When it comes to investing, sometimes it's best to start with the

obvious and look for companies that have the potential to slowly grow.

Contact lens specialist Cooper Companies (NYSE: COO ) is one such stock, and it's definitely worth taking a closer look at it.

Cooper Companies growth prospectsCooper

reports numbers in two separate segments. CooperVision is a soft

contact lens manufacturer generating 80% of revenues. CooperSurgical

generates 20% of revenues, with two-thirds coming from surgical devices,

and one-third from its fast growing fertility treatment products. I'm

going to focus on CooperVision.

Cooper's management is on record as expecting the

soft contact lens market to grow at a 4%-6% clip this year. The bad news

is that, for a second quarter running, the worldwide market only grew

at 4%. This suggests that market demand is not as strong as it could be.

The good news is that CooperVision managed to grow

its sales by 11% over the last 12 months, and there are a number of

reasons why it can continue to grow.

First, its silicone hydrogel lenses (more

comfortable, last longer) revenues now make up 43% of CooperVisions

total. They grew at 22% (constant currency) in the last quarter, and

Cooper can expect to generate more growth in the future from customers

"trading up" to these lenses.

Second, Cooper's management never tires of pointing

out that a customer trading up to its single-use (or one-day) lenses

generates four to six times more revenue and three to five times more

profit. In other words, there is ample room for growth in earnings and

margin growth from expanding one-day sales. For reference, its

single-use sphere revenues only make up 21% of CooperVision revenues

(17% of total company), and they grew at 9% in constant currency in the

last quarter.

Third, Cooper plans to move in on Johnson & Johnson's (NYSE: JNJ ) dominant position in the two-week modality in the U.S. by marketing its own two-week lenses.

Fourth, Cooper has just launched its new branded

one-day silicone hydrogel based lens called MyDay in Europe. According

to the management, MyDay is "not going to be a major influence" next

year because sales are building from a small base. It will take Cooper

time to build up production capacity, but longer-term Cooper should have

good prospects with MyDay.

And finally, Cooper has plans to geographically

expand sales of its leading Biofinity (monthly silicone hydrogel

lenses). Moreover, it can cut costs thanks to not paying royalties,

because sillicone hydrogel patents will expire in the U.S. in 2014 and

globally in 2016.

Threats to growth?While Cooper has been growing, there is no guarantee that it will continue to do so. Indeed, Valeant Pharmaceutical's (NYSE: VRX ) purchase of Bausch & Lomb

suggests that competition will get tougher. For example, Bausch &

Lomb recently launched a one-day lens. Moreover, Valeant has worldwide

plans to generate synergies between its existing dermatology and

eye-care products, and Bausch & Lomb's eye-care solutions. Valeant

will surely invest in trying to expand Bausch & Lomb's international

sales.

Similarly, Johnson & Johnson managed to

accelerate growth in its vision-care segment to 5.4% operationally in

the last quarter, and it cited its one-day lenses as one of "the primary

contributors to operational growth." Cooper is not alone in recognizing

the margin potential of one-day lenses, and Johnson & Johnson has a

formidable distribution network in the kinds of emerging markets that

Cooper wants to expand into.

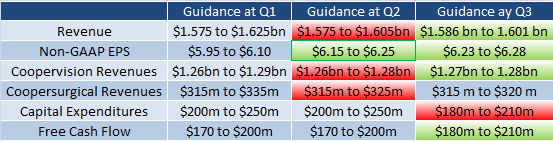

A look at the numbersCooper has strong prospects, but it also has a strong valuation. Cooper's own EPS guidance has increased throughout the year.

Source: Company presentations.

However, its valuation has more than kept pace, and

it now sits on a forward P/E of over 20 times the mid-point of its

full-year EPS guidance. This looks expensive, but recall that Cooper has

long-term margin expansion opportunities. Furthermore, a better gauge

of its value is to look at its free cash flow potential. I've chosen to

adjusted for the increased capital expenditure program it's undertaking

right now. Cooper is investing in order to develop production capacity

and to accelerate sales of its silicone hydrogel based sales.

In the following table, I have assumed that capital

expenditures equate to depreciation in order to give a better picture

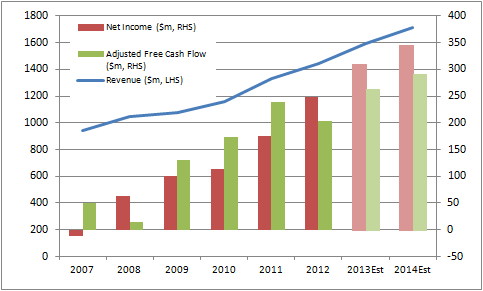

of underlying cash flow generation.

Sources: Company releases, author's estimates for 2013 and 2014.

My underlying free cash-flow estimates of $264

million and $290 million for the next two years indicate that Cooper

continues to generate plenty of cash. However, these figures represent

only around 4% and 4.3% of its current $6.65 billion enterprise value.

Cooper is an attractive company, but its valuation

gives little room for error, and it operates in a very competitive

market against giants like Johnson & Johnson and Novartis (Alcon). It's a great company, but one to keep on your watchlist for now.

No comments:

Post a Comment