This blog is devoted to helping investors make informed decisions. It will be regularly updated and provide opinions on earnings results. It is not intended to give investment advice and should not be taken as such. Consult your investment advisor.

Investors in health-care giant Johnson & Johnson(NYSE: JNJ)

have been rewarded with a 30% share price rise in the last year. The

health-care giant remains a go-to choice for investors seeking a

relatively recession-proof stock with a decent dividend. However,

investors need to ask themselves a few questions about its recent

results: Can this share price run continue? Does Johnson

& Johnson still provide compelling value? And what are the key

takeaways for the healthcare industry from these results?

Johnson & Johnson delivers

The argument for buying Johnson & Johnson is based on the fact

that its three big near-term factors depend on how its management

performs, rather than purely on the economy. This means that the stock can appreciate even in a weak economy.

First, Johnson & Johnson has been trying reintroduce

a number of over-the-counter (OTC) products that were taken off the

U.S. market due to production issues. Second, its pharmaceutical

division has several new drugs with which it can develop sales. Finally,

the successful integration of orthopedic company Synthes in its medical

devices and diagnostics division will create earnings growth in a weak

medical spending environment.

A checklist of these three factors would conclude that the company is well on track.

The company's plan to reintroduce 75% of those lost consumer brands

by the end of 2013 was confirmed in its recent second-quarter results. U.S.

OTC sales were up 17.4% in the quarter, and although they only

currently compose 7.9% of total consumer sales, the marginal increases

in sales and profits will make an impact in future quarters.

Furthermore, its pharmaceutical division has delivered

strong performance, with a 12.9% rise in constant-currency sales in the

quarter. The standout performers within pharmaceuticals included newer

drugs like Stelara (psoriasis), Incivo (hepatitis C), Xarelto

(anti-coagulant), Invega Sustenna (anti-psychotic) and Zytiga

(castration-resistant prostate cancer), all of which recorded sales

growth at around 50% or more in the quarter. In addition,

its biggest drug, Remicade (rheumatoid arthritis), which contributes

nearly 24% of its pharmaceutical sales, saw sales rise an impressive

10.3% in the quarter.

Lastly, the Synthes acquisition is working well. Indeed, J&J's

overall growth in the medical devices and diagnostics sector was 12% in

constant currency, largely thanks to Synthes. Excluding

the acquisition, the division would have reported sales growth of just

0.5%. It’s clear that the acquisition is helping Johnson & Johnson

generate growth within a difficult part of the health-care industry.

It’s all in the price

The problem for investors wanting to buy in is that the market now

seems to have priced these three factors into the share price. Compare

Johnson & Johnson's price-to-cash flow multiple with its price

chart:

The stock hasn’t traded on a price-to-cash flow multiple of around 20

since 2005-2007. A cursory glance at the chart would reveal that the

share price struggled to appreciate in that period. On the basis that it

currently trades on that valuation, I would argue that much of the good

news is already priced into the stock. Furthermore, analysts have

earnings growing in only the mid-single digits for the next two years,

and I’m not sure I’m keen to pay 24.5 times earnings for that kind of

growth profile.

Winners and losers from Johnson & Johnson’s results

It’s always fascinating to read between the lines of Johnson &

Johnson’s results and pick out indicators for other companies’

prospects. On the positive side, investors in eye-care specialist Cooper (NYSE: COO)

will be interested to hear that Johnson & Johnson recorded 5.4%

operational growth in its worldwide vision care business, and

specifically cited daily lenses as an area of growth.

This indicates strength within the eye-care market, and should be good news for Cooper Companies, since one of its key aims in 2013

is to increase its one-day modality sales. Cooper’s one-day lenses

generate three to five times more profit than its monthly lenses.

Moreover, it is more of a pure-play on the increasing popularity in

one-day lenses, because it doesn't sell lens-care solutions.

On the other hand, two losers from this report could be medical device company Covidien(NYSE: COV) and radiation oncology specialist Varian Medical Systems(NYSE: VAR).

Covidien has generated much of its growth in recent years from

surgical device appliances within its energy and endo-mechanical

divisions. Indeed, it’s a leader in the minimally invasive surgery

market. Covidien’s supporters (and I’m one of them) will always point

out that its solutions are relatively low-ticket, and they demonstrate a

tangible way for hospitals to reduce costs via achieving better patient

outcomes.

On the other hand, Covidien is still exposed to the volume of

surgical procedures in medical centers, and in its conference call,

Johnson & Johnson outlined that hospital and surgical procedures are

flat to negative.

Turning to Varian Medical Systems, this company definitely is a

high-ticket solution provider, and could suffer disproportionately if

there is a buyer’s strike in the hospital and medical center market.

There is a SWOT analysis of the company in an article linked here

which outlines its prospects for 2013. Johnson & Johnson talked of

the negative impact of macroeconomic conditions on its medical device

sales, and robotic surgery appliance manufacturer Intuitive Surgical (another high-ticket solution provider) has already disappointed in this earnings season.

Moreover, in its conference call, Johnson & Johnson described the

hospital capital expenditures market as being in recession for 10 to 12

consecutive quarters. All of these events are signs that Varian may

find its customers more reluctant to spend in 2013.

The bottom line

Johnson & Johnson has pretty much priced in most of the good

news, and it’s hard to see how the stock can appreciate much from here.

The stock has had a great run, but now it’s time to wait for a pullback.

One of the great IT bellwethers, IBM (NYSE: IBM),

issued mixed results in mid-July. It’s hard to be too critical of a

company that has just raised estimates despite increased currency

headwinds, but a deeper analysis of the company's results reveals some

underlying weakness. It’s been a difficult year for technology, and IBM’s earnings did little to raise investors' spirits.

IBM reports

The two key positives in the report came from the growth in

services backlog (7% at constant currency) and the strength in

higher-margin software sales. In order to demonstrate their impact, here

is a chart of IBM’s segmental growth. All data is sourced from company

accounts.

Growth in the second quarter was better than in the first. Moreover,

IBM’s reported revenue decline of 3% was made to look worse due to

currency headwinds of 2%. Based on its backlog, IBM forecasted that

third-quarter revenues in its global business services segment would be

up by mid-single digits, with global technology services increasing in

the low single digits.

The software segment's bounce back toward growth looked robust, and

management pointed out that its 4% reported revenue increase (5% in

constant currency) was the strongest recorded since the first quarter of

2012. IBM spoke of a very good software pipeline, and referenced good

growth in some important niches like branded middleware (up 10%) and

business analytics (11%).

To put this data into context, here is a graph (sourced from company

accounts) of the segmental revenue share and normalized pre-tax income

share.

Clearly, software is its highest-margin business, and its relative

strength in the quarter helped IBM raise gross margins to 49.7% from

48.3% last year.

With the services backlog up 7%, and higher-margin software returning

to growth in Q2, why aren’t these results as hot as they look?

Four reasons it's still tough out there

First, although software returned to growth in Q2, this was partly due to the weakness in the previous quarter. In fact, growth in the first half

was only 1.9%, which compares unfavorably to 2.6% and 11.5% in the two

previous years. Indeed, a glance at the first chart above demonstrates

that IBM is starting to lap some weaker quarters in 2012.

Second, going back to what IBM said last time around,

$400 million in software and mainframe deals were rolling in to Q2

anyway. When asked about these deals on the current conference call,

management stated that less than half closed in Q2, and, more

importantly, rollovers in higher-margin software are actually larger

going into the Q3. This all sounds good, but there is no guarantee that

rollover deals will get closed. In addition, its main rival Oracle(NYSE: ORCL) also reported some weakness in the quarter.

