this was largely a consequence

of its group leaders execution rather than any ‘rising tide’ in the

industry.

Sequestration affects have already been felt in its short cycle business and Heico is expecting more of an effect in a ‘6-9 timeframe’ and ‘continued deterioration’ in its domestic defense related revenue.

ETG saw sales rise 10% and

income up 32% as operating margins rose 400 basis points, helped by

increased space based sales which tend to be higher margin. This is a

positive, but space revenues tend to be variable and contingent upon

program funding.

The Reinhold acquisition is expected to be earnings accretive this year.

The full year revenue

guidance was raised to 8% to 10% growth from its earlier estimate of 6%

to 8%, and net income growth was raised to 11%-13% from the previous

9%-11%. My interpolation from company statements is that free cash flow

could come in at $120 million for the full year.

In a sense, I think that the full year guidance hike was partly

predictable from the company’s statements in the last report. As noted

in my link above, management did remark that they tend to be

conservative in their guidance.

Where next for Heico?

Putting all of these things together would paint a picture of a

company firing on all cylinders amid some favorable market conditions.

On the other hand, investing is about finding the best value proposition

rather than buying a stock when all the good news is already in the

price.

As discussed in the bullet points above, Heico is going

to have to deal with sequestration issues which will affect

defense-related revenues. The space industry is somewhat variable and

the FSG will have to keep executing at the current high level to drive

future upside. So, there is some risk here. On a forward free cash flow

yield of 4.5% (according to my calculations), I think it is fairly

valued and better to wait for a dip before buying into this high quality

company.

In the end, numbers are just numbers and while they are an

indispensable part of an investor's self-assessment, they do not always

reveal the full details. For example, my last month closed with a

negligible loss but the truth is, I started the month notably down after

two profit warnings on the last day of April. In retrospect, it was a

pleasing month and I think there are some useful conclusions to be drawn

from it.

For the record, I'm down 2% for the quarter but up nearly 34% on a yearly basis. Readers can access previous write-ups here.

April was a bad month for me, and much of that under-performance can be

traced to decisions made in February, of which the articles linked

below solely pertain.

Buy or sell when in doubt?

One of the hardest questions for any investor to deal with relates to

what to do when you see short-term earnings risk but long-term value in

a stock? If you sell out in anticipation the stock could easily fly

away from your estimate of 'fair value' if it delivers a decent set of

results. However, if it warns, you are delivered with a good buying

opportunity.

Moreover, if you do decide to hold over the results and the company

lowers and misses guidance, do you buy more or dump the stock? Frankly, I

think the answer to the last question depends on your view of why the

company missed.

For example, plenty of tech stocks missed in the last earnings season

and I've argued here this is could be a good chance to start picking

some up. The market is bidding up other sectors in anticipation of a

resumption to growth in the second half, so why won't technology take

part in this growth? Indeed, many of the statements of the leading tech

companies (IBM, Oracle, etc.)

specifically cite short-term hesitation (caused by sequestration fears)

by customers in closing deals but at the same time, growing pipelines.

The usual format below with links to the articles discussed. All of

them are from February and performance numbers are from the day they

were originally published on the Motley Fool.

It is a story of tech weakness and a conglomeration of the sort of factors that can gang up and assault the innocent investor. Intuit managed to report a weak tax return season and Regal Beloit

managed to lose a key customer and warn that the commercial

construction market wasn't as strong as it had previously expected. Ixia disclosed some accounting errors and then gave a (somewhat expected) disappointing earnings report. I bought some Fortinet after the warning, having been cautious over not holding too much tech going into the earnings season.

Those that warned

As ever, the key thing with investing is to hold your nerve and see what looks interesting. The first stock to consider is Citrix Systems(NASDAQ: CTXS),

which reported a mixed set of results. On one hand, its growing

application delivery controller Netscaler demonstrated that it was

probably growing market share against F5 Networks' rival solution. One

the other hand, Citrix's core virtualization solutions reported

disappointing results as customers seemed to hesitate in making

purchases, thanks to taking time to appraise the Q1 release of its

XenMobile solution. The result was that its full year EPS guidance of

$3.08-$3.11 fell short of analyst estimates of $3.14.

Frankly, I don't think this is a big deal and, if enterprise

technology spending bounces back, these estimates could prove

conservative. Citrix generates a lot of cash flow and its explanation

for the earnings miss is plausible.

