This blog is devoted to helping investors make informed decisions. It will be regularly updated and provide opinions on earnings results. It is not intended to give investment advice and should not be taken as such. Consult your investment advisor.

It’s always interesting to use earnings season as a way to formulate a

view on the economy. Unfortunately, anyone looking for some positive

news on the industrial sector would have been disappointed by the recent

results from industrial supply companies Fastenal(NASDAQ: FAST) and MSC Industrial Direct(NYSE: MSM). What did these companies say, and what does it all mean for the industrial sector?

Mixed growth in the industrial sector

In short, outside of areas like aerospace and aviation, the

industrial sector remains weak. Earlier in the week, aluminum supplier Alcoa(NYSE: AA) came out with a positive report that gave cause for optimism.

The company always gives good color on its industrial end markets,

and the fact that it failed to reduce guidance for China has to be taken

as a positive. The good news on China was somewhat surprising because

companies like FedEx, Pall, and Oracle have all come out and stated specific weakness in China. Nonetheless, we should take what Alcoa said at face value.

Similarly, Alcoa’s global aerospace, automotive, and industrial gas

turbine segments remain set for good growth in 2013, even if Europe is a

little weaker. Since Alcoa is saying good things, surely the industrial

supply companies would, too? They are always useful as a

bellwether because their sales cycle is relatively short. This means

that any change in conditions will immediately be seen in their sales

figures.

Fastenal adjusts its strategy

Unfortunately, Fastenal and MSC Industrial both had negative outlooks on the industrial sector.

Fastenal spoke of a slow economic condition causing its

fastener sales (a cyclical product) to remain weak. In a sense, this

apes the overlying Institute for Supply Management (ISM) manufacturing

numbers, which have been softer in 2013. The ISM surveys private

manufacturing companies in order to produce its Purchasing Managers

Index (PMI), which is the leading manufacturing indicator in the U.S.

Note how the strength in new orders (which usually precede a pick-up

in the headline PMI numbers) quickly dissipated in February, while the

headline PMI number has averaged 49.7 this year. A number below 50

indicates negative growth.

In fairness, Fastenal did point out in the previous conference call

that its sales were not represented by the stronger ISM data in the

first quarter (ISM new orders had averaged 54.2 in the first three

months). However, this historical relationship came back into line in

the second quarter as both the ISM and Fastenal’s sales growth was

weaker.

The company’s response is to try to drive sales by making significant

new hires (mainly sales support staff) in its stores. The idea is to

hire 600-900 new in-store staff by the end of the year. The plan would

enable its existing managers to have more free time to visit more

customers, increasing sales accordingly.

It’s an interesting approach, because previously Fastenal’s main

focus was on expanding the installations and sales of its vending

machines. However, with competitors like MSC Industrial also building

out its vending machines and Amazon increasingly moving

in on the industrial supply market, Fastenal may feel that a balanced

approach to growth is a better way to deal with a slow industrial

market.

MSC Industrial also weak

The theme of adjusting to macro weakness was shared by MSC

Industrial. The company decided against implementing its mid-year

pricing increase in a concession to a softer demand environment. It’s

tough to get customers to accept price increases at the best of times,

let alone when end demand is weak. The good news for MSC Industrial is

that it has non-cyclical ways to increase profitability:

The acquisition of Barnes Distribution North America will increase revenues, margins and create opportunities.

Its e-commerce revenues are growing at north of 40%.

It has the potential to increase vending machine installations.

Obviously, these three aims are easier to achieve given a stronger

demand environment, and if you buy the "second-half industrial recovery"

story, then MSC and Fastenal are interesting propositions. On the other

hand, until the headline ISM manufacturing indices improve, investors

should brace themselves for more disappointments and negative sentiment

around the sector.

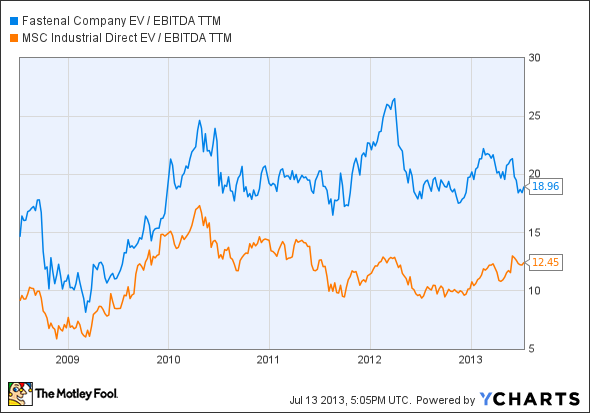

In comparing the two companies, MSC Industrial comes out on top in

terms of valuation and potential to grow earnings despite the economic

cycle.

In conclusion, these results told similar story to the first

quarter's about MSC and Fastenal and their end markets. It appears that

Alcoa’s optimism is more related to the strength of some of its

particular industry segments, such as aerospace and automotive.

Investors in Fastenal and MSC would do well to ignore Alcoa and focus

more on the ISM numbers in order to see where prospects for the two

companies are headed.

Alternatively, there is a strong case for simply staying invested

within the areas of strength in the industrial sector. It’s too early to

proclaim a general second half pick-up.

No comments:

Post a Comment