The third reason is that IBM’s forecast for services

revenue growth in Q3 needs to be put into context. Penciling in growth

of 5% and 2% for business services and technology services,

respectively, would give a total services revenue figure for Q3 of

around $14.9 billion. This compares favorably with the $14.4 billion

recorded last year, but rather less so against the $15.3 billion in

2011.

Finally, the macro commentary wasn’t great. America’s revenues

disappointingly declined 3%. However, the real surprise was within its

growth markets. Revenues in Brazil, India, Russia, and China, were flat

(up 1% in constant currency). In common with Oracle, IBM cited specific

weakness in Russia and China, and it expressed a cautious outlook for

its growth markets for the second half.

Key takeaways for the industry

While the tech market remains weak in 2013, there are pockets of

strength. IBM stated that its cloud revenues were up 70%; Oracle also

reported cloud-based strength. This shows a clear shift in corporate IT

spending towards the cloud and away from legacy on-license/on-premise

software.

Furthermore, the relative strength in IBM's middleware and business

analytics numbers suggests that middleware and data analytics company TIBCO Software(NASDAQ: TIBX) and interactions management provider NICE Systems(NASDAQ: NICE) could do well.

TIBCO finally seems to be sorting out its problems with its sales

force in North America. In addition, its increased focus on big data

analytics solutions, and offering its customers its service both

on-premise and via the cloud, is in line with trends in IT spending. Corporations

may be holding back on discretionary IT spending in general, but they

are still keen to invest in niche areas like social media and customer

engagement. Indeed, TIBCO cited specific strength in sectors such as

financial services and retail.

As for NICE, it has a deal with IBM to

integrate the latter’s analytics within its services. Unlike many areas

of tech spending this year, NICE has been reporting earnings that are

in line with expectations. Moreover, it is seeing strength within sales

of its advanced applications, which allow customers to analyze the data

that its systems capture. Again, this is a sign that in a slow global

economy, corporations are willing to spend on analyzing customer

interactions in order to better manage how they sell into their existing

customers.

The bottom line

In conclusion, IBM and Oracle have both reported earnings, and

neither had particularly good news for the IT spending environment.

Conditions appear to be stabilizing, but the broad-based bounceback in

demand hasn’t really happened yet.

With regards to IBM itself, the company’s story is about its ongoing

paring of lower-margin businesses, and how well it manages its shift

toward more software sales. For longer-term investors, I think the stock

will do fine. If it hits the raised adjusted diluted guidance of $16.90

in EPS for 2013, then it will trade on a forward earnings multiple of

11.4 times, as I write. This is attractive enough, but investors need to

be prepared for potential near-term volatility, because tech spending

remains weak.

It’s been a frustrating year for Yum! Brands’ (NYSE: YUM)

investors, as the fast-food giant has faced some significant challenges

in China. The country is at the forefront of Yum!'s efforts to shift

toward becoming the emerging-market fast food company du jour. Will the

company's problems prove temporary, or are there underlying

macro-economic reasons for the weakness in the Chinese fast food

sector?

Finger-licking buying opportunity?

The investment thesis behind buying Yum! is that its difficulties in

China will be swiftly resolved, and the company’s sales and margins will

come back strongly in the second half of the year. If you buy this argument then you must look into the causes of its problems.

Yum!'s issues in China started with a scare over the

quality of its chicken supply, and then moved on to consumers being

reluctant to eat poultry due to an outbreak of avian flu. The positive

case sees these problems as being short term in nature, and the current

valuation as being attractive relative to its long term prospects.

Superficially, the above suggests the stock is currently expensive.

In addition, if you assume it hits its estimate of “mid-single-digit

percentage decline” for 2013, then the stock is priced at roughly 23

times forward earnings as I write.

However, Yum! forecasts its Chinese sales growth to

turn positive in the fourth quarter, with 2014 turning into a year of

stellar growth because comparables will be a lot easier. If Yum! hits

analysts’ estimates of $3.79 in EPS for 2014, then the stock would be

trading on a forward valuation of 18.8x earnings. This makes it look historically cheap, so should you pile in?

KFC disappoints in China

In its latest results, Yum! reported that its

same-store sales for KFC in China were down 20% for the second quarter

in a row. However, in its recent conference call, Yum!’s management

outlined – in no uncertain terms – that its EPS forecasts were dependent

on Chinese sales coming back swiftly for its KFC operations. It also

served up a few indicators as to why it feels confident:

KFC same-store sales in China

were down 13% in June, compared to 26% for the second quarter,

indicating that the worst may be over.

KFC made low-teens sequential improvements in same-store sales in China from April to May, and then May to June.

Yum!’s second major

restaurant chain, Pizza Hut, recorded 7% same-store sales growth in

China for the quarter, suggesting that KFC’s problems are

company-specific, not due to a weakening Chinese consumer market.

Overall emerging-market-same store sales grew 5% in the quarter

In order to demonstrate the importance of China to Yum!, here is a

chart comparing its quarterly operating profit and the percentage of

Yum!'s total operating profit that comes from the country:

Source: Yum! Brands financial statements.

In summary, all of these points suggest that Yum! can turn around

performance in its key profit center. But what is the rest of its

industry saying?

A twist in the tale

Unfortunately, Yum! isn’t alone in seeing weaker results in China. In fact, its biggest rival, McDonald’s (NYSE: MCD),

also started to see its same-store sales growth slowing at the end of

2011. The main difference appears to be that Yum!’s performance notably

deteriorated after the chicken supply scare had its effect. However, the

downtrend was already in place by then, and it should be noted that

McDonald’s Asia-Pacific Middle East Africa (APMEA) sales haven’t been

strong this year, either. All the data in the chart is sourced from

company accounts.

It’s all very well for Pizza Hut to be generating growth in China,

but KFC makes up more than 74% of Yum!’s restaurants in the country.

Moreover, Burger King(NYSE: BKW)

also reported some disappointing numbers in its first-quarter results

to the end of March. For example, its global comparable same store sales

growth fell 1.4%. In addition, its results in Asia-Pacific (APAC)

weren’t much better with a paltry 2.7% systemwide comparable sales

growth recorded in the region. Furthermore, Burger King argued that the

rise in APAC was due to positive performances in Korea and Australia,

thanks to a combination of value promotions and programs.

In summary, neither Burger King nor McDonald’s are reporting anything

particularly positive on the global sales environment, let alone for

the Far East.

The bottom line

Yum!’s peers are seeing difficult conditions in China, so this looks

like it is more than a company-specific issue. Yum! is a compelling

proposition, but cautious investors will want to take a pass. The

company probably will engineer a recovery in China, but it may not be of

the magnitude needed to take the stock materially higher.

Earnings season is in full flow now, and it’s the turn of banking heavyweights such as Wells Fargo(NYSE: WFC) and JPMorgan Chase(NYSE: JPM)

to give their numbers and commentary on the economy. As ever, investors

will focus on the housing market’s effect on banking stocks' prospects,

and what it means to the wider economy. Frankly, I think the housing

marketis the key to future

movements in their share prices. Moreover, as long as the banks are

saying good things about housing, investors can feel confident about the

U.S. economy.

Don’t get fooled by randomness

It’s important not to get caught up in the minute detail of looking

at the banks. In truth they are still cyclical businesses. The banks

make money when the economy is trading in the direction of the core

assets (mortgages, loans, etc) on their loan book.

Therefore, if you want to buy banking stocks, you will need to focus

on how the economy affects the quality of their loan books. If housing

and the economy are doing well, then their credit quality (loan

delinquencies, charge off rates) will get better, loan loss provisions

will reduce, and demand for loans will go up. Ultimately higher rates

should be a positive to their earnings in the long term. In turn, all of

these metrics affect the valuation of the company.