The next interesting stock is Allergan(NYSE: AGN). Its mix of ophthalmic products and Botox gives it impressive defensive growth prospects. However, the stock has taken a near-term hit,

thanks to some disappointing clinical trial developments. It is

inevitable that some will sell out when these things happen, but

investors need to consider that the stock looks good value even if they

(conservatively) assume no contribution from DARPin (macular

degeneration) or Bimatoprost (scalp hair loss) in future.

Analysts have it on mid-teens earnings growth for the next few years

even without any contribution from these two programs. Given its near 5%

current free cash flow yield, I think it can 'do its earnings' in

returns from here. I bought some.

Those with momentum

I would argue that Sherwin-Williams(NYSE: SHW) and Colgate-Palmolive(NYSE: CL) are good examples of companies that have momentum behind them but are arguably on stretched evaluations right now.

The housing trade has been winning lately, and very few companies

have done better than paint company Sherwin-Williams over the last year.

Its correlation to the U.S. housing market is obvious and the company

should do well over the next year. The problem is that everyone else

seems to think so too and the stock's evaluation of around 30x current

earnings leaves little room for error. Even a cursory look at its

evaluation...

As for Colgate-Palmolive, I think the market has been keen to bid up

blue chip consumer staples and the company has certainly executed very

well in recent years. My question is, can it continue? It is in a highly

competitive industry and the likes of Procter & Gamble are responding in its core North American market.

Furthermore, Colgate is embarking on a four year growth and

efficiency program intended to drive growth in emerging markets. In

order to achieve this, it will need to continue to lead the field with

innovation. This creates pressure and given that it's on an evaluation

of nearly 24x earnings with only single-digit earnings growth priced in,

I don't think it is good value yet.

There is always value

I'm not the biggest fan of value investing, but it is notable how well NetApp(NASDAQ: NTAP)

performed in an otherwise difficult market for technology. Despite the

nice rise, NetApp still has around 35% of its market cap in net cash or

financial instruments. Furthermore, it has generated around $1.1 billion

in free cash flow (my calculations) over the last year. This equates to

around 13% of its enterprise value as I write. Moreover, analysts have

it on mid teens earnings growth for the next couple of years.

Quite clearly, the market is worried about something here and it is

likely to be a combination of its Government and European exposure in

the near to mid-term. As for the longer-term, the storage industry does

face some existential questions over how data will be stored in a cloud

computing age and will a smaller player like NetApp be a winner in such a

world? I do not know the answers to these questions, but those with a

stronger view may well be interested here

Investors had a right to feel a bit cautious about what Patterson Companies(NASDAQ: PDCO) might say in its full year results, but in the end the results were quite good.

Its end market conditions are not ideal and its hard to see the stock

recording rip roaring top line growth over the next few years. On the

other hand, it offers investors a good value proposition coupled with

decent earnings prospects and some upside from an improving economy.

Moreover, its downside is somewhat protected by the core stability of

its dental earnings.

In summary, Patterson is an attractive stock for cautious investors

or those looking to balance the cyclical end of their portfolio.

Patterson Companies reassures investors

It might seem contradictory to refer to the need for Patterson to

reassure investors while also mentioning its stability, but there were a

few short term questions going into these results. I’ve noted three of them below.

Its rival Henry Schein(NASDAQ: HSIC) had spoken of a pull forward effect in Q4

caused by speculation over the potential loss of a tax benefit.

Although Patterson had said in February that this wouldn’t have an

effect on its numbers, the issue was likely to still be on investor’s

minds.

Its consumables and core equipment sales had been weak in the back half of the calendar year, and the fear was that this could extend into this year.

The overall economy hasn’t grown strongly, so the macro pressures on dentists were still likely to constrain spending.

All of these fears were pretty much allayed in Patterson’s results.

The pull forward effect didn’t really occur for Patterson, and I’m

wondering whether Henry Schein saw this because its sales force

emphasized this in Q4. Moreover, Henry Schein has a couple of major

trade shows that should help it report good Q2 numbers. Like Patterson

it is not the most exciting stock, but if you are looking for solid cash

generator with limited downside and moderate upside Henry Schein could

fit the bill. Analysts have it on near 10% earnings growth rates for the

next couple of years. Nothing wrong with that!