Food company McCormick (NYSE: MKC )

is down over 13% from its high of the year as disappointing sales in

some of its markets dragged the stock lower. The spice and seasoning

maker has long been attractive thanks to its defensive-growth prospects,

demographic appeal and long-term potential within emerging markets.

However, its valuation has also looked a bit too spicy for a while. Is

the recent weakness a chance to buy in?

What happened?

The recent third quarter results were disappointing, and McCormick indicated that its full-year earnings per share would come in at the lower end of its $3.13 to $3.19 range. Similarly, its full-year adjusted operating income is now forecast to grow 3% to 5% versus a prior forecast of 5% to 7%. What went wrong?

McCormick reported three weak points in the

quarter. First, its industrial division saw weak demand from its quick

service restaurant customers in the quarter. Essentially, the fast food

companies are seeing lower demand, and they are also tailoring their

products and promotions toward the kinds of items (breakfast, coffee,

etc) that McCormick doesn't sell into. On a more positive note,

McCormick argued that China was a bit better than expected.

We had weak demand from quick service restaurants in the U.S. and China, although China was better than we expected as sales begin to recover from consumer concerns about bird flu earlier this year.

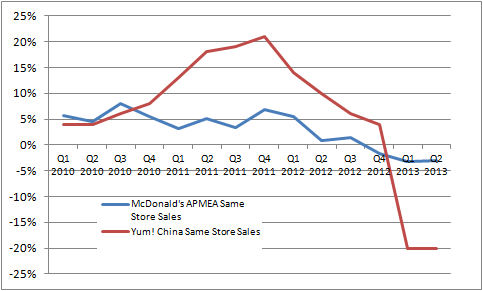

Given that Yum! Brands (NYSE: YUM )

is a key customer of McCormick (it's almost certainly being referred

to in the above statement), then this is relatively good news for Yum!'s

plans to return to growth in China. Over the last year, Yum! has been

hit by food safety scares, and an outbreak of bird flu has kept

customers worried. With McCormick indicating that China was relatively

positive, it can be seen as a good portent for Yum!'s next results.

source: company accounts

Second, McCormick outlined that its US consumer sales were lower at the start

of the quarter. They did come back up toward the end of the quarter,

but it wasn't enough to counteract the earlier weakness. Furthermore,

there was a pull-forward in consumer sales in the third quarter. This

was due to retailers aggressively taking up McCormick's holiday display

program (an initiative that McCormick does to encourage early season

sales), and this induced customers to buy early for the holiday season.

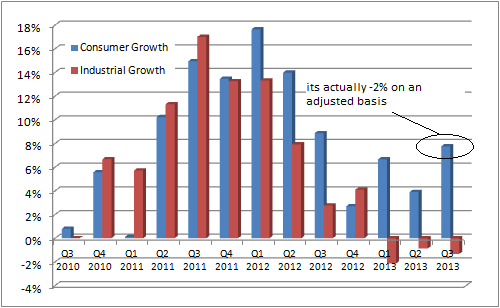

In fact, if overall consumer sales are adjusted for

currency, the pull-forward effect and the sales contribution from its

WAPC acquisition mean that its consumer sales actually declined by 2%.

It wasn't a strong set of results for McCormick.

source: company accounts

And finally, McCormick's underlying international

consumer sales were not strong either. Sales in Europe, the Middle East

and Africa, or EMEA, were flat (constant currency) with a year ago. It

wasn't much better in Asia-Pacific, or APAC, either. Sales in China were

down 5% (constant currency) on a comparable basis, but they rose 54% on

the back of a 59% contribution from WAPC. Furthermore, the company's

sales in India declined. This must have come as a disappointment,

because only two years ago it formed a joint venture with Kohinoor

Specialty foods in India.

A reason to be cheerful

The good news is that McCormick guided toward a better outcome in the next quarter, and in particular, from the part of the company's sales that really matters. After the quarter started off weakly in regard to US consumer sales, McCormick saw a stronger trend at the end of the quarter. Its management predicted that the trend would continue into the fourth quarter, and ultimately lead to a 7% sales increase in the quarter.

While industrial sales are likely to remain weak,

remember that McCormick generates around 80% of segment income from its

consumer sales. Moreover, WAPC will contribute to sales growth in the

quarter as well, even if the underlying picture in China isn't that

strong.

Going forward, if McCormick can get US consumer

sales back on track and make some more acquisitions, then it may be able

to ride through this difficult period.

Where next for McCormick?

In conclusion, McCormick's valuation still looks a little stretched for the risks involved. With a current share price of around $64.80 it still trades at a P/E ratio around 21 times its forecast earnings for 2013. The company has good long-term prospects, but it needs to start delivering.

MKC Price to Earnings Less Cash TTM data by YCharts

McCormick's current performance isn't great, and

the positive forecast for the next quarter is yet to be delivered.

Despite the pull-back in the share price, it still isn't a good value

yet.

No comments:

Post a Comment