My point here is that it's the direction of the core assets, rather

than looking at a snapshot of their earnings right now, that counts in

terms of making a decision to buy the stocks.

The big question over the banks…

The key issue is how the banks might deal with a rising rate

environment. The markets have been keen to price in higher rates ever

since Ben Bernanke implied that the Federal Reserve would begin tapering

bond-market purchases. So where does this leave the banks? Will rising

rates choke off loan demand, or will the housing market continue to

recover despite them? Naturally, if the latter occurs, the banks will see increased loan demand and banking profitability.

The issue can be seen by looking at Wells Fargo’s net

income and its net interest margin (NIM). Interest income (roughly half

of income) is more important to follow than non-interest income, because

it is more variable.

The market has been fretting over this issue in 2013 as economic

growth (therefore loan demand growth) has been moderate, while interest

rates remain low (reduced interest rate income) and deposit growth has

grown strongly (consumers continuing to deleverage).

Meanwhile, financial services companies such as Capital One Financial(NYSE: COF)

have been experiencing run-off. This is where existing loans are paid

off and not replaced by new loans due to weak demand. Indeed, Capital

One expects run-off to be $12 billion in 2013 and a further $8.5 billion

in 2014.

Furthermore, JPMorgan’s CEO, Jamie Dimon, discussed the possibility

for a “dramatic reduction” in the bank’s mortgage profits if rising

rates slowed demand for home loans. The issue is highly relevant because

Wells Fargo and JPMorgan are the two biggest mortgage lenders in the

U.S. Moreover, as the housing market is a key determinant for the

‘wealth effect’, the banks can expect demand for other forms of credit

(auto loans, credit card, etc) to be indirectly tied to it.

The two reasons why the banks will do well

The first cause for optimism is that the increase in deposit growth

created by consumer de-leveraging is building a powerful asset base from

which the banks can lend. For example, here is how Wells Fargo’s

average core deposits have increased recently:

In addition, its tier 1 capital ratio (a common measure of a bank’s

capital adequacy) has been rising. This indicates an increased capacity

to lend.

The second reason is that the wealth effect from housing is real.

Here is a graph of data from the Federal Reserve that demonstrates how

U.S. households and nonprofit organizations have seen real restate

wealth and their net worth improve in recent years:

Furthermore, gains in employment and slow-but-steady economic growth

are creating a favorable environment for growth in loan demand. If these

conditions persist, then the banks should be able to deal with a rising

rate environment. Indeed, historically speaking, a rising rate

environment means that banks will make more money.

The bottom line

In conclusion, investors should stay positive on the financial

services sector as long as the underlying fundamentals are moving in a

favorable direction. The debate about the effects of rising rates on the

economy will go on and on. There will be tomes of spilled ink

discussing the NIM, run-off, Basel III and other esoteric concepts that

ordinary investors find hard to grasp.

However, Bernanke has made it clear that tapering the purchases of

bonds –therefore lowering interest rates– is contingent upon a stronger

economy. Either the Federal Reserve will try to lower rates in the

future (given a slowing economy), or the economy will get better

(implying more loan demand). In any case, the banks are being supported

in their activities and, unless the economy is heading towards another

recession, investors should look to hold some banking stocks in their

portfolio.

It’s always interesting to use earnings season as a way to formulate a

view on the economy. Unfortunately, anyone looking for some positive

news on the industrial sector would have been disappointed by the recent

results from industrial supply companies Fastenal(NASDAQ: FAST) and MSC Industrial Direct(NYSE: MSM). What did these companies say, and what does it all mean for the industrial sector?

Mixed growth in the industrial sector

In short, outside of areas like aerospace and aviation, the

industrial sector remains weak. Earlier in the week, aluminum supplier Alcoa(NYSE: AA) came out with a positive report that gave cause for optimism.

The company always gives good color on its industrial end markets,

and the fact that it failed to reduce guidance for China has to be taken

as a positive. The good news on China was somewhat surprising because

companies like FedEx, Pall, and Oracle have all come out and stated specific weakness in China. Nonetheless, we should take what Alcoa said at face value.

Similarly, Alcoa’s global aerospace, automotive, and industrial gas

turbine segments remain set for good growth in 2013, even if Europe is a

little weaker. Since Alcoa is saying good things, surely the industrial

supply companies would, too? They are always useful as a

bellwether because their sales cycle is relatively short. This means

that any change in conditions will immediately be seen in their sales

figures.

Fastenal adjusts its strategy

Unfortunately, Fastenal and MSC Industrial both had negative outlooks on the industrial sector.

Fastenal spoke of a slow economic condition causing its

fastener sales (a cyclical product) to remain weak. In a sense, this

apes the overlying Institute for Supply Management (ISM) manufacturing

numbers, which have been softer in 2013. The ISM surveys private

manufacturing companies in order to produce its Purchasing Managers

Index (PMI), which is the leading manufacturing indicator in the U.S.

Note how the strength in new orders (which usually precede a pick-up

in the headline PMI numbers) quickly dissipated in February, while the

headline PMI number has averaged 49.7 this year. A number below 50

indicates negative growth.

In fairness, Fastenal did point out in the previous conference call

that its sales were not represented by the stronger ISM data in the

first quarter (ISM new orders had averaged 54.2 in the first three

months). However, this historical relationship came back into line in

the second quarter as both the ISM and Fastenal’s sales growth was

weaker.

The company’s response is to try to drive sales by making significant

new hires (mainly sales support staff) in its stores. The idea is to

hire 600-900 new in-store staff by the end of the year. The plan would

enable its existing managers to have more free time to visit more

customers, increasing sales accordingly.

It’s an interesting approach, because previously Fastenal’s main

focus was on expanding the installations and sales of its vending

machines. However, with competitors like MSC Industrial also building

out its vending machines and Amazon increasingly moving

in on the industrial supply market, Fastenal may feel that a balanced

approach to growth is a better way to deal with a slow industrial

market.

MSC Industrial also weak

The theme of adjusting to macro weakness was shared by MSC

Industrial. The company decided against implementing its mid-year

pricing increase in a concession to a softer demand environment. It’s

tough to get customers to accept price increases at the best of times,

let alone when end demand is weak. The good news for MSC Industrial is

that it has non-cyclical ways to increase profitability:

The acquisition of Barnes Distribution North America will increase revenues, margins and create opportunities.

Its e-commerce revenues are growing at north of 40%.

It has the potential to increase vending machine installations.

Obviously, these three aims are easier to achieve given a stronger

demand environment, and if you buy the "second-half industrial recovery"

story, then MSC and Fastenal are interesting propositions. On the other

hand, until the headline ISM manufacturing indices improve, investors

should brace themselves for more disappointments and negative sentiment

around the sector.

In comparing the two companies, MSC Industrial comes out on top in

terms of valuation and potential to grow earnings despite the economic

cycle.

In conclusion, these results told similar story to the first

quarter's about MSC and Fastenal and their end markets. It appears that

Alcoa’s optimism is more related to the strength of some of its

particular industry segments, such as aerospace and automotive.

Investors in Fastenal and MSC would do well to ignore Alcoa and focus

more on the ISM numbers in order to see where prospects for the two

companies are headed.

Alternatively, there is a strong case for simply staying invested

within the areas of strength in the industrial sector. It’s too early to

proclaim a general second half pick-up.

Investors can be forgiven for thinking that all is well with the outlook for the dollar stores after Family Dollar(NYSE: FDO) rose sharply in post-earnings trading. However, in reality, there were some warning signs for the economy in the report. Moreover, the underlying story in these earnings is of how well the company is adjusting to weak market conditions. Dollar General(NYSE: DG) and Dollar Tree(NASDAQ: DLTR) were marked up in sympathy, but it would be a mistake to assume that they will report in a similar manner to Family Dollar.

More margin pressure

In common with Dollar General, Family Dollar is seeing margin

pressure as its sales mix shifts towards lower-margin consumables and

away from higher-margin discretionary items. In fact, the share of

consumables rose to 72.5% of total sales, compared to 68.9% last year.

In contrast, Dollar Tree managed to benefit from margin expansion by

growing its sales mix in the other direction. However, this appears to

be an isolated case amongst the mass market retailers.

Family Dollar actually highlighted industry data that suggested that

its typical consumer was spending less in the marketplace, but more

at its stores. This is not a great sign for the economy. This data also

implies that if there is growth to be generated, it will come at the

expense of its competition. Family Dollar is likely taking share from

the supermarkets within the

grocery category. Unfortunately, consumables like tobacco and groceries

are not really high-margin items. So even as Family Dollar expands

sales in these areas, it will not see gross margin expansion.

These trends are nicely illustrated with a look at the company’s

sales and margin trends over the last few years. Note the company’s

forecast for the next quarter is for an anemic-looking 2% same store

sales growth. This is a bit disappointing, because even though the first

quarter was weak for most retailers due to a number of issues (payroll

tax increases, tough weather comps, tax refund delays and the

sequester), the second quarter was supposed to be a more favorable

environment.

On the other hand, the positive news is that gross margins were

forecast to be almost flat in the next quarter, much to the liking of

the markets.

Why the market likes these results

The real takeaway of these results is how Family Dollar is adjusting

to a slower sales environment. Gross margins were predicted to be almost

flat in the fourth quarter, and in the conference call, the management

discussed the possibility for them to be flat in 2014 as well. There are

a number of reasons for a more positive outlook for both gross and

operating margins:

The company has adjusted to

the slower sales environment and is now highly focused on reducing

things like freight, distribution center, and advertising costs.

It is starting to lap the unfavorable mix shift movements from last year, so comparisons will get easier.

Management spoke of some recent improvements in its core discretionary businesses and spoke of the beginnings of stabilization.

The last point is the key, because Dollar Tree has already managed to

do this in 2013, while Dollar General was punished by the market in

early June when it lowered guidance thanks to weakness in its

discretionary sales. In addition, Family Dollar is

somewhat playing catch-up because its discretionary merchandising

decisions were below par in 2012. In short, Family Dollar tried to

increase sales with discretionary items like clothing, but found it a

tough sell to its customers.

Why you shouldn’t get too excited

In putting these points together, it’s hard not to be puzzled as to

why the market dragged the other two dollar stores up in sympathy. Family

Dollar didn’t have many good things to say about the economy. In

addition, if it really is winning market share, then the other dollar

stores could be missing out.

Also, the dollar stores have tended to report similar

trends in same store sales (as shown in the graph below), but they have

tended to differ in how they deal with sales mix issues and getting

their discretionary sales right.

In conclusion, if these results were all about Family Dollar

adjusting to a slower sales environment, then there isn’t a strong

reason to think that Dollar Tree and Dollar General are about to shoot

the lights out in their next reports. Don’t get too excited.

It’s always interesting to look at Paychex's(NASDAQ: PAYX)

results, because the small business service provider usually gives good

color on the economy. What do its latest results say about the small

business environment, Paychex's own prospects, and can the company grow

its relatively large dividend?

Paychex gives mixed commentary

Anyone hoping that Paychex would deliver an upbeat depiction of

the economy would have been disappointed with the recent fourth-quarter

results. The key metric to follow, in terms of analyzing the health of

the small business sector, is its 'checks per payroll’. Unfortunately,

it only rose 0.9% in the quarter, and analysts spent much of the

conference call trying to find out why it was so weak. The commentary

wasn’t good, with the management describing it as moderating in the

quarter and then suggesting that the trend was downward.

In addition, this doesn’t even appear to be a Paychex-specific

issue because its client retention was at an all-time high at above 81%.

The payroll services market is competitive, with the likes of Automatic Data Processing(NASDAQ: ADP) and Intuit(NASDAQ: INTU)

also active, but Paychex is holding its own for now. Indeed, it made

bullish noises by predicting its client growth would come in at 1%-3%

going forward.

Paychex seems to be competing quite well, and it's helped by

strength in the housing sector. I note that in May, ADP kept its

forecast for pays per control (within its employer services division) at

2%-3% growth. In light of what Paychex just said, will it have to

reduce this figure?

In summary I think Paychex’s commentary -- it also highlighted

weaker-than-expected new business formulation -- confirms the mild

nature of the recovery, and you can see this in the National Federation of Independent Business (NFIB) data. I’ve broken out the current job openings data below.

The trend is favorable, but growth remains tepid, and Paychex’s results did little to assuage fears.

Paychex’s recent results

Paychex’s overall results were okay. In the last quarter, it

had forecast full year growth of 1%-2% in payroll services, with human

resource services forecast to grow at 9%-11% and net income up 5%-7%. In

the end, these full year numbers came in at 2%, 10% and 6%

respectively.

In its guidance for 2014, the company predicts:

Payroll services revenue growth of 3%-4%

Human resource services growth of 9%-10%

Total service revenue growth of 5%-6%

Net income growth of 8%-9%

The forecast for the acceleration in payroll service growth is

based on revenue per check rising for Paychex. This is thanks to price

increases made to customers, rather than an improvement in the amount of

checks per payroll. At this point, anyone would be inclined to ask

whether it is worth paying 24 times current earnings for a business that

is forecast to grow income by only 8%-9%.

One reason to make your answer "yes" is if you see some upside

prospects to these forecasts. Paychex obviously has the potential to

benefit if the economy does better. Furthermore, its management was keen

to highlight the potential for its healthcare services to do well as

companies grapple with regulatory changes. However, I think its most

interesting upside driver could come from its technological investments.

Technology to the rescue?

In common with others in its industry, Paychex is making ongoing

investments in software as a service (SaaS) offerings. The idea is to

create an integrated management tool that allows its customers to use

its human resource, employee management, and payroll services through

one application. In fact, it’s such a good idea that ADP and Intuit have

already been doing similarly.

I’ve discussed Intuit in more detail in an article linked here.

Its recent results were disappointing, but that was mainly due to its

core tax return business having a poor season. In fact, its small

business group (which now makes up 35% of revenues) saw growth come in

at 17% in the quarter. Its employment management services came in with

11% growth. Intuit is the poster boy for businesses shifting their

offerings towards SaaS, and clearly, Paychex needs to embrace these

industry changes.

With regards to Intuit, it will be a while before tax return

season comes into investors' minds again. Provided it can keep up good

growth in its small business group, I think Intuit's stock is well worth

looking at.

ADP claims to be the "leading provider in the cloud"

and is pushing its ADP Vantage HCM product. This product will integrate

things like ADP’s human resource management, payroll services, and

benefits administration. ADP described the products sales as "tracking

very well against our expectations" in its latest conference call.

Unfortunately Vantage is still a relatively small part of its sales, so

investors can't expect too much of a contribution in the near term. ADP

expects its employer services to grow at 7% this year, but is seeing its

growth prospects held back due to its European exposure and ongoing low

interest rates holding back investment income.

The bottom line

I think the main attraction of Paychex remains its dividend

yield which currently stands at around 3.5%. By my calculations, it paid

out nearly 83% of its free cash flow in dividends last year. Therefore,

there isn’t much scope to aggressively grow dividends outside of bottom

line growth, and, with income forecast to grow at 8%-9%, you shouldn’t

expect too much of a dividend increase in future.

In conclusion, Paychex's commentary on the economy wasn’t

great, but it is performing well in very competitive markets and has

some upside drivers. On the other hand, there are others increasing

investments in its core area of payroll services. On balance, it’s not a

stock for me, because I don't chase dividends. But those looking for

yield could do a lot worse than picking some up.

Investors always like to look at Alcoa’s (NYSE: AA)

earnings and use them as a guide to the rest of earnings season. In the

latest second-quarter results, there were some surprising elements

which deserve to be looked at in more detail. In this article, I want to

examine Alcoa’s end market commentary and discuss the implications for

some companies which you might be looking at.

Alcoa changes guidance, but not for China

I’ve tabulated the updated full-year guidance below. The green

segments are where numbers were upgraded, and red is for the downgrades.

Probably the most surprising aspect of these results was that Alcoa

didn’t reduce guidance in any of its end markets within China. A number of companies have reported recently and cited specific weakness in the country. For example, FedEx recently spoke of global trade growing slower than global growth, Oracle cited weakness in China, and filtration company Pall (NYSE: PLL) delivered some disappointing numbers in its industrial filtration results.

Pall’s Chinese industrial sales were down 11% in the quarter. The

company spoke of the ongoing changes in the Chinese economy and how they

are forcing Pall to adjust its sales focus. In general, China is trying

to shift towards more domestic consumption and reduce its dependency on

export-led manufacturing. This is presenting challenges

to Pall, and given that nearly 60% of its industrial sales are in

process technologies and 20% in microelectronics, it is likely to face

some difficulties.

Aside from what companies are saying, China’s own economic data has

been weaker recently, with the official Purchasing Managers’ Index

registering 50.1 in June. A reading above 50 indicates growth, so

clearly China’s manufacturing industry is not growing by much. However,

this is not the way that Alcoa sees it! Indeed, it actually cited

Chinese demand for aluminum as remaining strong and kept its 11% demand

growth forecast.

The reason why Alcoa may be seeing relatively better conditions is

because aerospace and automotives have been the standout performers

within the industrial sector this year. Furthermore, beverage can

packaging is relatively non-cyclical, and China’s heavy truck &

trailer industry is benefiting this year from some regulatory changes.

It looks like a case of good news for Alcoa, but not necessarily for the

wider economy.

Winners and losers from Alcoa’s report

Aerospace and automotive have been strong this year for similar

reasons. The U.S. consumer is starting to benefit from employment

increases, and lenders are more willing to expand credit in the form of

car loans. North American auto sales have been improving, while China’s

remain strong.

Aerospace has been very solid, and the industry has the

potential to outperform in a cyclical recovery because its dynamics

have changed. The need for austerity has forced

governments to stop subsidizing national loss-making champions, and

airlines are getting much better at dealing with high oil prices and

outsourcing unnecessary work. The result is increased airline

profitability driven by Asian passenger traffic.

This commentary will interest shareholders in a diversified industrial company like General Electric(NYSE: GE) or Ametek (NYSE: AME). Aviation is GE’s largest industrial profit generator,

and it needs strength in aviation, transportation, and health care in

order to offset some weaker performance in Europe (particularly within

its power & water segment). Alcoa spoke of a 40% rebound in growth

in its regional jet business and 12% for its business jet segment. This

is great news for GE, but, on a more worrying front, Alcoa also said

that it anticipated a weaker demand from Europe for industrial gas

turbines. It looks like GE’s weakness in power & water is set to

continue, so this is a mixed report for GE.

However, it was a good report for Ametek shareholders. The company has heavy exposure to aerospace, particularly the business jet sector (Textron is

a major customer). Ametek also has customers in the North American

heavy truck & trailer market. Indeed, in its most recent results,

Ametek had cited some softness in its power & industrial business,

thanks to softness in the heavy truck market. My point here is that if

Alcoa is talking about order rates being up, then this will surely feed

through into Ametek in future quarters.

Other stocks worth considering for the aerospace theme are B/E Aerospace, Heico, and Precision Castparts. Finally, the heavy truck & trailer market seems stronger, so stocks like Cummins could see better prospects.

The bottom line

In conclusion, this was a pretty good report from an

end-market-demand perspective. There were no downgrades to expectations

over China, and if anything, the news on the aerospace and automotive

sectors was a little better. There was even some positive news for the

heavy truck & trailer market. Overall, it was a favorable report,

but investors still need to remain selective about where they invest in

the industrial sector, because the sub-sectors within it are reporting

some varied performance.

ConAgra Foods(NYSE: CAG)

stands out as a winner in the food industry over the last few years.

Its mix of value brands in the consumer division, expanding private

label business and, a commercial foods division (which has been

expanding profits strongly over the last few years) has stood it in good

stead to deal with a challenging environment.

In summary, I think the company is well-positioned to do well, but a

lot of its prospects depend on believing the management can execute

successfully.

How ConAgra makes its money

I’ve broken out the recent fourth-quarter numbers, because

private-label manufacturer Ralcorp hasn’t been part of ConAgra for a

full year yet.

In order to properly reflect its performance ConAgra will change the

way it reports by splitting the commercial foods division into a

private-label segment (to reflect the addition of Ralcorp to its

existing private-label business) and, a food service segment which will

contain its Lamb Weston potato operations.

The three things its management needs to execute

The first question is it can continue to generate volume growth in

its consumer foods division. ConAgra increased prices last year; in

common with so many other companies in this slow economy, it then saw

volume decreases. Consequently, it’s taken a while for ConAgra to get

back to organic volume growth. Indeed, it only did so in the recent

fourth-quarter results with a 3% gain. Overall, consumer foods sales

were up 7%, with acquisitions contributing 5%.

ConAgra sees the organic sales growth as a turning point, but it has

come at the expense of increasing advertising and promotion expenditure

by 15%. Margins were up slightly thanks to strong cost savings which may

not be repeated this year. This is fine but,note that the company has

had to increase marketing costs in order to get volume growth. It is

also spending more on supporting the launch of some new products in

areas like desserts and frozen breakfasts. It is not a given that the

new products will work and/or that operating margins won’t suffer next

year thanks to increased marketing spending.

The second question relates to the Ralcorp acquisition. The good news

was that It raised its synergy projections to $300 million by 2017, as

opposed to the initial target of $225 million. Moreover Ralcorp’s

profits were in line with expectations, but its sales performance was

softer than ConAgra expects to see in the future. The subsequent

restructuring activity was described as short term and fixable in the

conference call.This is fine, but it still needs to be done.

Looking at the wider question of private label manufacturing I would issue caution. As investors in TreeHouse Foods(NYSE: THS)

will tell you, manufacturing private-label foods can be a volatile

business. Industry trends may be favorable right now, but Treehouse has

had to deal with difficult conditions in recent years. Its customers'

sales channels have changed along with the trend towards trading down.

Private-label companies are subject to the sales patterns of their

customers, and while Treehouse is currently doing well with things like

single-serve coffee and refrigerated dressings, it has also suffered

before with categories like soup and pickles. It’s a business that

requires a constant adjustment to the end market conditions of

customers. Don’t be surprised if Ralcorp faces similar issues in future.

Treehouse is on a forward PE of over 20 and is hardly cheap for such an

uncertain business.

The third issue is that its commercial foods segment saw its potato

operations (Lamb Weston) lose a major long-term customer. This will

reduce EPS by $0.10 next year.The contract loss will also hit margins,

but ConAgra expressed confidence that it would make up for it. Again,

the management needs to deliver.

In addition, ConAgra talked of "short term challenges in Asia," which

caused profits to decline for its potato operations for the quarter.

Frankly, I don’t believe in coincidences, and anyone looking at McCormick’s (NYSE: MKC)

latest results would note that it reported weakness from its quick

service restaurant customers in both China and the Americas. Yum! Brands

is a major customer of McCormick and much of its problems are company

specific but the truth is that it’s Chinese same store sales growth has

been falling since the first quarter of 2012.

In addition McCormick’s industrial growth has been negative for the

last two quarters. Is this a short term issue or is it a deeper one

relating to slowing quick-service restaurant sales growth? These types

of restaurants are major customers of ConAgra's potato operations.

The bottom line

In conclusion, I think these three concerns require you to

express a fair amount of confidence in the management to execute over

the next year. This might be okay if the stock traded on a more

attractive valuation. A forward PE of around 13 may look attractive, but

recall that the company has to pay off significant amounts of debt.

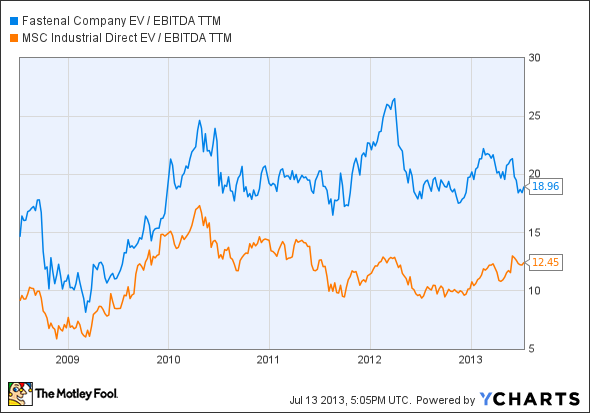

Looking at these companies' current enterprise values (EV) in

relation to their earnings before interest, depreciation and

amortization (EBITDA) reveals that none of them are cheap. The measure

helps to account for debt levels in evaluating a stock.

ConAgra is the most expensive of the three companies above, and it's

not cheap enough to compensate for the execution risk. It's a stock for

the monitor list. The market may be in love with food stocks, but there

is no excuse for not sticking to your valuation principles.

There is a lot to like about the long-term prospects for spice and seasoning company McCormick(NYSE: MKC)Consumers

are demanding ever more flavor in their cooking, and food companies are

being forced to innovate by using flavorings in order to compete in

difficult end markets. With these positive trends in place, the company

is doing well. But what of its near-term prospects? Moreover, is the

stock good value right now?

McCormick delivers mixed results

It was an underwhelming set of second-quarter (Q2) results for

McCormick, as reported sales rose a paltry 2%. Its top line growth has

been slowing in recent quarters as it laps some difficult comparables.

In addition, Yum! Brands(NYSE: YUM), is one of its major clients and it's having some well documented difficulties in China

with its KFC stores. First it was a scare over its chicken suppliers,

and now it has to deal with fears over bird flu. The issue is hurting

Yum!, and McCormick's industrial sales are being hit because it supplies

spices and seasonings to KFC.

I’ve broken out the progression of McCormick's divisional sales growth below.

The problems in the industrial division aren’t just about

quick-service restaurants in China, because McCormick's industrial sales

in the Americas declined 1%. McCormick cited strength in its snack

seasonings and food flavorings, but it wasn’t enough to offset declines

in demand from quick service restaurants in the Americas. The eating out

category has faced some weaker growth and, the areas that are growing

within it are not favoring McCormick.

All of which is not to be too negative on the stock because it’s the

consumer side that makes the majority of profits. And it is still doing

quite well.

A breakout of Q2 operating income here.

Consumer segment sales grew 5% in constant currency. Within developed

markets, McCormick is benefiting from a increased willingness among

consumers to eat at home and, to utilize more flavors in their cooking.

The latter trend is also being driven by an increasingly ethnically

diverse population in many developed countries.

Within emerging markets, McCormick is seeing good results via a mix

of organic and acquisition-led growth. For example, in India its

acquisition of spice company Kohinoor is giving McCormick long-term

opportunities in an important growth market. India makes up less that 5%

of sales, so there is plenty of scale for this figure to increase in

future years. Similarly, the WAPC acquisition in China is believed to

bring its Chinese sales up to 7% of the company total.

Two concerns

The first relates to the disappointing performance within China and

the Americas on the industrial side. The hope with Yum! is that it will

be able to recover from its company specific issues but I think there

might be some macro factors at play here too. Yum! Brands' same-store

sales in China were getting weaker even before the media scare stories

and bird flu worries hit.

It was a similar story with McDonald’s(NYSE: MCD).

The outlook for the quick service restaurant sector is important to

McCormick, since much of its industrial demand goes to this industry.

The signs are that it is not just a Yum! issue. McDonalds’s could be facing a tough year this year, and Yum! investors need to take note.

McDonald’s management was very clear on its last earnings call that

it intends to retain and even grow market share. This as a sign that it

will be willing to sacrifice margins and cash flow in order to secure

long term positioning. McDonald's and Yum! are likely to increase

competitive efforts in North America in order to try and make up

weakness elsewhere. McCormick investors will be hoping that Yum! wins

out.

The second concern is that even though the consumer division is doing

well, its growth is still slowing. The company announced it was

increasing incremental marketing on its consumer brands to $15 million

but, it did not raise revenue expectations. The weakness on the

industrial side is increasing the pressure on the consumer side.Is this

marketing increase a sign that it is having to work harder to hit its

numbers?

The bottom line

I don’t want to appear too negative here, because this company has

plenty of good long-term drivers, and its acquisition strategy makes

perfect sense. However, if you are going to add this stock to your

portfolio, you will need to assess it on a risk/reward basis. This is a

stock that trades at 22 times its November 2013 earnings, which looks

pricey when compared to International Flavors & Fragrances' forward PE of nearly 18, and German rival Symrise at 20 estimated 2013 earnings.

McCormick is hardly cheap, and its underlying growth is slowing while

its end-market customers (on the industrial side) are facing some

difficult market conditions. This stock is worth monitoring for a

long-term buy, but an entry point might only come should it miss

estimates this year.

With the housing market seemingly at the start of a multi-year

recovery, the market has been keen to bid up any stock related to the

sector. Usually this is for good reason, because the earnings outlook is

improving for these companies. However, in the case of homeware

retailer Bed Bath & Beyond (NASDAQ: BBBY),

I think the market is giving it the benefit of the doubt over the

prospects for its restructuring, acquisition and expansion strategy. The

stock is already up 26% this year. How much further can it run without

definitive evidence of success?

A special situations play

Going into this year, BB&B was challenged to adequately integrate

its World Markets and Linen Holdings acquisitions, restore same-store

sales growth and margins, and successfully continue is store expansion

plans.

It needs to do these things because It has been suffering from margin

contraction as its sales mix has been shifting towards lower margin

item sales. Meanwhile, its acquisitions have increased selling, general,

and administration (SG&A) costs.

Here's a graphical representation of how its margins have moved in the last few years:

Source: Company financial statements.

Readers will note that there wasn’t much improvement in the recent quarter.

Latest scorecard from the Q1 results

The bad news in the quarter was that the acquisitions continued to

increase SG&A costs by 100 basis points, while gross margins

declined thanks to increases in couponing and redemptions. Meanwhile,

sales have continued to drift toward lower-margin categories.

The good news was that same-store sales increased by a healthier

3.4%. This was put down to an increase in transactions and transaction

amounts. While this is a good sign – and Q1 was a difficult retail

environment -- I can’t help but remark that it should be able to sell

more items if it is offering more coupons.Unfortunately,

the drive to increase sales is coming at the expense of

margins. Furthermore, its guidance of 2%-4% same-store-sales growth for

Q2 and the full year was nothing to write home about.

So the acquisition integration appears to be holding back margins,

but the company hasn't slowed down its expansion plans. In fact, store

space (including acquisitions) increased by 16% for the year, and

capital expenditures for 2013 are forecast to increase to $350 million

in 2013 from $315 million last year.

The company plans the number of new stores opened in 2013 to be in

the "mid thirties," although the management gave notice that it would

update investors in the final figure as the year progresses. And

finally, a significant amount of investment is being made to upgrade

Bed Bath & Beyond's websites and e-commerce facilities in order to

drive multichannel sales. Will it all work?

The benefit of the doubt?

Are investors being too keen to cut the company slack over its performance and prospects? It’s not hard to see why they would, because so much has being going right for this subsector of retail in 2013.

On the other hand, each company must be judged on its own merits. For example companies like Williams-Sonoma(NYSE: WSM) and Pier 1 Imports (NYSE: PIR)

have done very well by increasing their multichannel sales efforts. But

they are way ahead of where Bed Bath & Beyond is right now.

Williams-Sonoma is trying to increase its Direct to Consumer (Dtc)

revenues (things like catalogue and online sales) because they tend to

fetch higher margins than selling through retail and wholesale channels.

Indeed, its DtC-based revenues rose to 22.9% of total revenues from

20.8% last year. This helped its operating margins rise by 60 basis

points in the last quarter. Similarly, Williams-Sonoma is engaging in a

program of opening new stores and expanding existing ones -- albeit

mostly abroad. It's also increasing capital expenditure plans this year

to $200 million-$220 million, this year, compared to $205 million last

year.

The difference is that Williams-Sonoma is firing on all cylinders.

It is expanding margins and demonstrating success with its expansion

plans, and it generated 7.2% overall growth in its comparable brand

revenue. This is a far cry from Bed Bath & Beyond’s 3.4% same-store sales growth.

As for Pier 1 Imports, it recently reported comparable store sales

growth of 5.9% and has just reached the anniversary of its e-commerce

enabled site. It has seen its e-commerce contributions to total revenue

make ‘progressive increases’ since their launch (even though investors

will have to wait until Q1 2015 for a breakout of its comparable-sales

calculation for DtC sales), and it is investing heavily in that effort

as an integral part of its plans.

Pier 1’s strategy is to arrange for in-store pick up capability

(customers seem to use this extensively), and it's rolling out an in

store point of sales system (90% of its stores are already operating

it). Pier 1 grew its overall sales by 9.3% in the quarter. Again, this

company is executing very well within a favorable end market.

Furthermore, note that Pier 1 is well ahead of Bed, Bath & Beyond

with its online plans.

Where next for Bed Bath & Beyond?

Of course, what BB&B does have going for it is its valuation. On

these grounds it compares quite favorably with the two other companies

mentioned in this article.

Moreover, if it hits analyst estimates for $5.02 in EPS it will trade on a forward PE ratio of around 14.4 as I write.

Ultimately, an investment decision here is going to depend on your

level of belief in the successful execution of the plans outlined above

and an ongoing belief in the housing market recovery. The company will

see better end market conditions thanks to an improving market, but I

don't think that is enough of a reason to buy the stock.

Moreover, If the the housing market stalls, then this stock’s

prospects will be called into question. There are always risks with

expansion plans, not least from a company that has been seeing margins

falling and lackluster same-store sales growth. Sentiment will likely

take the stock higher, but I think the company needs to demonstrate

better underlying performance before justifying buying in at this level.

North America's leading lighting company, Acuity

Brands (NYSE: AYI), delivered another

good set of results for its recent third quarter, and spoke about its markets

picking up.The stock offers a ‘back door’ way to play the increasing usage of

LEDs in lighting solutions.If you like the construction industry and

energy-efficient lighting, then Acuity could be a stock for you. Its prospects

look positive, but is that enough to justify its lofty valuation?

Acuity Brands' secular growth drivers

The decreasing cost (per lumen) of LEDs means that Acuity can generate growth

from LED lighting replacing conventional lighting. Margins on LED lighting are

similar to conventional bulbs, but Acuity argues that it sells controls with

virtually all its LED lights. Lighting controls are an essential part of the

value proposition because, they help to increase the efficiency of lighting

solutions.

The good news is that this is driving sales growth. Its net sales were up 11%

in the third quarter, as opposed to the ‘low single digit growth rates’ that it

claims its markets are growing at. The ‘bad’ news is that volumes grew by 14%.

The discrepancy is due to lower prices of LED components and an unfavorable

product mix. Essentially, Acuity is providing relatively more solutions to lower

margin renovation work because large scale new construction hasn’t kicked in yet

thanks to the slow economy.

Acuity's LED-based revenue is now at 20% of its total, from 15% and 13% in

the previous two quarters. This is a powerful trend.

For example, a company like Cree(NASDAQ: CREE) is more of a pure

LED play than Acuity. It offers a vertically integrated way to play growth in

LEDs. Lighting looks set to be the primary driver of the next upswing in the LED

cycle. Cree’s own lighting division managed to increase sales by 6% in the last

quarter, even with unseasonal weather negatively affecting outdoor lighting

sales.

Cree’s lighting products gross margins are at 30.6%, while Acuity’s numbers

are at a more impressive 40.8%. Acuity has a more mature sales operation, while

Cree uses sales agents. Nevertheless, Cree appears to have the opportunity to

improve its lighting products margins going forward. Cree’s lighting product

revenues currently represent nearly 38% of its total, so the opportunity is

significant.

Cyclical growth drivers

Acuity can see cyclical growth in two ways. The first is from a general

pickup in construction activity, and the second is through margin expansion, as

more profitable activity like large-scale new construction takes place.

Historically speaking, the former usually entails the latter.

In addition, investors need to appreciate that lighting is one of last phases

of construction, so a natural time lag exists between general activity and

orders coming in for lighting.

All eyes will be fixed on construction indicators such as the

Architectural Billings Index (ABI) from the American Institute of

Architects. It has been unusually volatile lately.

One explanation for this is the late spring this year, plus delays over

worries with issues like the sequester and payroll taxes.

Moreover there are some peculiar recent dynamics which can be seen in the ABI

data.

The recent weakness in the commercial/industrial (C & I) sector is

concerning because it’s Acuity’s strongest end market. The hope is that new

residential construction will feed into new C & I construction as

infrastructure is built up around the new housing.Unfortunately, it hasn't happened yet.

Other companies have talked of weakness. Regal Beloit(NYSE: RBC) revealed a shocker

of an earnings announcement at the end of April. The company makes the kinds of

motors used in heating, ventilation and air conditioning systems.

Regal lost a major contract when a customer decided to source components from

a third party (rather than buy from Regal Beloit and manufacture themselves)

and, overall its commentary on its C & I markets was poor. Guidance was

lowered and, the strength that it had seen in January fell away through the

quarter. The ABI data has weakened since then so it's anybody’s guess what it

will say in its next set of results. On the other hand, it's cheap on a cash

flow basis and, this could be a decent entry point.

The bottom line

In conclusion, you need to believe in both these drivers to want to buy

Acuity at this level. While secular growth looks assured, it is far from clear

that the cyclical growth is. On a trailing PE ratio of nearly 32, compared to

its smaller rival Hubbell at 20, the stock is not cheap. I share some of the

optimism over this company, but a strong and sustained recovery in the C & I

market is not a "done deal." That makes Acuity one for the monitor list.

It’s been a mixed earnings season for industrial-based stocks and

Ametek’s (NYSE: AME) last set of

results provided a pretty good microcosm of what has been going on. In short,

companies with heavy exposure to industries like automotive and aerospace have

done well, while almost everything else has found things difficult. So what

makes Ametek interesting and what can we read across for other companies?

Ametek generates growth across the cycle

The company is attractive for a few reasons. Firstly although it

is not a pure-play aerospace company, it has heavy exposure and as the industry

is looking set for good long-cycle growth, it has good prospects. Secondly,

Ametek has long been a company categorized by its management’s ability to make

earnings-enhancing acquisitions without damaging its return on invested capital

(ROIC).

As the chart indicates, Ametek has done a pretty good job of consistently

generating ROIC even when market conditions are not great. An acquisition-led

growth strategy does have its advantages and disadvantages. On the plus side,

the company can carry on generating growth by getting companies cheaper in the

downswing (and benefiting from the hopeful upswing in the economy); but on the

downside its management will be under pressure to make the right acquisitions.

And making the wrong decision can occur irrespective of where the economy is

positioned.

Recent results

The good news is that Ametek’s management has a strong track record in this

regard and acquisitions are a key part of the focus for 2013 as well. Even in

the latest Q1 results we saw organic sales decline 2% but acquisitions

contribute 9% and –even in a weaker environment for aerospace- its sales were up

7%.

As ever with this type of company, cost management and lean manufacturing

will be a strong focus. Indeed cost reductions were made in the quarter, without

which, EPS would have been up 18%. There was good news on the cost-cutting front

with estimates for total full-year savings rising to $95 million from $85

million previously. Operating cash flow rose 11% and full-year EPS guidance was

raised at the low end to imply 11% to 13% growth. Moreover the commentary on

linearity was positive with April cited as looking ‘good’. Like many in the

industrial sector it saw some weakness in March.

Industry background

As usual with earnings season, Alcoa (NYSE: AA)tends to set

the tone for the industrials. A brief look at the

conclusions from its earnings reveals that areas like aerospace and

automotive remain relatively positive. Europe remains weak on the whole and the

heavy truck and trailer market is experiencing a sharp slowdown. Moreover much

of Alcoa’s growth is predicated on stronger conditions in China. The surprising

thing was that Alcoa did not alter its full-year end-demand outlook by much even

though the consensus is that Q1 did get weaker overall for industrials.

Alcoa’s trends were confirmed by Ametek when it discussed some softness in

its power and industrial business created by the North American heavy truck

market, so no surprises there. Furthermore within its process business segment

the strongest performer was oil and gas while metals analysis revenue was

relatively weaker.

The key strength in the business was from aerospace. Its electronic

instruments group (EIG) saw aerospace (commercial, business and regional jets)

revenue rise by low double digits and growth is expected to remain solid for the

rest of the year inline with build-out rates at Boeing and

Airbus. Overall EIG sales were up 3%.

It was a similar story in the other segment. The electromechanical group

(EMG) saw its differentiated business sales up in the mid-teens with particular

strength cited in its aerospace maintenance, repair and overhaul (MRO)

operations. However, overall sales for EMG only rose 3% thanks to

a 14% contribution from acquisitions.

Which stocks read across well?

Frankly I think investors should try and stick to the themes that are working

well and try and find value in them. If aerospace and automotives are doing well

and companies like Alcoa and Ametek are confirming this, then why not stick to

the idea? Three names that I like are Heico (NYSE: HEI),

Precision Castparts (NYSE: PCP) and

PPG Industries (NYSE: PPG).

Heico recently reported strong results and the business clearly has good long

term prospects from helping airlines to try and reduce costs by outsourcing

flight support activities. Even though Heico argued that its success in the

quarter (its flight support group saw sales and income rise 10% and 14%,

respectively) was largely a consequence of internal execution rather than

industry growth, I think that there are enough positive signs within its

performance to suggest further growth this year.

Its space-related sales may well be variable and its defense

sales will be subject to sequestration effects so now may not be the best time

to buy into the stock. But if you can tolerate these fears, the stock is

attractive.

Precision Castparts is attractive because of its heavy

exposure to commercial aerospace (75% of its market) and its opportunities

to generate synergies from its acquisitions. In addition, it is ramping up

production in order to meet demand from Boeing on the 737 and 787.

My one concern with this company is the cyclicality of its cash flows. The

aerospace industry is cyclical but there is evidence to suggest that it is

likely to experience better conditions in this cycle. However companies like

Precision Castparts always need to make significant capital expenditures in

order to service demand.

This is great when demand is good but it leaves them exposed should demand

start to weaken. You can make the argument for making an evaluation based on

assessing its long-term earnings or cash flow performance but in reality I think

the market just trades these stocks based on momentum.

My favored play on this theme would be PPG Industries. The company has good

exposure to aerospace and automotive and its purchase of Akzo Nobel’s US

household paints operation is timely. Costs appear to be moderating and it has

some cost synergies coming from the acquisition. Margins are expanding thanks to

its restructuring efforts (such as selling some of its commodity-based

businesses) and its cash flow generation remains very strong.

Meanwhile the recent court order over the Pittsburgh Corning (a joint venture

with Corning) has somewhat de-risked the stock from uncertainty

over future asbestos claims. Earnings growth is being held back this year

thanks to some of the issues discussed above but, this is a business which has

generated an average $1.1 billion in free cash flow over the last three years

and trades on an EV/Ebitda multiple of 9.5x. Looks like good value to me.

Where next for Ametek?

This is an impressive company and a real ‘go to’ option for a pick in

the industrial sector. Unfortunately its trailing PE of around 22x plus its

EV/Ebitda multiple of 13.1x suggest it is largely pricing in the good news. It’s

well worth monitoring and hoping for a dip because $42 looks like a fair price

for the stock. Given any kind of market retraction it's worth a close look.

Nike (NYSE: NKE)

is one of those companies whose results will interest the whole of the

retail industry as well as its own shareholders. And given its recent

results there are many things to consider. It’s a story of strong

execution in North America and with footwear in particular. However, its

European markets remain weak and China is displaying the kind of

softness that others are seeing.

In summary, Nike's prospects are reliant upon continued success

within its North American operations and the belief that it will turn

around its performance in China. If either of these things fail then the

stock's evaluation will start to look a little stretched. The stock may

have some good near-term upside drivers, but I think it also has

downside risk and this article will explain why.

Nike triumphs in North America

In order to illustrate the importance of the performance of its

North American operations I’ve broken out its quarterly earnings before

interest and taxes (EBIT) below.

Indeed over the course of this graph, its North American segment has

increased its contribution to overall segmental EBIT from 44.3% to

48.6%. Meanwhile China (traditionally its highest margin market) has

disappointed and the only other regions to be at a high watermark are

emerging markets and the CEE.

Moreover in terms of categories, footwear contributes two

thirds of its North American revenues and the growth outside North

America is largely coming from footwear.

Clearly the strong performance over the last years is thanks to North

America and footwear globally. Part of this is – no doubt- due to the

success of sponsorship deals with established stars in sports like

basketball and running. Another favorable aspect is the trend towards

casual footwear.

The last point is an industry trend that shouldn’t be underestimated. For example a company like V.F. Corp(NYSE: VFC)

has some strong outdoor activity brands such as The North Face, Vans

and Timberland. All three of these brands contain a strong superficial

appeal to consumers but, not necessarily from those that do actually

undertake mountaineering, hiking or skate boarding! People will buy the

products just to be associated with these sports (and the lifestyle)

even if they don't do them so -almost bizarrely- marketing efforts must

focus on promoting these activities.

Growth opportunities

Aside from ongoing execution in North America, there are three main near-term growth opportunities.